What Is Maple Finance? Institutional DeFi Lending Guide 2026

— By Tony Rabbit in Tutorials

Maple Finance explained: syrupUSDC yields, Cash Management pool, SYRUP tokenomics, $5B+ originated, and how to earn 9-15% APY in institutional DeFi.

Maple Finance is the largest institutional credit marketplace in decentralized finance (DeFi), with over $5 billion in cumulative loans originated since launch and a fresh post-FTX architecture that turned a 2022 collapse into one of the cleanest comeback stories in onchain credit. If you have ever wondered how prime brokers, market makers, and trading firms borrow USDC and BTC onchain at scale, Maple is where most of that activity actually happens.

Founded in 2019 in Sydney, Australia by Sid Powell and Joe Flanagan (both ex-traditional credit), Maple combines the underwriting discipline of a private credit fund with the composability of smart contracts. Lenders deposit stablecoins or BTC into curated pools, professional Pool Delegates underwrite institutional borrowers, and depositors receive yield-bearing receipt tokens like syrupUSDC that plug straight into Aave, Pendle, Curve, and Spark.

This guide is the most complete English-language walkthrough of Maple Finance available in 2026. You will learn what makes the v2 architecture different from the original Maple, how syrupUSDC and the Cash Management pool work, why the MPL to SYRUP token migration mattered, and the practical steps to deposit, earn, and withdraw with the cooldown mechanism. We finish with the unflinching risk discussion every institutional product deserves.

What Is Maple Finance?

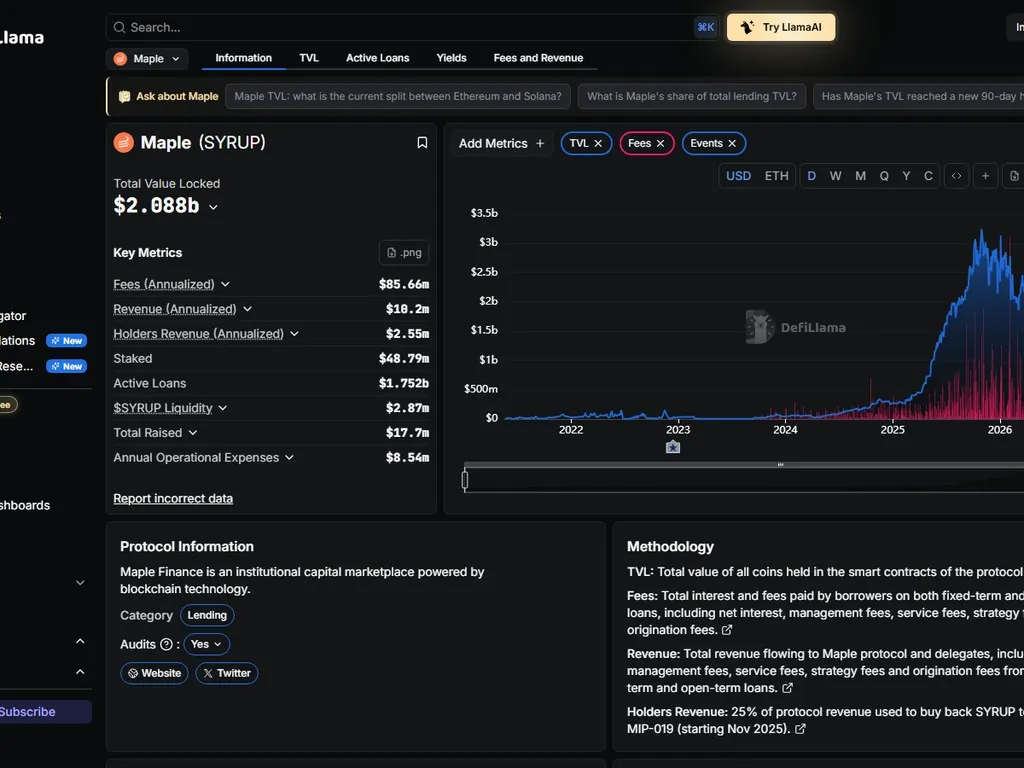

Maple Finance is an institutional DeFi lending protocol where verified borrowers (typically crypto-native market makers, prime brokers, and trading firms) access overcollateralised or under-collateralised loans funded by liquidity providers who earn yield in return. It is the bridge between professional credit underwriting and permissionless onchain liquidity, currently operating across Ethereum, Base, and Solana with more than $2 billion in active TVL.

