Buyback and Burn vs. Buyback and Distribute Explained

Native protocol revenues are useless without an optimized distribution architecture. We pull back the curtain on how top-tier networks manage their cash flows, manipulate liquid float, and signal macro health to the market.

The Capital Allocation Imperative: Corporate Finance Re-Engineered for Web3

- In the traditional corporate landscape, the accumulation of net corporate earnings triggers a standard, boardroom-driven question: How should excess cash flows be returned to equity holders? Executives evaluate the macroeconomic landscape to decide between issuing direct, cash-settled dividends or executing open-market share repurchases. Dividends offer immediate, visible cash flow to investors, while share buybacks reduce the outstanding share count, programmatically boosting the fractional ownership share and earnings metrics of every remaining stock unit.

- Inside permissionless, decentralized networks, this core financial problem undergoes a profound cryptoeconomic transformation. Web3 protocols operate as software-driven corporate entities, capturing substantial top-line revenues from transactional gas fees, interest-rate spreads on lending primitives, liquidation penalties, and real-world asset yields. However, simply generating protocol revenue is not enough to sustain a digital economy. Without an optimized, hardcoded value-capture primitive embedded into the core smart contract layer, accrued platform earnings sit stagnant inside multi-signature treasuries, disconnected from the native utility token.

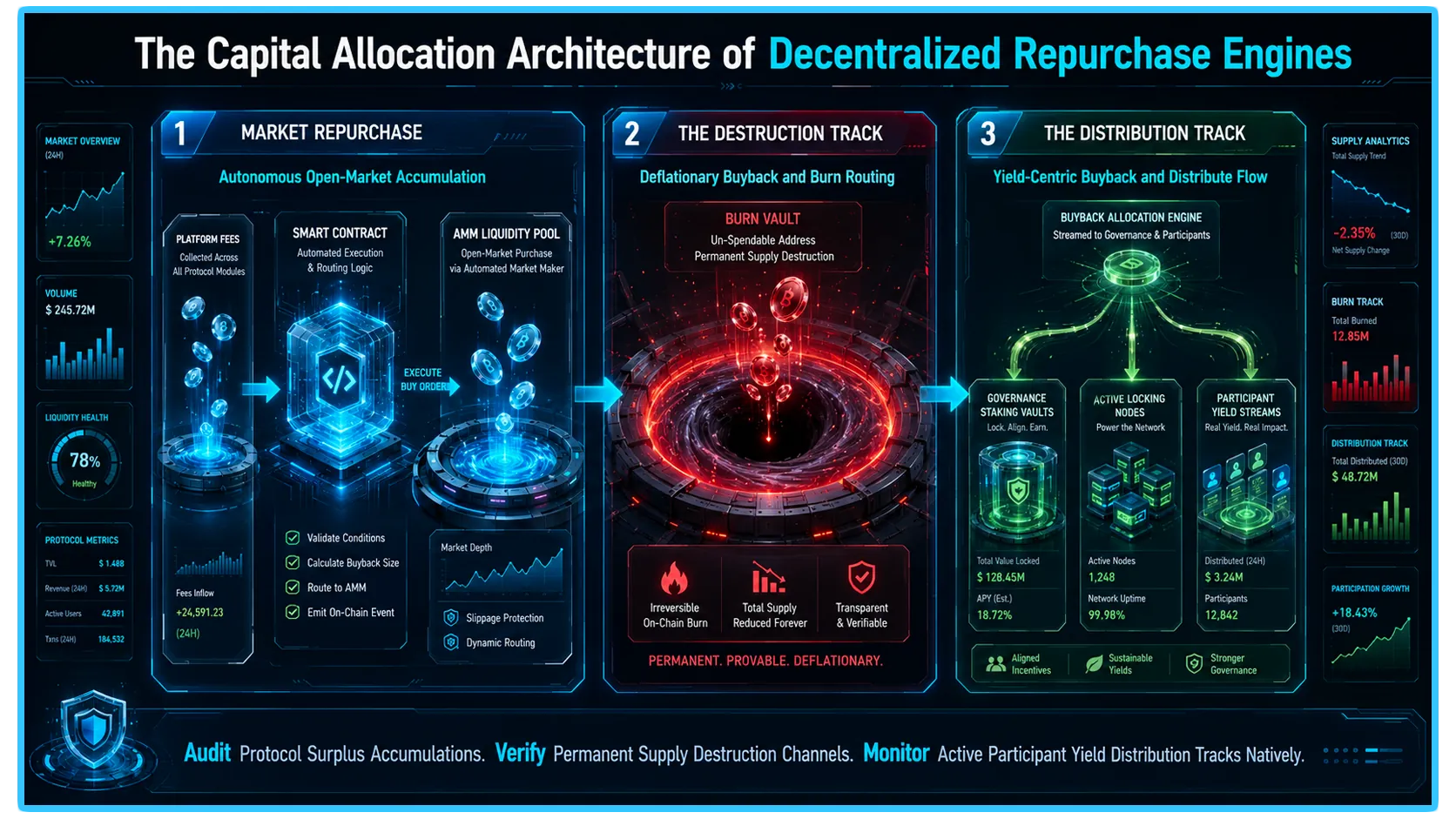

- To bridge this operational gap, token engineers deploy automated repurchase frameworks. Mastering the underlying crypto token supply dynamics requires analyzing how these capital streams are routed once they enter the open market. The two primary mechanisms used to align treasury cash flows with investor value are Buyback and Burn and Buyback and Distribute. Choosing which model to deploy across a specific protocol architecture is not a superficial choice; it changes the network's liquid float, dictates its systemic regulatory profile, shapes investor psychology through powerful market signaling, and alters the game-theoretic incentives of all community participants.

1. Buyback and Burn: The Pure Deflationary Engine

