Robinhood Chain Was Sold as 24/7 Stocks. One Week In, We Read the Chain: It Is Running on Memecoins

— By Tony Rabbit in News

Robinhood Chain went live on July 1 as a 24/7 tokenized-stock network. We read the chain a week later, and the open on-chain liquidity is memecoins and a stablecoin, not equities. The real stock tokens are synthetic debt instruments, blocked to US users, and a rounding error of activity, while imposter AAPL and TSLA tickers already trade.

On July 1, 2026, Robinhood flipped the switch on Robinhood Chain, its own Ethereum Layer-2 built on the Arbitrum stack and pitched as the home of 24/7 tokenized stocks that plug straight into DeFi. The keynote in London called it the future of markets. A week later, we did the thing the marketing does not invite: we read the chain. Its RPC answered on chain ID 4663, it is live and public, and anyone can pull its data. So we did, and the picture on-chain is very different from the pitch. The open, permissionless activity on the tokenized-stock chain is not stocks. It is memecoins.

What Robinhood Chain was sold as

The pitch is genuinely ambitious, and parts of it are real. Robinhood Chain is an Ethereum Layer-2 that uses ETH for gas with no separate chain token, settles in about a tenth of a second, and shares 10% of its net fees back to the Arbitrum ecosystem. It launched with a DeFi lineup on day one and the promise of tokenized US stocks you can hold in self-custody and trade around the clock. If you want the full primer on how the chain works and who can actually use it, our Robinhood Chain explainer covers it. The launch itself is not the story here. What the chain is being used for, one week in, is.

What we found when we read the chain

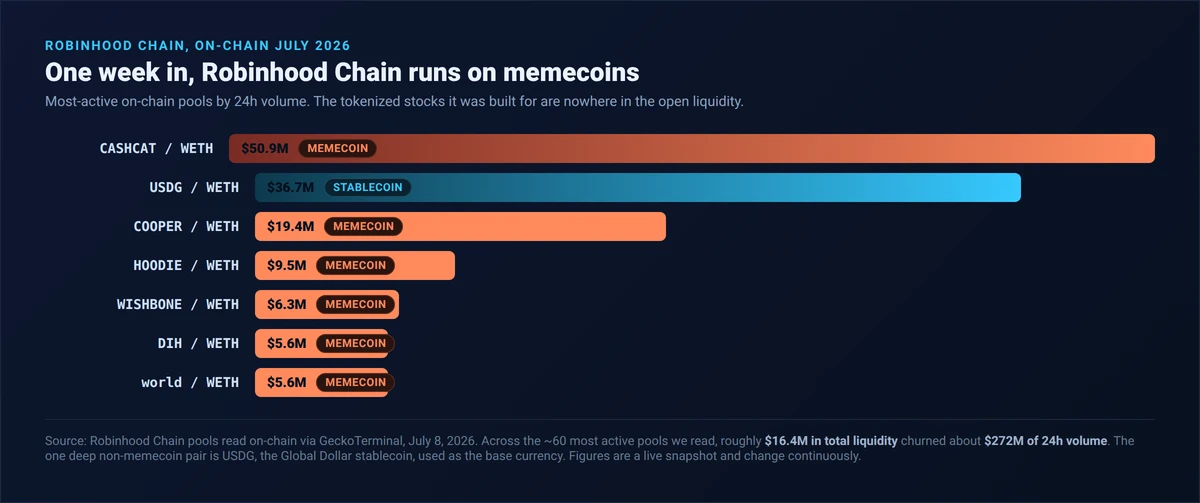

We pulled the most active pools on Robinhood Chain directly from on-chain data. Across the roughly sixty busiest pools, about $16.4 million of liquidity was churning around $272 million of volume in a single day. And almost every one of those pools is a memecoin: CASHCAT, COOPER, HOODIE, WISHBONE, DIH, VLAD, Hoodlings, a token literally called world. They trade on Uniswap, PancakeSwap and Bankr. The one deep pool that is not a memecoin is USDG, the Global Dollar stablecoin, which the chain uses as its base currency.

To be fair, this is normal for a brand-new permissionless chain. Open blockspace attracts memecoin speculation first, everywhere, because anyone can deploy and trade instantly. It is not unique to Robinhood. But it is a striking gap between the marketing, which is about tokenized equities, and the on-chain reality, which right now is a memecoin venue with a stablecoin attached. By reported counts of early transfers, the actual Stock Tokens were only around 0.27% of activity, while wrapped ETH and memecoins made up the rest.