Unlike money markets like Aave or Compound that rely purely on algorithmic interest rate curves, Maple uses human Pool Delegates who underwrite each borrower individually. This is a fundamentally different credit model: every loan is term-based, every borrower is KYC verified, and pricing is negotiated rather than dictated by utilisation curves.

The History of Maple Finance: From Sydney Startup to $5B Originated

Maple was founded in 2019 by Sid Powell and Joe Flanagan, two Australian credit professionals who had spent years inside traditional debt capital markets. Their thesis was simple: crypto-native trading firms desperately needed working capital for inventory, basis trades, and market-making operations, but no bank would lend to them. At the same time, DeFi was minting yield from nowhere, much of it backed by unsustainable token emissions rather than real cash flows.

The first Maple pools went live on Ethereum in May 2021. By the end of that year, Maple was the dominant uncollateralised lender in DeFi, with pools managed by Maven 11, Orthogonal Trading, Celsius (yes, that Celsius), and Icebreaker Finance. Cumulative loan originations crossed $1.4 billion within the first nine months.

Then November 2022 happened. The FTX collapse cascaded through every crypto credit desk on the planet. Orthogonal Trading, one of Maple's largest Pool Delegates, had quietly extended significant unsecured credit to Alameda Research and lied to its own depositors about the exposure. When FTX filed Chapter 11 on 11 November 2022, Orthogonal's pools became insolvent overnight. Maple lender losses across the Orthogonal pool totalled approximately $36 million.

This was the existential moment. Most protocols would have died. Instead, Maple v2 was already in development and the team accelerated a complete redesign: tighter delegate vetting, mandatory collateral on most new pools, real-time onchain reporting, and a clear separation between high-yield secured products and the original unsecured model. By mid-2023 Maple was originating loans again, this time with a structurally safer architecture and a sharper focus on overcollateralised products.

How Maple Finance Works: The Architecture

The Maple v2 architecture has four key participant roles. Understanding each is essential before you deposit a single dollar.

Professional credit underwriters who manage a pool, vet borrowers, set loan terms, and earn a cut of interest. The closest thing DeFi has to a credit officer.

Anyone (retail or institutional) who deposits USDC, USDT, or BTC and receives a yield-bearing token like syrupUSDC representing their share of the pool.

KYC verified institutions (market makers, prime brokers, miners) who post collateral and draw down term loans for trading capital or operations.

The Maple smart contracts that hold funds, enforce loan terms, mint receipt tokens, distribute interest, and handle the withdrawal cooldown mechanic.

When a lender deposits USDC into the Maple High Yield Secured pool, the protocol mints them syrupUSDC at the current exchange rate. The deposit sits in the pool waiting to be drawn by an approved borrower. The Pool Delegate has already done the underwriting work: a credit memo, financial statements, collateral arrangements, and term sheet are all negotiated before the loan goes live. When a borrower draws funds, they post agreed collateral (typically BTC, ETH, or stables) into a separate escrow contract, and the loan begins accruing interest at the agreed rate, often paid daily.

Interest flows back into the pool and the exchange rate of syrupUSDC versus USDC slowly increases. That is how depositors earn yield: no rebasing, no claimable rewards by default, just a quietly appreciating receipt token that always represents a growing share of the underlying USDC.

syrupUSDC: The Yield-Bearing Token That Plugs Into All of DeFi

syrupUSDC is arguably the most important product Maple has ever shipped. It is an ERC-20 token, fully composable, representing a holder's share of the Maple High Yield Secured pool. As the underlying loans accrue interest, syrupUSDC appreciates against USDC. One syrupUSDC was worth approximately 1.06 USDC by Q1 2026, reflecting roughly 12 months of accumulated yield.

Because syrupUSDC is a standard ERC-20 with a published oracle price, it has become a building block across DeFi. Lenders are no longer choosing between Maple yield and DeFi liquidity. They can have both.

