Bitcoin Derivatives Flash a Warning as a $1B Deribit Put Looms at $60K

— By Tony Rabbit in Markets

Bitcoin derivatives are sending a bearish signal as BTC trades near $61,000 to $62,500, with open interest down 8.5% and a $1 billion put cluster sitting at the $60,000 strike on Deribit.

Bitcoin derivatives are flashing a clearly bearish signal as the largest cryptocurrency trades near $61,000 to $62,500. Open interest has fallen about 8.5% to roughly $111.4 billion as leverage was flushed out of the market, while traders rush to buy downside protection. The mood across the options market has shifted from confidence to caution in a matter of sessions.

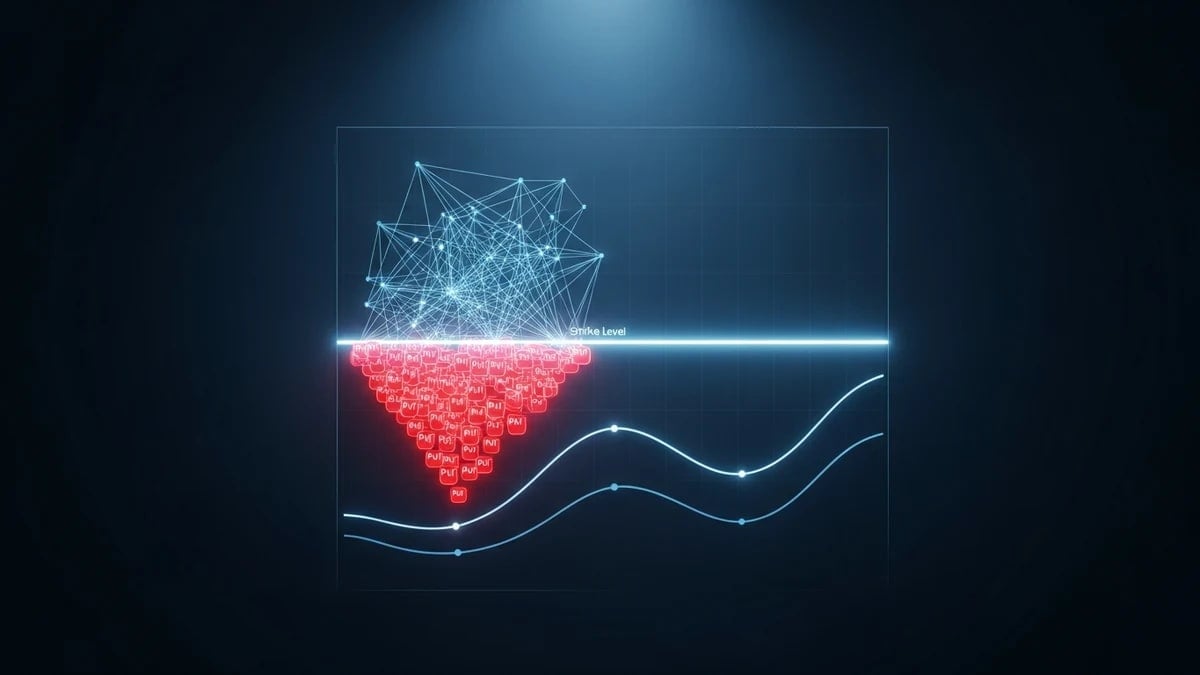

At the center of the story is a single price level. A $60,000 strike put option on Deribit now carries over $1 billion in notional open interest, and as spot drifts toward that strike, the chance of large position adjustments grows. That combination of a heavy put cluster, rising implied volatility and aggressive selling pressure is exactly what makes seasoned traders nervous. Below we break down what each of these signals means in plain language and why they matter right now.

What the Derivatives Data Is Saying

The headline number is open interest. Open interest is the total value of outstanding derivatives contracts that have not yet been closed or settled. A falling open interest reading, like the 8.5% drop to roughly $111.4 billion, usually means positions are being closed and leverage is leaving the system. When leverage is flushed out, it can reduce the risk of a sudden cascade of forced liquidations, but it can also signal that traders are stepping back and reducing exposure because they expect trouble ahead.

At the same time, the way traders are positioning tells a story of fear rather than greed. Money is flowing into protective contracts, and the cost of that protection is climbing. That points to a market that is bracing for downside rather than chasing upside.

The $1 Billion Put at $60,000 Explained

A put option gives its holder the right to sell an asset at a fixed price, known as the strike, before the contract expires. Traders buy puts to protect against falling prices or to bet that a price will drop. When a put gains more than $1 billion in notional open interest at a single strike, that strike becomes a magnet for attention because so much money is concentrated there.