The Buyback and Burn model operates as the pure, un-falsifiable deflationary engine of decentralized application design. Its core functional purpose is to link the protocol’s ongoing commercial success directly to asset scarcity by permanently and systematically extracting supply from the open market.

The Mechanics of the Deflationary Pipeline

- The operational pipeline of a buyback-and-burn mechanism is completely governed by autonomous smart contracts, removing human bias and boardroom delays from the capital allocation process.

- First, the application accumulates gross protocol revenues in various base assets, such as decentralized stablecoins or layer-1 gas tokens. Once this treasury surplus crosses a pre-set threshold defined by governance parameters, the protocol's automated scripts initialize an execution command.

- Second, the smart contract routes these captured revenues straight into open-market liquidity venues, placing automated market buy orders within decentralized automated market makers or centralized limit order books. The engine acts as a continuous, price-insensitive buyer, absorbing liquid supply straight off the market.

- Third, rather than storing these acquired tokens inside a corporate treasury vault where they could potentially be re-issued, the smart contract routes the purchased assets directly to an un-spendable, dead cryptographic address. This process permanently alters the total token supply registry, guaranteeing that the destroyed units can never re-enter circulation or be used as market collateral.

The Market Signaling of Permanent Extinction

In the broader market microstructure, executing a buyback-and-burn model broadcasts a highly potent, institutional signal to the investment landscape:

The Scarcity Multiplier: By permanently destroying tokens, each remaining liquid token in circulation captures a larger proportional share of the underlying protocol's future growth and governance control. It creates a structural wealth redistribution effect that rewards all token holders equally, regardless of whether they own ten tokens or ten million.

The Continuous Bidding Cushion: Because the smart contract executes buy orders systematically based on platform revenue velocity, it injects a constant layer of non-emotional bid depth into the order book. During volatile market downcycles, this continuous revenue-linked buying pressure serves as an essential structural cushion, stabilizing the asset's spot price against speculative short-selling cascades.