- Aave V3: syrupUSDC is listed as collateral on Ethereum mainnet, letting holders borrow stablecoins against their yield-bearing position

- Pendle: syrupUSDC has principal token and yield token markets, allowing yield separation and fixed-rate strategies

- Curve: syrupUSDC/USDC liquidity pool offers instant exit liquidity without waiting for the cooldown

- Spark Protocol: syrupUSDC accepted as collateral inside the MakerDAO ecosystem

- Morpho Blue: isolated markets where users borrow against syrupUSDC at custom LTV ratios

This composability is what makes Maple meaningfully different from traditional private credit. In TradFi, locking capital into a credit fund means giving up liquidity entirely until the next quarterly redemption window. With syrupUSDC, you can deposit, accrue yield, and still use the token as collateral on Aave or sell it on Curve if you need to exit before the cooldown finishes.

The Maple Product Suite: Four Distinct Pools

Maple is not one product. It is a stack of four distinct credit products targeting different risk profiles and yield levels.

1. High Yield Secured Pool (syrupUSDC)

This is the flagship. Lenders deposit USDC. Pool Delegates lend that USDC to KYC verified institutional borrowers (Wintermute, FalconX, Auros, BlockFills, Flow Traders, and similar prime trading firms) at rates between 9% and 15% APY. Every loan is overcollateralised with BTC or ETH posted into onchain escrow, and loans are short-duration (typically 30 to 90 days) so the book turns over quickly.

This is the pool that most retail and DeFi-native depositors use. It is also the pool whose receipt token (syrupUSDC) is composable across the DeFi protocols listed above. As of May 2026, this pool alone holds more than $1.2 billion in deposits.

2. Cash Management Pool (US Treasuries RWA)

For institutional treasuries that want yield without crypto credit risk, Maple offers a Cash Management pool that allocates USDC into short-duration US Treasury bills via a regulated custodian. Yield tracks the federal funds rate, currently producing around 4.5% to 5.0% APY net of fees, with effectively zero credit risk.

This product directly competes with offerings from Ondo Finance and other tokenized real-world asset (RWA) issuers. It targets crypto-native DAOs, foundations, and venture funds who want to park stablecoin treasury in something earning real yield without exposing themselves to private credit defaults.

3. BTC Yield Product

One of the harder problems in DeFi has been earning native yield on Bitcoin without wrapping into questionable bridges or staking derivatives. Maple's BTC Yield pool accepts BTC deposits, lends the BTC to institutional borrowers for delta-neutral trading strategies (basis trades, funding arbitrage, futures market making), and returns yield in BTC.

Net APY on BTC Yield has hovered between 4% and 7% throughout 2025-2026, depending on funding rates and demand for BTC borrow inventory. Loans are again secured with collateral, typically denominated in USDC or stablecoins, posted into Maple's escrow contracts.

4. Permissioned Institutional Pools

Maple still operates several KYC-gated pools for accredited investors and institutions that require regulated access. These pools offer higher yields (sometimes 15% to 20%+ APY) on more specialised credit products but require full institutional onboarding, accredited investor verification, and longer lockup periods.

The MPL to SYRUP Token Migration

For its first five years, the Maple ecosystem token was MPL. In late 2024, the community approved a token migration to SYRUP at a 1:100 ratio. Every 1 MPL was exchanged for 100 SYRUP, with the migration window staying open into 2025. The rationale was twofold: align the token name with the syrupUSDC product brand, and create a larger token supply that could support deeper liquidity and broader staking participation.

The 1:100 split was purely cosmetic in economic terms. Total fully diluted value did not change, governance weight did not change, and economic claims on protocol revenue did not change. But the rebranding was strategically meaningful: it signalled that Maple's identity was tied to its productive yield-bearing tokens, not legacy DeFi token tickers.

SYRUP Tokenomics

SYRUP has a total supply of roughly 1.16 billion tokens. Holders can stake SYRUP to receive stSYRUP, which earns a share of protocol revenue (origination fees, performance fees, and reserve fund growth). Staked SYRUP also participates in governance votes that decide which new Pool Delegates are onboarded, which assets are listed, and how the treasury is deployed.

A meaningful share of the supply is allocated to the Drips program, the ongoing incentive campaign that distributes SYRUP rewards to syrupUSDC holders, liquidity providers in syrupUSDC/USDC pools, and integration partners. We will cover Drips in detail later.

