Bank of America, Citi and Wells Fargo Plan Tokenized Deposit Network

— By Tony Rabbit in Markets

Bank of America, Citi, Wells Fargo and JPMorgan plan a shared tokenized deposit network via The Clearing House, targeting an early 2027 launch.

A consortium of major U.S. banks, including Bank of America, Citigroup, Wells Fargo and JPMorgan, plans to build a shared tokenized deposit network operated by The Clearing House, with a launch targeted for the first half of 2027. The effort aims to connect traditional bank rails with blockchain so member institutions can move tokenized customer deposits 24 hours a day, seven days a week, with instant settlement. According to reporting from The Block and Cryptopolitan, more than a dozen lenders have signed on, in what observers describe as Wall Street's most coordinated answer yet to the rise of stablecoins.

What the banks are building

The plan would let participating banks issue digital tokens that represent customer deposits and settle them across blockchain infrastructure. Unlike the slow batch processing of legacy systems such as ACH or wire transfers, the network is designed to clear payments around the clock, eliminating the hours or days of delay that typically follow a transaction. The Clearing House, a bank-owned payments company that already processes a large share of U.S. interbank transfers, would operate the system.

Per coverage from PYMNTS and Crypto Briefing, no blockchain vendor has been selected yet and the technical specifications remain under development. Some banks have reportedly referred to the project internally as "the bridge" and others as "the chain." The Clearing House CEO David Watson called it "a big move for the banks," framing the initiative as a response to a payments landscape he described as "radically different."

Which banks are involved

Beyond the four largest names, the group reportedly includes a broad set of regional and global lenders. Coverage from The Defiant and Unchained lists participants such as BNY, BMO, Citizens Financial, Fifth Third, HSBC, Huntington, KeyBank, PNC, Regions, Santander, TD Bank, Truist and U.S. Bank, alongside the four anchor institutions. That breadth matters: a tokenized deposit is only useful across the wider economy if many banks can recognize and settle one another's tokens, which is why a shared, neutral operator like The Clearing House is central to the design.

The effort builds on earlier single-bank experiments. JPMorgan, for example, developed an internal token for moving funds between its own accounts, and Citi has worked on integrating tokenized deposits with its clearing services for cross-border payments. The new network extends that idea across many institutions so the tokens can travel between banks rather than staying inside a single firm.

How tokenized deposits differ from stablecoins

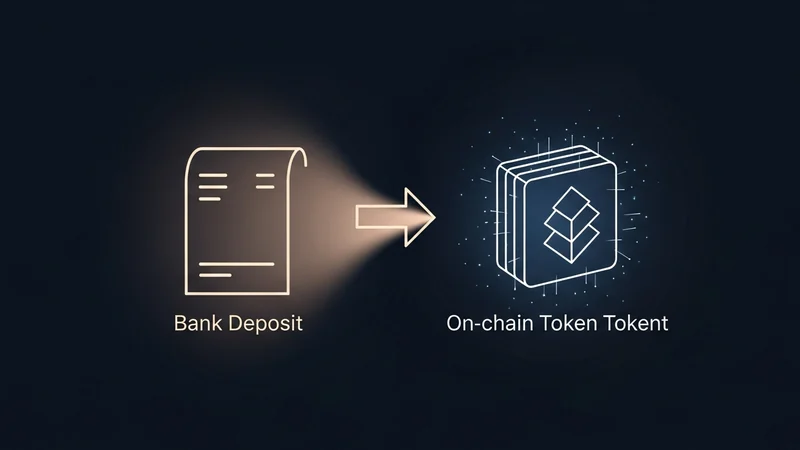

The distinction is at the heart of the project. Tokenized deposits are digital representations of money held in a regulated commercial bank. They carry the same credit-risk profile, regulatory treatment and accounting standards as ordinary deposits, and they stay inside the banking system with deposit insurance protections intact. They are account-based, meaning the bank still tracks who owns what.

- Tokenized deposits: commercial bank money on a blockchain, issued by federally regulated banks, account-based, and tied to existing deposit relationships.

- Stablecoins: typically issued by non-bank entities, backed by reserves such as short-term U.S. Treasury bills, and structured as bearer instruments where holding the token equals ownership.

According to analysis published by the Brookings Institution, stablecoins function more like digital cash, while tokenized deposits behave like a faster, programmable version of a bank transfer. Both can settle on-chain, but tokenized deposits aim to deliver that speed without moving money out of the regulated banking sector.

Market context after the GENIUS Act

The timing reflects a broader push by traditional finance into blockchain settlement. In July 2025, the United States enacted the GENIUS Act, the first federal framework for payment stablecoins. Crucially, the law's definition of a payment stablecoin excludes deposits, including tokenized deposits issued by banks. That carve-out leaves banks free to issue tokenized deposits without falling under the stablecoin rulebook, while non-bank stablecoin issuers operate under the new reserve and disclosure requirements.

The result is a competitive split. Stablecoins have grown into a fast, 24/7 settlement option that does not rely on traditional banking hours, and banks see a risk of deposits migrating toward crypto-native rails. The Clearing House network is, in part, a defensive move: a way for banks to offer comparable speed and programmability while keeping funds, and the lending those funds support, inside the regulated system.

What it means for the market

The Clearing House expects large multinational corporations to be the earliest adopters, with use cases spanning programmable treasury operations, real-time liquidity management and cross-border payments. Executives have been candid about demand timing. Bank of America's Mark Monaco acknowledged that clients are not currently "beating down the door" for tokenized deposits, while Citigroup's Shahmir Khaliq said the network "cements" the role of banks in financing and capital markets.

For the wider digital asset market, a bank-run settlement layer could blur the line between traditional payments and on-chain finance. As more value moves across public and private chains, traders and analysts often watch where activity concentrates. On-chain assets, token liquidity and trading pairs can be tracked on DEXTools, which gives a real-time view of decentralized market activity that runs in parallel to these institutional settlement efforts.

What is next

Several pieces remain unsettled. The group has not chosen a blockchain, the technical standards are still being written, and interoperability between tokenized deposits issued on different platforms is an open engineering question. Regulators will also weigh in on how these tokens interact with existing payment and settlement oversight. With a target window in the first half of 2027, the banks have given themselves time to resolve those questions before any rollout.

For now, the announcement signals intent rather than a finished product. It places the largest U.S. lenders firmly in the contest over the future of money movement, positioning bank-issued tokens as a regulated alternative to stablecoins while the underlying infrastructure takes shape over the coming year.