What Is Realized Volatility in Crypto? RV vs IV Explained (2026)

— By Tony Rabbit in Tutorials

Understand realized volatility (RV) and implied volatility (IV) in crypto. Learn how these metrics differ, why IV is often higher, and what the gap between

In the dynamic world of cryptocurrency, understanding volatility is paramount for anyone looking to navigate the markets effectively. From spot trading to advanced options strategies, volatility is a constant companion. But not all volatility is created equal, nor is it measured in the same way. This guide will demystify two crucial concepts: realized volatility (RV) and implied volatility (IV), explaining their differences, their relationship, and how you can use them to gain an edge in your crypto trading decisions.

As we look towards 2026 and beyond, the sophistication of crypto markets continues to grow. Tools and metrics that were once the exclusive domain of institutional finance are now readily accessible. Mastering RV and IV is a key step in becoming a more informed and strategic participant in this evolving landscape.

What Is Realized Volatility (RV) in Crypto?

Realized volatility, often abbreviated as RV, is a backward looking measure. It quantifies the actual variability of an asset's price over a specific historical period. Think of it as a historical report card for price swings. If a token's price has bounced up and down significantly over the last week, its 7 day realized volatility will be high. Conversely, if its price has been relatively stable, its RV will be low.

RV is calculated by looking at past price data, typically using daily, hourly, or even minute by minute returns. Common windows for calculating RV include 7 day, 30 day, or 60 day periods. This makes it an objective measure, as it's based purely on what has already occurred in the market. Traders often use RV to understand the historical risk profile of an asset or to calibrate their expectations for future price movements, although RV itself doesn't predict the future.

- RV is a historical measure, reflecting past price movements.

- It is calculated from actual price data over a specific time window.

- Common lookback periods include 7 day, 30 day, or 60 day.

- High RV indicates significant past price swings, while low RV suggests relative stability.

Understanding Implied Volatility (IV)

In contrast to RV, implied volatility (IV) is a forward looking metric. It represents the market's expectation of future volatility for an asset. IV is not directly calculated from past price data; instead, it is derived from the current prices of options contracts on that asset. When you see an options pricing model, IV is the volatility input that makes the model's theoretical price match the actual market price of an option.

If options for a particular cryptocurrency are trading at very high prices, it suggests that the market participants expect significant price swings in the future, leading to a high IV. Conversely, if options are cheap, it implies expectations of lower future volatility and thus a lower IV. IV is a crucial component for options traders, as it directly impacts the premium of an option. It reflects the collective sentiment and expectations of market participants regarding an asset's future price behavior.

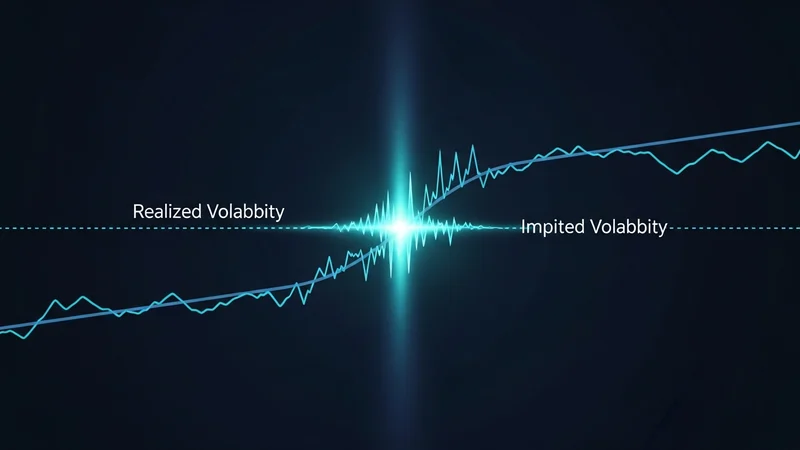

RV vs. IV: The Core Differences Explained

The fundamental distinction between realized and implied volatility lies in their temporal orientation and their source of data. RV looks backward, at what has happened. IV looks forward, at what the market expects to happen. This difference is critical for understanding their utility in trading and analysis.

While RV is a factual account of past price action, IV is a projection, a consensus forecast embedded in options prices. This makes IV a powerful indicator of market sentiment and perceived risk. A rising IV often signals increasing uncertainty or anticipation of a significant market event. Conversely, a falling IV can suggest growing complacency or a belief that the market will remain calm.