How to Deposit USDC and Earn With syrupUSDC: Step by Step

For retail and DeFi-native users, depositing into the High Yield Secured pool takes about three minutes. Here is the complete walkthrough.

Step 1: Connect Your Wallet

Navigate to syrup.fi (the official Maple lender app) and click Connect Wallet. MetaMask, WalletConnect, Coinbase Wallet, Rabby, and most major wallets are supported. Make sure you are on Ethereum mainnet, although Base and Solana deposits are also available through their respective interfaces. Always double-check the URL before connecting (a common phishing vector). Read our wallet security guide if you want a refresher on safe DeFi habits.

Step 2: Approve USDC Spend

Maple's smart contracts need permission to pull USDC from your wallet. This is a standard ERC-20 approval. We recommend approving the exact amount you intend to deposit rather than unlimited spending, even though the gas cost is slightly higher. Our breakdown of token permission safeguards explains why bounded approvals are safer.

Step 3: Deposit USDC and Receive syrupUSDC

Enter the amount you want to deposit and confirm the transaction. The Maple pool contract pulls your USDC and mints you the equivalent syrupUSDC at the current exchange rate. The rate is always greater than 1.0 USDC per syrupUSDC because the pool has been earning interest since launch. As of mid-2026 the rate sits around 1.06, meaning every syrupUSDC you receive is already backed by roughly 1.06 USDC of underlying assets.

Step 4: Earn Yield Automatically

Your syrupUSDC sits in your wallet (no claim required) and quietly appreciates against USDC as borrowers pay interest. Yield compounds automatically inside the pool. There is no claiming, no manual restaking, and no gas fees for compounding. Your position grows continuously.

Step 5: Withdraw (The Cooldown Mechanism)

This is the part most newcomers miss. Maple is not an instant withdrawal protocol. Because the underlying USDC is loaned to institutional borrowers on term loans, the pool cannot honour an instant unlimited withdrawal. Instead, Maple uses a request-and-cooldown system. You initiate a withdrawal request by burning some of your syrupUSDC. After a cooldown period (typically 7 to 30 days depending on pool conditions), you can claim your USDC. If you need instant liquidity, you can alternatively swap syrupUSDC for USDC on Curve at a small discount.

Maple Finance vs Other Institutional DeFi Lenders

Maple is not the only institutional credit protocol onchain, although it is the largest. Here is how it stacks up against the leading alternatives.

The differentiators that matter for Maple in 2026 are: largest TVL in the category, strongest secondary market liquidity for its receipt token (syrupUSDC), deepest integration across DeFi (Aave, Pendle, Curve, Spark, Morpho), and the cleanest post-FTX track record after redesigning the architecture around overcollateralisation. Centrifuge wins on real-world asset diversity, Goldfinch wins on emerging market exposure, but for trading-firm credit secured by crypto collateral, Maple is the default venue.

Who Borrows From Maple? The Institutional Borrower List

Transparency on the borrower side is one of Maple's underrated strengths. Every active loan is published onchain with borrower name, loan size, term, interest rate, and collateral. Recent and active borrowers from the High Yield Secured pool include some of the largest names in crypto market making and prime brokerage.

- Wintermute: one of the largest crypto market makers globally, regular borrower for trading inventory

- FalconX: institutional prime broker serving hedge funds and asset managers

- Auros: algorithmic market maker active across CEX and DEX venues

- BlockFills: OTC desk and prime brokerage for crypto institutions

- Flow Traders: traditional finance market maker with crypto desk

- Flowdesk, GSR, Cumberland: additional rotation of MM borrowers depending on pool capacity

If you want to understand the broader category these firms operate in, our guide to market makers in crypto is the right starting point. These are the firms providing two-sided liquidity on exchanges every minute of every day, and they need short-term working capital to fund inventory and basis positions. Maple is one of their cleanest sources of that capital.

The Drips Incentive Program: Earn SYRUP While You Lend

Drips is Maple's ongoing token incentive program that rewards users for holding syrupUSDC, providing liquidity to syrupUSDC pools, and integrating syrupUSDC into other DeFi protocols. As of mid-2026, the program is in its third season.

