Crypto Cost Basis method: FIFO vs. Specific ID

The era of global token pooling is officially dead. We break down the structural shifts, pre-identification mandates, and accounting metrics governing post-2025 crypto taxes.

Crypto Cost Basis Methods Explained: FIFO vs. Specific ID After the Wallet Rule

- The methodology governing decentralized asset tax sub-accounting has experienced its most aggressive structural overhaul since the inception of the digital asset class. For years, crypto traders and decentralized finance (DeFi) participants utilized a highly convenient accounting assumption known as universal pool tracking.

- Under this legacy framework, an investor could aggregate all identical tokens held across a global matrix of separate exchange accounts, hardware wallets, and web3 interfaces into a single, centralized data queue. When liquidating an asset, the tax engine could programmatically "reach across" the entire portfolio to pull the most mathematically advantageous historical purchase lot, regardless of where the physical transaction physically occurred.

- The finalization of Treasury Regulation completely terminated this practice. Enforced as the mandatory per-wallet cost basis rule, the IRS officially banned universal pool tracking. Moving forward, the open financial ledger is treated as a series of completely isolated data silos. Each individual exchange account, hardware address, and institutional custodial vault must maintain its own fully independent tax lot queue.

- As a result, your chosen Crypto Cost Basis Method no longer evaluates your global net wealth: it executes strictly within the isolated walls of the specific container where your asset disposal occurs. This technical guide contrasts the mechanics of First-In, First-Out (FIFO) against Specific Identification (Specific ID) under this strict localized accounting regime.

