Uniswap v2 vs v3 vs v4: Differences for Liquidity Providers

Providing liquidity has transformed from passive indexing to algorithmic market making. We analyze the technical structural evolution across Uniswap v2, v3, and v4.

The Definitive Liquidity Provider Guide

- The architecture of decentralized exchanges has shifted from passive asset indexing to hyper-efficient, highly programmable capital management. As the pioneer of the Automated Market Maker (AMM) model, Uniswap has iteratively rewritten the rules of on-chain market making. For Liquidity Providers (LPs), each major version change represents a fundamental shift in capital efficiency, risk mitigation, and operational overhead.

- Deploying capital into the contemporary decentralized finance (DeFi) market requires a forensic understanding of how Uniswap v2, v3, and v4 alter your inventory risk and yield generation. This guide contrasts these three protocols from the perspective of a liquidity provider.

1. Inventory Architecture: From Passive Curves to Singletons

The physical deployment of assets across Uniswap's history shows an ongoing effort to reduce capital fragmentation and maximize storage efficiency on the blockchain ledger.

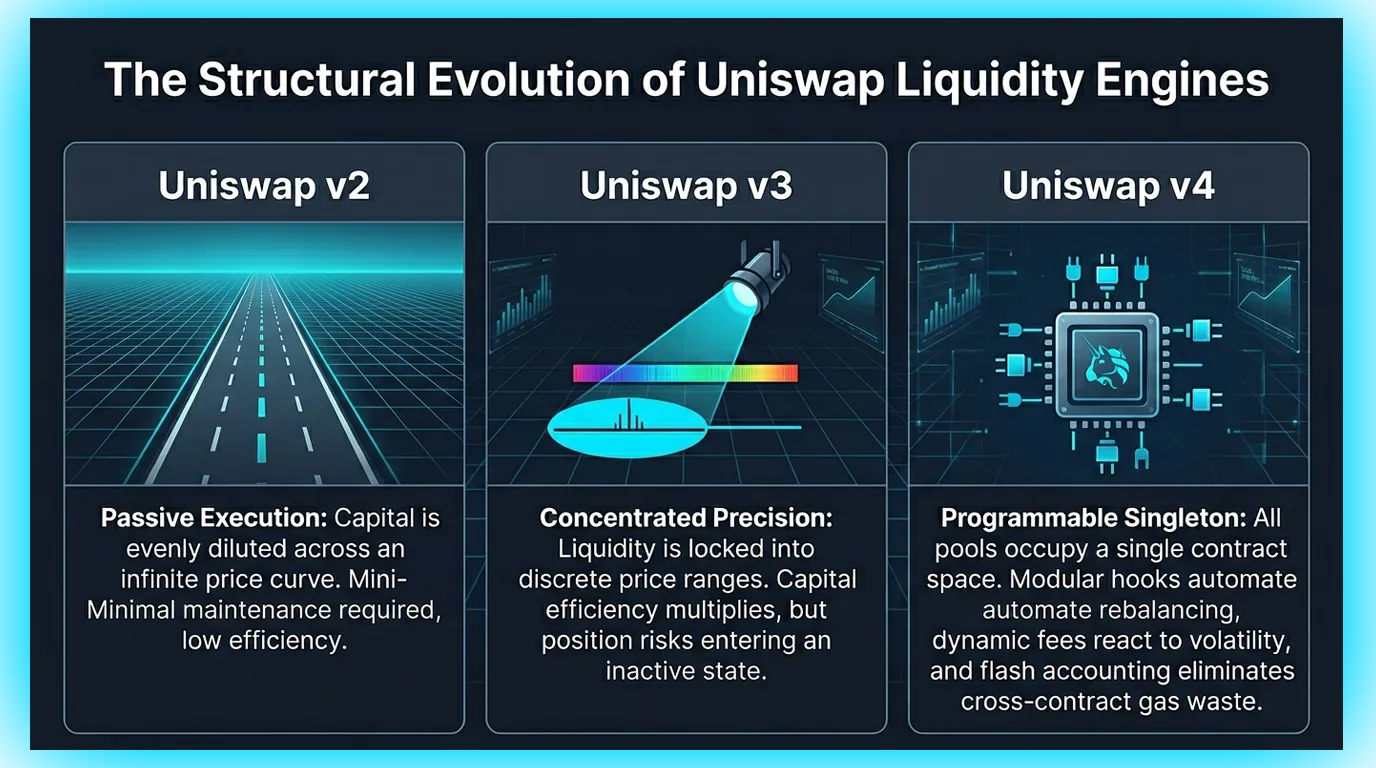

Uniswap v2: The Passive Uniform Standard

Uniswap v2 relies on a rigid constant product model. When an LP deposits capital into a v2 pool, the smart contract automatically distributes those tokens uniformly across an infinite price scale, spanning from zero to infinity.

The LP Experience: Absolute passivity. Once liquidity is deposited, it requires zero active management. The position can never go "out of range," meaning it continuously collects fees regardless of market direction.

The Capital Drawback: Extreme capital inefficiency. Because your liquidity is spread across every possible price point, only a tiny fraction of your deposited capital is actively used to facilitate swaps near the current market price. The rest sits idle.