The $60,000 strike sits just below where Bitcoin is currently trading. As spot approaches that level, the dealers and market makers who sold those puts have to manage their own risk. They often do this by selling the underlying asset or related futures to stay balanced, a process that can add fuel to a move lower. In short, a large put cluster near spot can amplify volatility precisely when the market is already fragile, turning a routine pullback into a sharper slide.

Implied Volatility Is Climbing

Implied volatility measures how much the market expects an asset to move in the future, based on the prices traders are willing to pay for options. Higher implied volatility means options are getting more expensive because demand for them is rising. It is often described as the market's fear gauge.

Right now that gauge is heating up. Volmex's 30-day implied volatility indexes for Bitcoin, known as BVIV, and for Ether, known as EVIV, have surged over recent sessions. That jump reflects a clear demand for options-based hedging, with traders paying up to insure their portfolios against a deeper drop. Rising implied volatility does not predict direction on its own, but combined with the other signals here it underlines how defensive the market has become.

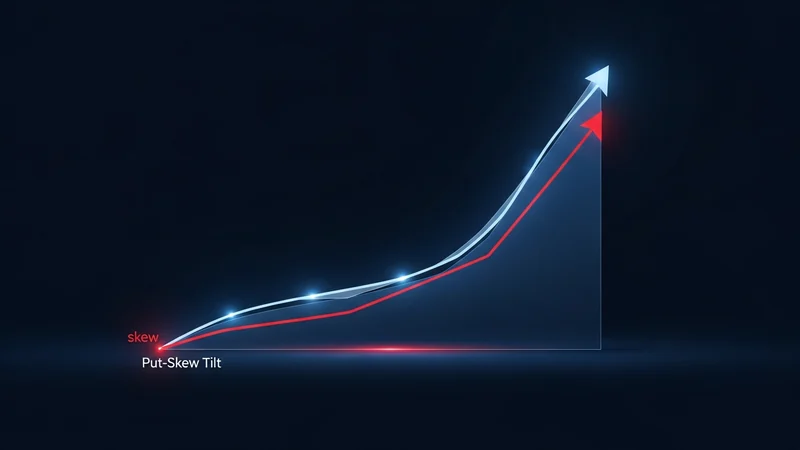

Put Skew Shows Traders Want Protection

Put skew compares the cost of downside protection against the cost of upside bets. When put options become more expensive than equivalent call options, the skew is said to strengthen toward puts. It is one of the cleanest ways to read which direction traders are most worried about.

In this market, put skews have strengthened in both Bitcoin and Ether. Traders are paying a premium for downside protection, which tells us they see the risk of a fall as greater than the chance of a rally in the near term. A persistent put skew is a hallmark of a defensive, risk-off market rather than a confident, risk-on one.

Aggressive Selling in the Spot Market

Derivatives are not the only place showing pressure. The 24-hour cumulative volume delta across the top 20 tokens is negative. Cumulative volume delta measures the difference between aggressive buying and aggressive selling, and a negative reading means sellers are hitting bids with market orders rather than patiently placing passive limit orders.

That distinction matters. Aggressive market selling shows urgency and conviction among sellers, and it tends to move prices faster than passive flows. When this kind of selling lines up with a defensive options market and a giant put cluster just below spot, the warning signs reinforce one another. Traders watching real-time flow on platforms like DEXTools can see how this aggressive selling spreads across tokens rather than staying confined to Bitcoin alone.

Why These Signals Matter Together

Any one of these data points could be noise. Open interest falls and rises all the time, and implied volatility ebbs and flows with the news cycle. What makes the current picture notable is the alignment. Falling open interest, surging implied volatility, strengthening put skew, a billion-dollar put at $60,000 and negative cumulative volume delta all point the same way.

When spot sits this close to a heavily loaded strike, the market becomes reflexive. A move toward $60,000 can trigger hedging that pushes price further in the same direction, which can trigger more hedging. That feedback loop is why derivatives positioning often matters as much as headlines during fragile periods. It does not guarantee a drop, but it raises the stakes of every move.

What to Watch

The most important level to monitor is the $60,000 strike. If Bitcoin holds comfortably above it and open interest stabilizes, the pressure from that put cluster may ease without a violent reaction. If spot breaks below and the put open interest stays elevated, the resulting position adjustments could amplify volatility in both directions. Keep an eye on whether implied volatility keeps climbing or starts to cool, and watch the put skew for any sign that demand for downside protection is fading. A flip in cumulative volume delta back to positive would be an early hint that aggressive selling is exhausting itself.

Derivatives are high-risk instruments and the signals described here can shift quickly. This article is for informational purposes only and is not financial advice. Always do your own research and understand the risks before trading options or other leveraged products.