What Is a Crypto Savings Account? Yield Guide (2026)

— By Tony Rabbit in Tutorials

A crypto savings account lets you earn yield on idle coins. Learn how a crypto savings account works, the APY, and the risks before you deposit.

A crypto savings account is a product that pays you yield, usually quoted as an annual percentage yield (APY), for depositing your digital assets instead of letting them sit idle in a wallet. In traditional finance, a bank pays interest because it lends your deposit out. Crypto savings accounts work on a similar idea, but the plumbing and the risks are very different, and that difference is the whole point of this guide.

If you are comparing a high yield crypto savings account against simply holding, the headline number is only half the story. The other half is who controls your coins, how the yield is actually produced, and what happens if something breaks. Let us start with how the money is made.

How Do Crypto Savings Accounts Work?

The yield does not appear from nowhere. A crypto interest account has to do something productive with your deposit to generate a return. There are three common engines behind the APY:

- Lending: Your coins are lent to borrowers (traders, market makers, or other users) who pay interest. That interest, minus a platform cut, becomes your yield.

- Staking: On proof-of-stake networks, deposited tokens help secure the blockchain and earn protocol rewards. The platform stakes on your behalf and passes on most of the rewards.

- DeFi protocols: Funds are routed into automated lending markets or liquidity pools governed by smart contracts, where rates move with supply and demand.

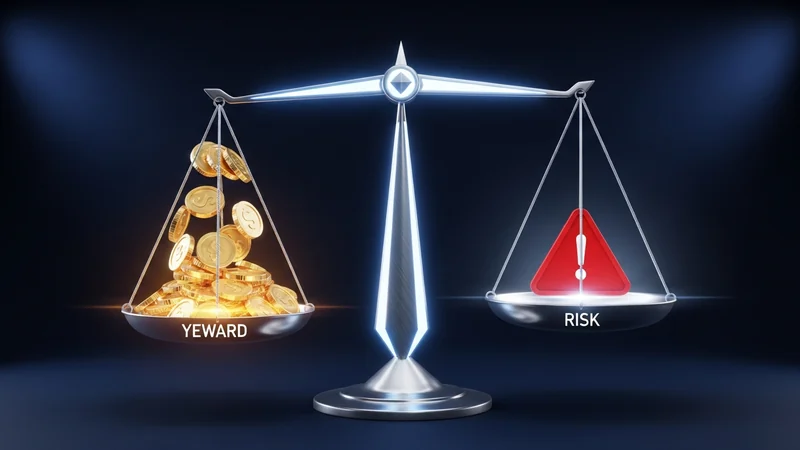

Understanding which engine is running matters, because each one carries its own failure mode. A 5 percent yield from over-collateralized lending is not the same risk as a 5 percent yield from an opaque trading desk, even though the number on the screen looks identical.

CeFi vs DeFi Savings Accounts

The market splits into two broad camps. Centralized finance (CeFi) platforms operate like companies: you create an account, pass identity checks, and the firm custodies your coins and manages the yield strategy for you. Decentralized finance (DeFi) earn products are smart contracts you interact with directly from your own wallet, with no company holding your keys.

Neither model is automatically safer. CeFi is convenient but you must trust the operator. DeFi is transparent and non-custodial but exposes you to code risk and demands more technical care. Here is a side by side view.

| Feature | CeFi savings account | DeFi earn |

|---|---|---|

| Custody of coins | Platform holds your assets | You keep your own keys |

| Main risk | Counterparty and insolvency risk | Smart-contract risk |

| Ease of use | Simple, app based | Requires a wallet and on-chain skills |

| Transparency | Limited, you trust their books | Auditable on-chain |

| Identity checks | Usually required | Usually none |

What APY Can You Expect?

Rates move constantly with market conditions, so treat any quoted figure as a snapshot rather than a promise. As a general guide in 2026, yields on major stablecoins from reputable venues have tended to sit in the low to high single digits, while some CeFi platforms advertise higher tiers in exchange for holding their native token or locking funds for fixed terms.

A useful rule: the further a yield sits above the broad market average, the harder you should look at where it comes from. Outsized APY is almost always paying you for extra risk, whether that is a thinly traded token, an unproven protocol, or a borrower base you cannot see. When a return looks too good, the missing piece is usually the risk being hidden.

The Risks You Must Understand

This is the most important section, so read it slowly. A crypto savings account is not a bank account, and the protections you may assume exist often do not.

- Not FDIC or SIPC insured: Crypto deposits are generally not covered by US deposit insurance. If the platform fails, there is no government backstop to make you whole.

- Counterparty and insolvency risk: With CeFi, you are an unsecured creditor. If the firm becomes insolvent, you may recover little or nothing and may wait years in bankruptcy proceedings.

- Smart-contract risk: DeFi protocols can be exploited through code bugs, even after audits. A single vulnerability can drain a pool.

- Depeg risk: If your yield is paid on a stablecoin and that stablecoin loses its peg, the underlying value can fall even while the APY keeps ticking.

- Withdrawal freezes: Platforms under stress have paused withdrawals, locking users out exactly when they wanted to exit.