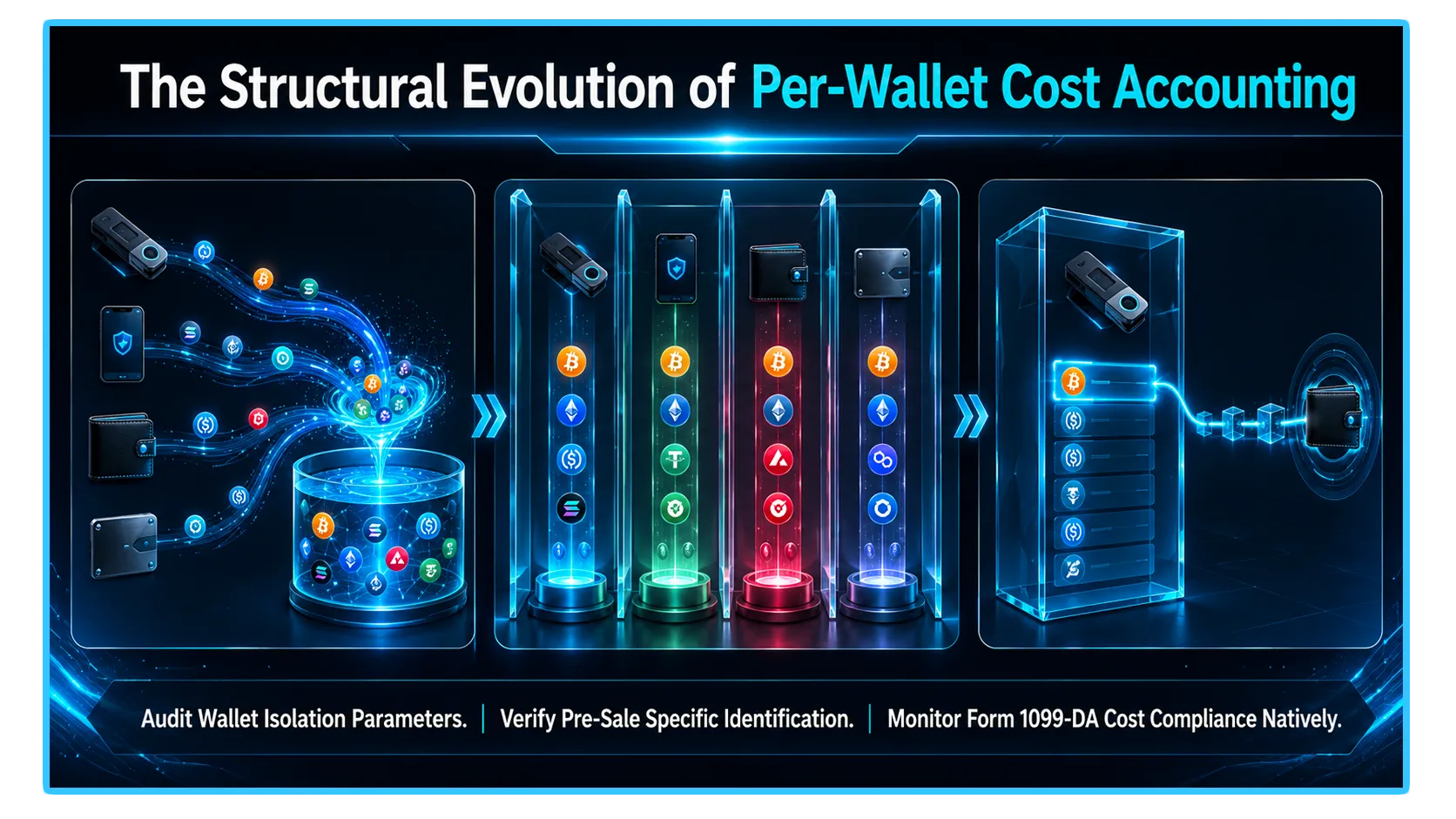

1. The Structural Shift: Universal Pooling vs. Per-Wallet Isolation

- To evaluate modern tax liability with quantitative precision, you must first visualize the operational separation mandated by the new regulatory framework.

- Under the old pooling regime, if you purchased 1 Bitcoin on Coinbase for $20,000, another on Kraken for $60,000, and later sold 1 Bitcoin on Kraken for $70,000, your software could pair the Kraken sale with the Coinbase purchase lot. This minimized your realized capital gain down to $50,000, despite the assets residing on separate ledgers.

- Under the per-wallet rule, this cross-ledger pairing is completely illegal. Because the liquidation occurred on Kraken, you are forced to match the transaction exclusively against the cost basis lots natively native to that specific Kraken account. Your Coinbase purchase lot remains locked and completely inaccessible for matching unless a physical, documented on-chain asset migration was executed between the platforms prior to the trade. Whichever matching calculation you choose must be calculated entirely within localized account queues.

2. First-In, First-Out (FIFO): The Default Multi-Chain Baseline

First-In, First-Out (FIFO) stands as the baseline default method mandated by the IRS if a taxpayer fails to adequately satisfy the strict criteria required to implement a more complex optimization strategy.

The Localized FIFO Mechanism

FIFO operates under the rigid chronological assumption that the oldest units of an asset accumulated within a specific account are the absolute first units liquidated upon a disposal.

The Upward Market Trend Trap: In a prolonged, multi-year bull market, FIFO typically yields the largest immediate taxable capital gains. Because your oldest historical lots are usually your cheapest acquisition points, pairing them against current open-market rates maximizes the visible profit spread.

The Long-Term Capital Gains Silver Lining: While FIFO often inflates the raw size of your taxable gain, it accelerates your transition into long-term capital gains classification. If the oldest localized lot was held continuously within that specific account for more than 365 days, the transaction qualifies for lower tax brackets (0%, 15%, or 20%), frequently offsetting the nominal gain expansion.

3. Specific Identification (Specific ID): The Precision Steering Wheel

- For advanced allocators seeking complete control over their tax liability, Specific Identification (Specific ID) functions as the ultimate portfolio steering wheel. Specific ID permits the taxpayer to manually select the exact historical purchase lot they wish to pair against a specific disposal, provided they maintain meticulous ledger-level tracking.