The mechanics are straightforward: every block, a fixed allocation of SYRUP is distributed pro-rata across eligible participants. You do not need to claim, stake, or lock. Simply holding syrupUSDC in a wallet or LP position registers you for the rewards, which accrue as a "Drips" balance you can claim at any time.

The effective yield boost from Drips has historically ranged from 1% to 4% APY on top of the underlying pool yield, depending on the SYRUP token price and total participation. For lenders looking at a 12% base yield from the High Yield Secured pool, Drips often pushes the effective gross APY into the 14% to 16% range.

Drips Season 3 Multipliers

Season 3 introduced multiplier categories that reward stickier capital. Locking syrupUSDC for longer durations, providing liquidity to syrupUSDC/USDC Curve pools, or holding stSYRUP all unlock multipliers (1.5x, 2x, even 3x in some categories). These are explicitly designed to bootstrap deep secondary market liquidity for syrupUSDC, which is the single biggest factor in syrupUSDC adoption across the DeFi stack.

The Risks: What Can Go Wrong

Maple Finance is one of the better-engineered credit protocols in DeFi, but anyone telling you that institutional lending is risk-free has not been paying attention. Here are the specific risks lenders should price in before depositing.

1. Underwriting Failure (The Orthogonal Lesson)

The single biggest risk in any credit protocol is bad underwriting. November 2022 proved this brutally: Orthogonal Trading, one of Maple's largest delegates, lied to the protocol and to depositors about its exposure to Alameda Research, and the resulting default cost lenders approximately $36 million. The Maple v2 redesign explicitly addresses this by mandating overcollateralisation on most new pools and tightening delegate vetting, but the residual risk is never zero. A pool delegate could still misjudge a borrower's creditworthiness, and a sudden market move could leave collateral insufficient.

2. Collateral Volatility and Liquidation Lag

Most Maple loans are secured with BTC, ETH, or stablecoin collateral. If crypto prices fall rapidly between collateral checks, a borrower's position can briefly go underwater. Maple has automated collateral monitoring and margin calls, but unlike Aave there is no instant liquidator bot ready to seize collateral within a single block. Resolution can take hours or days, which means a sharp drawdown could expose lenders to temporary undercollateralisation. Our explainer on liquidation zones is worth reading if you want to understand how collateral safety margins really work.

3. Smart Contract Risk

Maple's contracts have been audited multiple times by Spearbit, Three Sigma, Trail of Bits, and other reputable firms. There has never been a contract-level exploit. But every smart contract carries non-zero risk of a previously undiscovered bug. The protocol's bug bounty program is generous, and the contracts have been battle-tested with billions of dollars of throughput, but you cannot rule out exploit risk completely.

4. Withdrawal Cooldown Risk

Because the underlying pool is funding term loans, instant withdrawals are not guaranteed. In a stress scenario where many lenders try to exit at once, the cooldown queue can extend, and the discount on syrupUSDC in Curve secondary markets can widen significantly. We saw small versions of this dynamic during the 2024 mini-cycle dips, with syrupUSDC briefly trading at a 0.5% to 1.0% discount before normalising.

5. Regulatory Risk on RWA Products

The Cash Management pool and other RWA products rely on offchain regulated custodians and brokers. Changes in US Treasury regulation, custodian counterparty risk, or regulatory action against tokenized RWA products could disrupt these specific pools. The High Yield Secured pool is less exposed since it operates on crypto-native collateral, but the regulatory perimeter around DeFi credit is still being drawn.

6. Pool Delegate Concentration Risk

While Maple has more delegates than in 2022, the largest pools still represent significant capital concentration with specific underwriting teams. If a single delegate makes a series of bad calls, the impact on that pool's lenders is direct and immediate.

Maple by the Numbers: 2026 Snapshot

The growth trajectory matters. Two years after the FTX shockwave nearly killed the protocol, Maple has more than tripled its peak 2022 TVL, expanded across Ethereum, Base, and Solana, and become the canonical institutional lender in DeFi. Independent dashboards on DefiLlama and Token Terminal corroborate these numbers in real time.

Advanced Strategies With syrupUSDC

For users comfortable with DeFi composability, syrupUSDC unlocks several layered strategies that meaningfully boost effective yield.