2. Real-World Case Studies: The Evolution of BNB and MakerDAO (Sky)

To observe how buyback-and-burn frameworks adapt under real-world economic stress, we must analyze the operational lifecycles of two industry standards: the BNB Chain ecosystem and MakerDAO’s recent transition into Sky.

BNB: From Manual Corporate Repurchases to On-Chain Auto-Burns

- When BNB launched in 2017, its whitepaper established a corporate buyback-and-burn model modeled after traditional stock buybacks. Every quarter, the centralized Binance exchange calculated its net corporate profits and committed twenty percent of those earnings to manually repurchase and destroy BNB tokens, aiming to cut the total supply down to a maximum cap of one hundred million.

- While this manual model successfully removed millions of tokens from circulation, it faced significant technical criticism regarding transparency and centralization. To eliminate human intervention, the ecosystem implemented a comprehensive overhaul, transitioning to a fully automated system.

- Today, the asset's supply contraction is driven by a programmatic Auto-Burn system. This on-chain mechanism ignores centralized corporate revenue reporting entirely. Instead, it utilizes an objective software script that automatically calculates the precise number of tokens to destroy every quarter by processing two live variables: the average market spot price of BNB and the total number of blocks successfully generated during that horizon.

- This model introduced an innovative economic stabilizing function: if the market price of the token experiences a significant downward drop, the programmatic calculation automatically scales the number of tokens to be burned upward. This auto-balancing feature injects an aggressive deflationary cushion exactly when the ecosystem requires structural support. This auto-balancing feature injects an aggressive deflationary cushion exactly when the ecosystem requires structural support.

- Complementing this quarterly contraction is the BEP-95 upgrade, which introduces an unyielding, transaction-based destruction layer. Operating directly inside the Proof-of-Staked-Authority consensus engine, BEP-95 mandates that a fixed ratio of the gas fees collected within every single block is instantly routed to a dead address, completely bypassing validator payout pools. This ensures that even during periods of sideways market consolidation, high dApp utility, opBNB Layer 2 traffic, and on-chain transactional volume actively drive permanent asset scarcity second by second.

MakerDAO (Sky): Surplus Auctions and the Smart Burn Engine

- MakerDAO pioneered decentralized credit generation through the minting of overcollateralized DAI stablecoins. The protocol’s native value-capture engine was historically anchored to a programmatic Surplus Auction (Flap Auction) framework.

- The system’s financial plumbing routes all platform cash flows (generated by stability fees charged to borrowers and yields harvested from real-world asset treasuries) directly into a central repository known as the Maker Buffer. The buffer acts as a defensive equity shield designed to absorb bad protocol debt during volatile market liquidations.

- Under the protocol's baseline logic, the moment the capital sitting inside the Maker Buffer exceeds a hardcoded governance threshold, the excess system surplus is immediately deployed to fund public surplus auctions. The protocol sells this excess DAI to the market in exchange for MKR tokens, which are instantly and permanently burned by the system contract, linking DAI credit expansion directly to MKR scarcity.

- Entering recent market regimes, MakerDAO executed a historic structural rebranding, evolving into the Sky Protocol. This transition introduced a highly advanced optimization layer known as the Smart Burn Engine. Moving past the legacy periodic auction design, the Smart Burn Engine deploys system surplus capital continuously on a daily basis to systematically acquire and destroy tokens off the open market, actively balancing new ecosystem reward emissions and locking down a highly resilient macroeconomic value-capture track for all participants.

3. Buyback and Distribute: The Yield-Centric Cash Flow Framework

While the buyback-and-burn framework focuses on driving asset value through passive, vertical supply contraction, the Buyback and Distribute model focuses on driving active user engagement through immediate, visible cash flow rewards.

The Mechanics of the Distribution Loop

- The initial stages of the buyback-and-distribute pipeline mimic the burn model: the protocol aggregates its operational revenues and executes automated market buy orders to purchase its native token straight off public exchanges. However, the exact millisecond the tokens clear the execution matching engine, the technical routing pathway diverges completely.