- Through Specific ID, traders can automate advanced financial engineering substrates like Highest-In, First-Out (HIFO). In a high-volume trading environment, selecting your highest-cost purchase lots to match against sales allows you to minimize your immediate capital gains (or maximize your realized capital losses), preserving active working capital on your balance sheet.

The Crucial Pre-Identification Mandate

- The implementation of Specific ID comes with a major regulatory catch. Historically, traders could deploy Specific ID retroactively, waiting until the end of the tax year to run data simulations and cherry-pick optimal lots long after the trades had settled.

- The current framework permanently bans retroactive identification. To legally utilize Specific ID, the specific asset lots being disposed of must be identified at or before the exact time of the sale or transfer.

- You must explicitly instruct your exchange interface, programmatic trading script, or internal ledger tracking system which lot is being liquidated before the transaction completes. If you fail to pre-identify the lot and record the documentation contemporaneously, the IRS can invalidate your custom optimization and force-revert your entire account history to standard FIFO matching.

4. The Transition Bridge: Revenue Procedure 2024-28

- Because millions of legacy investors possessed historically pooled data gaps moving into this rigid regime, the IRS provided a vital, one-time transition safe harbor known as Revenue Procedure 2024-28.

- This procedure granted taxpayers the legal authority to systematically disassemble their historical, universal cost pools and distribute their unused basis lots among their active physical wallets and exchange accounts as of January 1, 2025.

- Taxpayers were permitted to utilize any reasonable allocation method, such as mapping their lowest-cost basis lots to their highest-balance cold storage wallets to preserve them for long-term holding. This safe harbor migration window was required to be fully completed and documented before the formal filing of the 2025 tax return.

- Once this allocation threshold passes, your historical wallet baselines are officially locked. Moving forward, the only method to migrate basis between independent wallets is through a physical, on-chain asset transfer, with the specific cost basis lot carrying over atomically alongside the token.

5. Summary Matrix: FIFO vs. Specific ID

To conceptualize the strategic trade-offs between the two primary accounting frameworks, we can analyze their core operational properties side-by-side:

| Accounting Dimension | First-In, First-Out (FIFO) | Specific Identification (Specific ID) |

| IRS Classification Status | Statutory Default Baseline | Permissible Optimization Paradigm |

| Execution Timing Window | Automated; requires zero real-time input | Mandatory; must pre-identify at time of trade |

| Record-Keeping Complexity | Minimal (Chronological ledger queue) | High (Contemporaneous lot-level documentation) |

| Immediate Tax Exposure | Generally higher in ascending macro trends | Generally minimized via HIFO selection |

| Holding Period Velocity | Prioritizes long-term tax bracket graduation | Variable; driven by your specific lot choices |

6. On-Chain Diagnostics and Verification via DEXTools

- Formulating an institutional-grade tax strategy under a strict per-wallet mandate requires look-through visibility into live, multi-chain liquidity data. While centralized brokerages track internal database transactions to generate Form 1099-DA proceeds reports, independent verification of your raw, historical execution price ticks across decentralized applications is the only method to defend your custom Specific ID lot selections during a federal audit.

- DEXTools provides the critical analytical infrastructure needed to monitor these movements in real-time. By utilizing advanced pair tracking, historical block order visualization, and comprehensive wallet telemetry across alternative layer-1 and layer-2 networks, market participants can independently verify that their documented cost basis matches real-world historical market depth.

- Ensuring that your localized sub-accounting systems are aligned with authentic on-chain telemetry protects your portfolio from arbitrary zero-basis assumptions, keeping your capital highly efficient under the modern regulatory paradigm.

Disclaimer: This article is for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other kind of advice. DEXTools does not recommend buying, selling, or holding any cryptocurrency or token. Users should conduct their own research and consult with a qualified financial advisor before making any investment decisions. Cryptocurrency investments are volatile and high-risk. DEXTools is not responsible for any losses incurred.