Strategy 1: Aave Looping

Deposit syrupUSDC as collateral on Aave V3, borrow USDC against it at 70% LTV, deposit the borrowed USDC back into Maple to mint more syrupUSDC, and repeat. After three or four loops, the effective yield on your original capital can rise from 12% to 18% to 22% APY, depending on Aave's USDC borrow rate. The catch: leverage amplifies any losses if Maple has an underwriting issue, and your position can be liquidated on Aave if syrupUSDC depegs in secondary markets.

Strategy 2: Pendle Yield Tokenisation

Pendle separates syrupUSDC into Principal Tokens (PT) and Yield Tokens (YT). Buying PT-syrupUSDC at a discount lets you lock in a fixed APY until maturity. Buying YT gives you leveraged exposure to the underlying syrupUSDC yield without holding the principal. Sophisticated yield farmers use Pendle to bet on rising or falling Maple rates, similar to interest rate swaps in TradFi.

Strategy 3: Curve LP Plus Drips

Provide liquidity to the syrupUSDC/USDC Curve pool. You earn trading fees from people exiting Maple positions before the cooldown completes, plus your LP position is eligible for Drips Season 3 multipliers. Effective LP yields have run 10% to 14% APY through 2026, with low impermanent loss because both sides of the pair are tightly correlated stablecoin instruments.

Strategy 4: Treasury Allocation Mix

A DAO treasury might allocate 60% to Cash Management pool (low risk, ~5% APY), 30% to High Yield Secured (moderate risk, ~12% APY), and 10% to syrupUSDC LP on Curve (active management, ~12% APY plus Drips). The blended yield exceeds 8% APY with diversified credit exposure, while maintaining stablecoin denomination throughout.

Maple on Multiple Chains: Ethereum, Base, Solana

Maple started as an Ethereum-only protocol. By 2025 the team had launched canonical deployments on Base and Solana, with bridged syrupUSDC variants accessible on both. The strategic case for multichain expansion is straightforward: institutional borrowers want access to the cheapest gas and fastest finality available, and lenders want exposure to high-throughput chain ecosystems where stablecoin activity is growing.

On Base, deposits use the same USDC contract as Ethereum and the cooldown logic is identical. Solana deployment uses native USDC and integrates with Solana DeFi protocols like Kamino and Drift for syrupUSDC composability. If you want to understand the broader L2 landscape this fits into, our coverage of Ethereum's roadmap and how rollups changed DeFi is the natural prerequisite.

Pros and Cons of Using Maple Finance

- Highest yields in institutional DeFi credit (9-15%)

- syrupUSDC composability across Aave, Pendle, Curve

- Transparent onchain reporting of every loan

- Overcollateralised since the v2 redesign

- SYRUP Drips program boosts effective APY

- $5B+ originated, deep institutional borrower roster

- Underwriting risk if a delegate misjudges credit

- 7-30 day cooldown for direct withdrawals

- Historical default (Orthogonal, $36M, 2022)

- Regulatory uncertainty around RWA products

- syrupUSDC can trade at discount in secondary markets

- Yields lower than aggressive yield farms or restaking

How Maple Compares to Lending on Aave or Compound

This is a common point of confusion. Aave and Compound are money markets: anyone can deposit, anyone can borrow against collateral they post, and interest rates are set algorithmically based on pool utilisation. Maple is a credit market: borrowers are individually underwritten institutions, loan terms are negotiated, and pools are managed by professional delegates rather than smart contract curves.

The practical implication is yield. Aave USDC supply typically pays 3% to 6% APY because anyone can borrow against ETH or BTC collateral. Maple's High Yield Secured pool pays 9% to 15% because the borrowers are willing to pay a premium for committed term financing tailored to their trading book. The flip side is that Aave gives you instant liquidity while Maple imposes a cooldown.

If you want the deepest pool, instant withdrawals, and pure algorithmic pricing, Aave is the right venue. If you want yield generated by real institutional credit demand and you are comfortable with a 7-30 day cooldown, Maple delivers a meaningfully different product. Many sophisticated users hold positions in both: Aave for liquidity, Maple for yield.