- Instead of transmitting the repurchased tokens to a dead blackhole address, the smart contract routes the newly acquired asset cache into a designated Distribution Pool. These tokens are then systematically streamed back to specific subsets of the user base who have actively committed their own capital to secure the network, such as governance stakers, long-term liquidity providers, or ecosystems lockers.

The Psychology of Real Yield Signaling

By maintaining a constant supply loop rather than destroying tokens, the buyback-and-distribute architecture project a completely alternative behavioral and financial signal to the market:

The Cash Flow Incentive: Investors frequently display a psychological preference for tangible, visible cash flows (Real Yield) over the abstract promise of passive price appreciation through deflation. Receiving a steady, compounding stream of native tokens directly into a staking vault satisfies the investor's desire for income, matching the cash flow expectations found in traditional real estate or dividend-paying equities.

Sustaining the Liquid Float: Because tokens are redistributed and recycled rather than destroyed, the total maximum supply cap of the asset remains completely unchanged. This prevents the protocol from experiencing extreme liquidity starvation, ensuring that an adequate volume of liquid floating supply remains available across secondary exchanges to facilitate orderly market-making and deep trading depth.

Capital Allocation Structural Matrix

| Structural Attribute | Buyback and Burn Model | Buyback and Distribute Model |

| Primary Economic Axis | Absolute Supply Scarcity Contraction | Direct Cash Flow Yield Redistribution |

| Total Supply Impact | Permanently and Irreversibly Decreased | Remains Completely Static and Constant |

| Target Recipient | Every token holder captures value passively | Exclusively rewards active stakers/lockers |

| Market Microstructure Role | Shrinks the liquid order book float over time | Stablizes float while incentivizing retention loops |

| Primary Risk State | Ineffective if price drops on flat volume | High sell pressure if stakers dump rewards |

4. Strategic Trade-offs: Game Theory and Value Accrual

Choosing between these two structural architectures requires a protocol's governance cabinet to balance complex game-theoretic trade-offs and market conditions.

The Passive Holder vs. Active Staker Dilemma

- The buyback-and-burn model is inherently egalitarian: it rewards every single participant who holds the token in their wallet, requiring zero gas expenses, staking lockup commitments, or active governance voting management. This simplicity makes it a highly attractive framework for passive retail investors and large macro funds who want to hold an asset cleanly inside cold storage hardware wallets.

- The buyback-and-distribute model, conversely, intentionally discriminates against passive holders. If a protocol repurchases tokens and routes them exclusively to a staking vault, any participant who chooses to leave their tokens liquid on an exchange experiences continuous, fractional dilution of their governance weight and network ownership. This structure is explicitly engineered to force token velocity into long-term lockup channels, compelling the community to actively participate in the day-to-day security and management of the network.

5. Live Telemetry Auditing via DEXTools

- Even when keeping your keys safe offline inside hardened hardware setups, real-time volume validation remains vital for tracking protocol cash flows. DEXTools delivers essential live metrics to monitor decentralized liquidity pools, evaluate bid-ask depth, trace large whale reallocations, and run contract security scans via tools like the Pair Explorer, Big Swap Explorer, and Live New Pairs tracker.

- This structural transparency ensures your wallet interacts exclusively with verified, liquid market venues while your primary positions rest fully insulated from unexpected market anomalies.

Disclaimer: This article is for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other kind of advice. DEXTools does not recommend buying, selling, or holding any cryptocurrency or token. Users should conduct their own research and consult with a qualified financial advisor before making any investment decisions. Cryptocurrency investments are volatile and high-risk. DEXTools is not responsible for any losses incurred.

Revenue Concentration vs Revenue Diversity: Why One Income Stream Can Make Protocols Fragile Liquidation Volume vs Bad Debt in DeFi Lending Token Transfer Velocity vs Holder Retention: What Shows Real Conviction? Loan Origination vs Outstanding Debt: Which Shows Real Lending Growth?