The danger zone: volume with almost no liquidity

Inside that memecoin activity is a pattern worth flagging for anyone tempted to ape in. Fourteen of the pools we read held under $1,000 of liquidity while each traded more than $200,000 in a day. Some are far more extreme: one COOPER pool traded $19.4 million on about $10,000 of liquidity, and a HOODIE pool traded $7.66 million on roughly $3. A pool that turns over thousands of times its own liquidity in a day is not doing price discovery. It is the classic thin-liquidity pattern that correlates with wash trading and liquidity traps, where the exit can vanish the moment you try to sell.

This is exactly the kind of thing to screen before you touch it, on any chain. Paste a contract into the DEXTools Token Safety Checker and look at liquidity depth, holder concentration and sell-side health before you buy, not after.

The real stock tokens: synthetic, US-blocked, and a rounding error

So where are the tokenized stocks the chain was built for? They exist on-chain, but they are a small slice of activity and they are not what most people assume. According to Robinhood's own documentation, its Stock Tokens are "tokenised debt securities issued by Robinhood Assets (Jersey) Limited" that grant holders "no legal or beneficial rights in, or against the issuer of, those underlying securities." In plain terms: you get price exposure through a debt instrument, not the share itself, with no voting and no ownership. US users are blocked from them entirely, along with several other jurisdictions.

There is a second catch that is pure DeFi. Because Robinhood Chain is permissionless, anyone can deploy an ERC-20 and call it whatever they like. When we searched the chain for stock tickers, we did not find deep official equity markets. We found imposters: multiple tiny "AAPL" pools with roughly $2,400 of liquidity each, a scattering of "TSLA" pools worth a few thousand dollars, all spun up in the last day. Anyone who assumes a token named AAPL on Robinhood's chain is a real Robinhood stock token can walk straight into a ticker-squatting trap. The genuine, canonical stock tokens are a specific set of contracts; everything else wearing the ticker is not.

How the tokenized stocks compare

The distinction matters because tokenized stocks are increasingly used as DeFi collateral. A synthetic, issuer-linked debt token carries a bankruptcy and counterparty risk that a custody-backed token, or the real share, does not. That is not a knock on Robinhood specifically, it is the structural reality traders need to price in, and it is why the tokenization narrative and the token-safety narrative are the same conversation. For the wider picture, our guide to real-world assets lays out how these instruments are built.

Why it matters, and what to watch

None of this means Robinhood Chain is a failure. It is one week old, it is a real product from a company with tens of millions of users, and the tokenized-stock share of activity could climb from here. That is exactly the honest metric to watch: does the equity side actually grow, or does the chain settle in as another memecoin venue with a premium brand on it? There is a business subtext too. Robinhood's crypto revenue fell about 47% year on year to $134 million in the first quarter of 2026, so leaning into tokenization is partly a hedge against fading retail crypto trading. The ambition is real. So is the on-chain gap between the pitch and the print. Read the chain, not the press release.

- a real product on a mainstream on-ramp, live mainnet since July 1, 2026

- self-custody plus 24/7 settlement is a genuine step for tokenized assets

- it shares 10% of its fees with the Arbitrum ecosystem, and it is only one week old

- the open liquidity is memecoins and one stablecoin, not equities

- the real stock tokens are synthetic debt, US-blocked, and a rounding error of activity

- because the chain is permissionless, imposter AAPL and TSLA tickers already trade

The takeaway is not that tokenized stocks are a scam or that Robinhood Chain is a bust. It is that on-chain, right now, the marketing and the money are pointed in different directions, and only the chain tells you which is which. That gap is the whole reason to read the data yourself.

Methodology and disclaimer: pool liquidity, 24h volume and the memecoin-versus-stablecoin composition were read on-chain from Robinhood Chain via GeckoTerminal on July 8 to 9, 2026, and the chain ID (4663) was confirmed by querying Robinhood Chain's public RPC directly; on-chain figures are a live snapshot and change continuously. The "~0.27% of early transfers" figure and the day-one DeFi lineup are as reported by third parties and were not independently recomputed by us. The Stock Token structure ("tokenised debt securities... no legal or beneficial rights"), the US restriction, the July 1, 2026 mainnet launch and the Q1 2026 crypto revenue decline are from Robinhood's own documentation, newsroom and regulatory filings. References to imposter tickers describe permissionless tokens that reuse well-known names and are not affiliated with the companies or with Robinhood; they are a general safety observation, not an allegation against any named party. This article is for information only and is not financial or investment advice. Tokenized assets and memecoins are volatile and can lose all value; do your own research.