Governance and stSYRUP: Owning a Slice of the Protocol

Holding SYRUP gives you economic exposure to Maple's growth. Staking SYRUP into stSYRUP gives you that exposure plus governance voting power plus a claim on protocol revenue. Origination fees from every new loan flow into the staking reward pool, alongside performance fees on the Cash Management product. As Maple originations grew from $4 billion to over $5 billion across 2025-2026, stSYRUP revenue scaled in step, producing an additional yield layer on top of any SYRUP price appreciation.

Governance votes typically cover decisions like onboarding new Pool Delegates, listing new collateral assets, adjusting protocol fee parameters, and approving treasury allocations. The Maple DAO has been notably active compared to many DeFi governance bodies, with consistent monthly proposal cadence and high participation rates from stSYRUP holders. The most influential recent votes have included the syrupUSDC listing on Aave V3, the Solana deployment authorisation, and the structure of the Drips Season 3 reward distribution.

For users who want exposure to the Maple thesis without taking direct credit risk, holding stSYRUP is the cleanest way to participate. You get the upside of protocol growth without the downside of a specific loan defaulting, and your tokens still earn yield from the protocol's collected fees regardless of which individual pools perform best in a given period.

Maple's Role in the Broader RWA Trend

One of the dominant narratives in DeFi through 2025 and 2026 has been the migration of real-world assets onchain. From tokenized US Treasuries to private credit funds to tokenized money market funds, traditional finance instruments are being wrapped as ERC-20 tokens at an accelerating pace. Estimates put onchain RWA value north of $20 billion by mid-2026, with private credit specifically representing the fastest-growing subcategory.

Maple sits at the intersection of two RWA subcategories: institutional crypto credit (where the collateral is onchain but the borrower is a regulated entity) and tokenized treasuries (through the Cash Management pool). This dual positioning is strategically valuable. Pure crypto credit protocols are exposed to crypto market cycles, while pure RWA tokenizers are exposed to traditional finance interest rates. Maple captures both ends, letting depositors rotate between high-yield secured crypto credit and lower-risk treasury exposure within a single ecosystem.

If you want a broader view of how tokenized assets are reshaping yield products, our explainer on RWA tokenization covers the regulatory landscape, custodial structures, and competing protocols in the space. Maple is one of the most credible operators in the institutional credit slice of that broader market.

Frequently Asked Questions

Q Is Maple Finance safe?

Maple v2 is meaningfully safer than v1 thanks to mandatory overcollateralisation, tighter delegate vetting, and real-time onchain reporting. No protocol-level exploit has occurred, and contracts have been audited by Spearbit, Three Sigma, and Trail of Bits. However, credit risk is never zero: the November 2022 Orthogonal default cost lenders approximately $36 million, and a future underwriting failure remains possible. Size positions accordingly.

Q What is syrupUSDC and how is it different from USDC?

syrupUSDC is the yield-bearing receipt token you receive when you deposit USDC into Maple's High Yield Secured pool. It is a standard ERC-20 that appreciates against USDC over time as borrowers pay interest. Unlike USDC (which is always worth 1.00 USD), 1 syrupUSDC was worth roughly 1.06 USDC by Q1 2026. The token is composable across Aave, Pendle, Curve, and Spark.

Q What APY can I earn on Maple Finance in 2026?

The High Yield Secured pool (syrupUSDC) has historically yielded 9% to 15% APY, currently averaging around 12%. The Cash Management pool yields roughly 4.5% to 5.0% backed by US Treasuries. BTC Yield pays 4% to 7% in BTC. The Drips Season 3 incentive program can add another 1% to 4% effective yield in SYRUP tokens on top of base APY.

Q How do I withdraw USDC from Maple?

Maple uses a cooldown withdrawal system. You initiate a withdrawal request by burning your syrupUSDC, and after a cooldown period (typically 7 to 30 days depending on pool utilisation) you can claim USDC at the prevailing exchange rate. For instant exit, you can swap syrupUSDC to USDC on the Curve secondary market, usually at a small discount of 0.1% to 0.5%.

Q Who founded Maple Finance and where is it based?

Maple was founded in 2019 by Sid Powell (CEO) and Joe Flanagan (President), both former traditional credit professionals based in Sydney, Australia. The team has since expanded globally, with personnel in Sydney, Singapore, London, and New York supporting both crypto-native and institutional clients.

Q What happened to Maple during the FTX collapse?