The Volatility Risk Premium: Why IV is Usually Higher Than RV

One of the most observed phenomena in volatility analysis is that implied volatility is usually higher than realized volatility. This persistent difference is known as the volatility risk premium. It's not a coincidence; there's a logical economic reason behind it.

Option sellers, who take on the risk of future price movements, demand compensation for that uncertainty. They are essentially selling insurance against large price swings. To entice them to take on this risk, the price of options (and thus the embedded IV) is generally inflated above what the actual historical volatility has been. This premium compensates sellers for the possibility of unexpected, large moves that could lead to significant losses. It's their cushion against the unknown future.

This means that, on average, options tend to be priced slightly higher than what the asset's actual future volatility turns out to be. This premium ensures that option sellers are adequately compensated for bearing the risk. Understanding this dynamic is crucial for anyone involved in options trading, as it forms the basis for many strategies.

Interpreting the Gap Between IV and RV

The relationship between IV and RV is not static; the gap between them constantly changes and provides valuable insights into market sentiment and potential opportunities. Observing this gap is a key part of advanced market analysis.

A Wide Gap (IV > RV)

When IV is significantly higher than RV, it indicates that the market is expecting more volatility in the future than it has experienced in the recent past. This wide gap can reflect several scenarios:

- Fear or Uncertainty: Traders might be anticipating a major market event, regulatory changes, or macroeconomic shifts that could cause significant price swings. This drives up demand for protection (options), pushing IV higher.

- Event Pricing: Ahead of specific known events, such as a major protocol upgrade, token unlock, or earnings report for a related company, IV often spikes as traders position themselves for potential volatility.

- Demand for Protection: Investors might be buying options to hedge their spot positions against potential downturns, increasing demand and thus IV.

A wide gap can suggest that options are relatively 'rich' or expensive compared to the recent historical price action. This might present opportunities for option sellers who believe the market's future volatility expectations are overblown.

A Narrow or Negative Gap (IV <= RV)

Conversely, a narrow gap, or even a rare negative gap where IV is lower than RV, can signal different market conditions:

- Complacency: A narrow gap often suggests that the market is complacent, expecting future volatility to be similar to or even less than recent historical volatility. Traders might not foresee any significant catalysts.

- Underpricing of Options: In rare cases, if IV is significantly below RV, it could imply that options are 'cheap' relative to the asset's recent price action. This might signal that the market is underestimating future volatility.

- Post Event Cool Down: After a major event has passed and the expected volatility did not materialize, IV can drop sharply, potentially even below RV temporarily.

A narrow or negative gap might indicate that options are relatively 'cheap'. This could be attractive for option buyers who believe that future volatility will pick up and exceed current market expectations.

Conclusion

Realized volatility and implied volatility are two sides of the same coin when it comes to understanding price fluctuations in crypto markets. RV provides a factual look at the past, while IV offers a glimpse into the market's collective expectations for the future. The interplay between these two metrics, particularly the often observed volatility risk premium and the dynamic gap between them, offers profound insights for traders and investors.

By comparing RV and IV, you can judge whether options appear rich or cheap, anticipate potential market shifts, and refine your trading strategies. As crypto markets mature, the ability to interpret these sophisticated volatility measures will become an increasingly valuable skill, empowering you to make more informed decisions and navigate the landscape with greater confidence.

Frequently Asked Questions

What is the main difference between realized volatility and implied volatility?

Realized volatility (RV) measures actual past price fluctuations, making it backward looking. Implied volatility (IV) is forward looking, representing the market's expectation of future volatility, derived from options prices.

Why is implied volatility usually higher than realized volatility?

IV is typically higher than RV due to the volatility risk premium. This premium compensates option sellers for taking on the risk and uncertainty of future price movements, as they are essentially providing insurance against large swings.

What does a wide gap between IV and RV signal?

A wide gap, where IV is significantly higher than RV, often reflects market fear, anticipation of major events, or strong demand for protection. It suggests that the market expects more future volatility than recently experienced.

What does a narrow or negative gap between IV and RV indicate?

A narrow or negative gap (IV equal to or lower than RV) can signal market complacency, a belief that future volatility will be low, or that options are relatively cheap. It might suggest the market is underestimating future price swings.

How can traders use RV and IV in their strategies?

Traders compare RV and IV to assess if options are 'rich' (expensive) or 'cheap'. A high IV relative to RV might indicate selling opportunities, while a low IV relative to RV could suggest buying opportunities, depending on one's outlook on future volatility.