Uniswap v3: Concentrated Liquidity Ticks

Uniswap v3 introduced concentrated liquidity, allowing LPs to bound their assets within distinct price ranges. The infinite price scale was divided into discrete mathematical intervals called "ticks."

The LP Experience: Market making transformed into an active, competitive strategy. LPs specify upper and lower price boundaries. Within that narrow window, their capital multiplier spikes, capturing substantially higher fee revenues per dollar deposited than v2.

The Operational Cost: If the market price moves completely outside an LP's custom boundaries, their position automatically becomes 100% inactive, shifting entirely into the depreciating asset of the pair and earning zero trading fees until manually rebalanced.

Uniswap v4: The Modular Singleton Engine

- Uniswap v4 preserves the concentrated liquidity mechanics of v3 but radically restructures the underlying smart contract environment. In previous versions, every distinct token pair required the execution of an independent smart contract deployed on-chain, creating severe gas overhead when routing trades across multiple pools.

- Version v4 consolidates all liquidity pools into a single, comprehensive contract called the PoolManager. Coupled with a flash accounting architecture, this singleton design eliminates the need to physically transfer tokens across multiple contract addresses during multi-hop trades. For LPs, this architecture reduces the cost of initializing new pools by up to 99%, while introducing native support for assets like Ethereum without requiring token wrapping.

2. Fee Tier Evolution and Customization

The monetization framework for providing liquidity has evolved from fixed global protocol rates to highly dynamic, programmatically adjusted pricing modules.

Uniswap v2: Enforces a rigid, unalterable 0.3% trading fee across every single pool deployment, offering no distinction between low-volatility stablecoins and highly volatile exotic assets.

Uniswap v3: Introduced four structured, static fee tiers: 0.01% for stablecoins, 0.05% for premier blue-chip assets, 0.30% for standard volatile pairings, and 1.00% for highly speculative long-tail tokens.

Uniswap v4: Removes static fee barriers entirely. Pool creators can define any baseline swap fee in precise fractions of a basis point. More importantly, v4 enables dynamic fees that adjust in real-time. Through custom programming extensions, a pool can automatically scale its swap fees upward during periods of hyper-volatility to extract higher premiums from toxic order flow, protecting LP margins when risk exposure peaks.

3. The Impermanent Loss (IL) Profile Shift

Impermanent loss represents the opportunity cost incurred when providing assets to a rebalancing pool rather than holding them passively in a private wallet. The risk trajectory of IL has scaled exponentially alongside the evolution of the protocol.

The Linear Curve of v2

Because v2 liquidity is spread uniformly across an infinite price scale, the impact of price divergence is slow, predictable, and manageable. Impermanent loss accumulates on a smooth curve, giving passive LPs extended time horizons to offset inventory divergence through steady fee accrual.

The Accelerated Leverage of v3

- Concentrating liquidity into narrow price brackets dramatically compounds your exposure to impermanent loss. Because your assets are localized within a tight window, a aggressive price breakout moves your position to 100% of the underperforming asset at an accelerated rate.

- In v3, narrow concentration acts as a leveraged bet on horizontal price action; if the market trends strongly in one direction, the sudden accumulation of IL can easily wipe out months of accumulated fee revenue.

The Programmable Mitigation of v4

While the mathematical baseline for impermanent loss in v4 matches the concentrated structure of v3, v4 introduces the infrastructure to programmatically fight IL on-chain. Through the deployment of lifecycle modifiers called Hooks, custom pools can automate risk mitigation strategies:

Auto-Rebalancing Hooks: Contracts can automatically adjust active price intervals based on external market data, preventing positions from sitting idle out-of-range.

MEV Internalization Hooks: Capture the arbitrage profits that predatory trading bots normally extract from pools during price movements, automatically redirecting those revenues back into the pool to compensate LPs.

Derivatives Hedging Hooks: Programmatically trigger options or perpetual short positions using pool assets to construct an automated hedge against directional price divergence.

4. Core Structural Comparison Matrix

| Operational Parameter | Uniswap v2 | Uniswap v3 | Uniswap v4 |

| Liquidity Distribution | Infinite Range (Uniform) | Concentrated Range (Custom Ticks) | Concentrated Range (Custom Ticks) |

| Smart Contract Layout | Factory Model (Separate Contracts) | Factory Model (Separate Contracts) | Singleton Model (Unified PoolManager) |

| Fee Configurations | Flat 0.3% | Static Tiers (0.01% to 1.00%) | Infinite Customization & Dynamic Fees |

| Operational State | Fully Passive | Active Management Required | Programmable Automation (Hooks) |

| Accounting Method | Traditional Settlement | Traditional Settlement | Flash Accounting System |

| Impermanent Loss Profile | Slow, Predictable Accumulation | Accelerated, High Concentration Risk | Accelerated Baseline, Mitigable via Hooks |

Disclaimer: This article is for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other kind of advice. DEXTools does not recommend buying, selling, or holding any cryptocurrency or token. Users should conduct their own research and consult with a qualified financial advisor before making any investment decisions. Cryptocurrency investments are volatile and high-risk. DEXTools is not responsible for any losses incurred.