In November 2022, Orthogonal Trading (a Maple Pool Delegate) had extended significant unsecured credit to Alameda Research and misrepresented its exposure to lenders. When FTX collapsed, Orthogonal's pool became insolvent and lenders suffered approximately $36 million in losses. Maple responded with the v2 architecture redesign, mandating overcollateralisation on most new pools, stricter delegate vetting, and improved real-time reporting.

Q What is the difference between MPL and SYRUP tokens?

MPL was the original Maple governance and value-accrual token. In late 2024 the community approved a migration to SYRUP at a 1:100 ratio, meaning every 1 MPL was exchanged for 100 SYRUP. The split was cosmetic in economic terms (total value, governance weight, and revenue claims were unchanged) but aligned the token brand with the syrupUSDC product line. SYRUP can be staked to receive stSYRUP and a share of protocol revenue.

Q Who are Maple Finance's biggest borrowers?

Maple's borrower roster includes some of the largest crypto market makers and prime brokers in the world: Wintermute, FalconX, Auros, BlockFills, Flow Traders, GSR, Flowdesk, and Cumberland. Every active loan is published onchain with borrower name, size, rate, and collateral, giving full transparency to lenders.

Q How does Maple compare to Aave for lending stablecoins?

Aave is a money market with algorithmic interest rates and instant withdrawals, typically paying 3% to 6% APY on USDC. Maple is a credit market with negotiated loans to KYC institutions, paying 9% to 15% APY but requiring a withdrawal cooldown. Aave is best for liquidity and price-discovery yield, while Maple delivers higher yield backed by real institutional credit demand.

Q What is the Drips airdrop program?

Drips is Maple's ongoing SYRUP incentive program, now in Season 3. Lenders who hold syrupUSDC, LP in syrupUSDC/USDC Curve pools, or hold stSYRUP automatically accrue SYRUP rewards. There is no claim-and-stake process required: rewards stream in real time and can be claimed at any point. The effective yield boost averages 1% to 4% APY on top of the base lending yield, with multipliers for stickier capital.

Q Can I use syrupUSDC as collateral on Aave?

Yes. syrupUSDC was listed as collateral on Aave V3 mainnet through governance proposal, allowing holders to borrow USDC or other stablecoins against their yield-bearing Maple position. This enables looping strategies that amplify the effective Maple yield, although leverage also amplifies any underwriting losses or syrupUSDC depeg risk.

Q Is the Cash Management pool the same as Ondo's OUSG?

They are similar in concept (both are tokenized US Treasury exposure) but use different custodians, legal structures, and target audiences. Ondo's OUSG and USDY products target permissionless and accredited DeFi users with broad distribution. Maple's Cash Management pool is more institutional-focused, targeting crypto-native DAOs and treasuries who already use Maple for credit products. Both produce yield approximately equal to the federal funds rate minus fees.

Conclusion: Why Maple Matters for DeFi's Next Phase

Institutional credit is the missing piece in mature financial systems, and Maple has built the most credible onchain version of it. With $5 billion in cumulative originations, a redesigned post-FTX architecture, and a yield-bearing token that plugs into Aave, Pendle, Curve, and Spark, Maple has become the default venue for stablecoin holders who want institutional-grade yield without giving up DeFi composability.

The 9% to 15% APY available on syrupUSDC is not magic. It is the spread between what trading firms pay for working capital and what depositors are willing to accept for committed liquidity, net of underwriting fees. That spread exists because credit is genuinely useful in crypto and because professional underwriting is genuinely hard to replicate with smart contract logic alone.

The right way to think about Maple is as a stablecoin yield engine that uses DeFi as distribution and traditional credit discipline as the production model. For risk-aware lenders willing to accept a withdrawal cooldown and real (if mitigated) credit risk, the product set is the most compelling in the institutional DeFi category. Start small, understand the cooldown mechanic, study the borrower disclosures, and size your position relative to your total stablecoin allocation. If you do, Maple becomes one of the cleaner sources of real yield in onchain finance.

For deeper context on the protocols Maple plugs into, see our guides on Pyth Network oracles, USDT and stablecoin design, and tokenized treasuries. The Maple ecosystem only makes full sense in the context of the broader RWA and DeFi credit landscape.