Cautionary Lessons from 2022

These are not hypothetical risks. In 2022 a cluster of high profile crypto lenders collapsed. Voyager Digital filed for bankruptcy in early July 2022, Celsius Network filed days later in mid July 2022, and BlockFi filed in late November 2022. The trigger sequence ran through the collapse of the TerraUSD stablecoin in May 2022 and the failure of the hedge fund Three Arrows Capital, with BlockFi later pushed over the edge by the failure of FTX.

The common thread was custody and counterparty risk. Customers had handed over their coins, the platforms took on risk those customers could not see, and when the market turned, depositors became creditors in a bankruptcy line. Separately, in February 2022 the US SEC reached a settlement with BlockFi over its interest accounts, treating them as unregistered securities offerings. The lesson is durable: convenience and a high advertised rate are no substitute for knowing how a platform actually operates.

How to Use a Crypto Savings Account Safely

You can engage with these products thoughtfully if you follow a few disciplined habits:

- Only deposit what you can afford to lose, and never your entire stack.

- Favor established platforms and protocols with long track records and public audits.

- Read how the yield is generated. If the platform cannot or will not explain it clearly, treat that as a red flag.

- For DeFi options, research the protocol and the token before depositing. You can use DEXTools to inspect a token, check on-chain liquidity, and review trading activity before you trust a pool with your funds.

- Diversify across platforms and strategies rather than concentrating in one venue.

- Watch for depeg signals on any stablecoin you hold.

Alternatives to a Crypto Savings Account

A savings account is just one way to earn on crypto. Depending on your goals and risk tolerance, you might consider these instead or alongside it:

- Direct staking: Staking native tokens yourself (or through a non-custodial service) keeps you closer to your keys and the protocol rewards.

- Stablecoin yield in DeFi: Supplying stablecoins to established lending markets, with the smart-contract and depeg caveats above.

- T-bill backed products: Tokenized products designed to track short term US Treasury yields aim to ground returns in traditional assets rather than crypto lending demand.

When you screen any DeFi earn opportunity, doing your own homework is essential. DEXTools is a practical starting point for checking a token contract, verifying that liquidity is real and reasonably deep, and tracking how holders behave before you commit capital.

Conclusion

A crypto savings account can turn idle coins into yield, but the APY is only meaningful once you understand the engine behind it and the risks attached. Decide whether you value the convenience of CeFi or the self-custody of DeFi, size your position to what you can lose, and verify every platform and token before you deposit. This article is for education only and is not financial advice, so treat it as a framework for asking better questions, not a recommendation to buy or deposit anything.

The Yield Curve: Navigating Variable and Fixed-Term Opportunities

While the fundamental premise of a crypto savings account is to generate yield, the sophisticated investor understands that not all yield is created equal. The "yield curve" in traditional finance refers to the relationship between the interest rate (or cost of borrowing) and the time to maturity of the debt. In the nascent crypto savings landscape, we can draw parallels, observing how different platforms and product structures offer varying APYs based on factors like lock-up periods, underlying protocols, and perceived risk.

Understanding this nuanced "crypto yield curve" is crucial for optimizing returns. A higher APY often corresponds to either a longer lock-up period, greater exposure to volatile DeFi protocols, or a less liquid asset. Conversely, lower APYs are typically found with flexible, instant-access accounts or those backed by more stable, regulated entities, albeit with potentially higher overheads.

Optimizing Your Yield Strategy

- Assess your liquidity needs: Do you require immediate access to funds, or are you comfortable locking them up for a period?

- Diversify across platforms and assets: Avoid single points of failure by spreading your investments across multiple reputable providers.

- Understand the underlying mechanics: Is the yield generated through lending, staking, or liquidity provision? Each carries distinct risk profiles.

- Monitor market conditions: Yields can fluctuate significantly based on demand for borrowing, network activity, and overall market sentiment.

- Factor in withdrawal fees and gas costs: These can eat into your net yield, especially for smaller deposits or frequent transactions.

- Consider stablecoin vs. volatile asset yields: Stablecoin yields generally offer lower but more predictable returns, while volatile assets carry higher potential upside but also greater price risk.

Related Guides

- What Is zkSync Era? Account Abstraction L2

- What Is Safe: Multisig Wallets, Smart Accounts and Treasury Control (2026)

- Coinbase Smart Wallet: Passkey & Base Account Guide 2026

- What Is Biconomy: Account Abstraction, Gasless UX and Cross-Chain Execution (2026)

- What Is Biconomy: Account Abstraction, Gasless UX and Smart Account Infrastructure (2026)

Frequently Asked Questions

What is a crypto savings account?

A crypto savings account is a service that lets you deposit cryptocurrency to earn yield over time. The provider typically generates returns by lending out or deploying the deposited funds.

How does a crypto savings account generate yield?

Yield usually comes from lending deposits to borrowers, deploying them in DeFi, or other strategies run by the provider. The advertised rate reflects the return passed on to depositors, often expressed as an APY.

What is APY on a crypto savings account?

APY, or annual percentage yield, expresses the yearly return on a deposit including the effect of compounding. It lets you compare different products, though rates can change and are not guaranteed.

What are the risks of a crypto savings account?

Risks include the provider failing or becoming insolvent, smart contract issues in DeFi based products, and the volatility of the underlying crypto. Deposits are often not protected the way traditional bank deposits can be.