Crypto Tax Loss Harvesting: Sell Low, Rebuy Legally

Market drawdowns don't have to mean portfolio decay. We break down the structural, statutory, and compliance frameworks to turn your crypto paper losses into massive tax write-offs.

Crypto Tax Loss Harvesting: How to Sell at a Loss and Rebuy Legally

- The hyper-volatility of cryptocurrency is traditionally framed as its greatest operational hazard. However, for sophisticated capital allocators, sharp market drawdowns present a highly powerful corporate finance optimization strategy. When token values contract, everyday investors see portfolio decay, but tax-conscious traders see an aggressive opportunity to manufacture tax deductions. This process is known as Crypto Tax Loss Harvesting.

- In traditional equities and options markets, selling an asset to lock in a tax write-off and immediately buying it back is strictly prohibited by the IRS's 61-day wash sale rule. Attempting this maneuver with stocks results in an automatically disallowed deduction.

- In the spot digital asset ecosystem, the landscape is entirely different. Because the regulatory architecture treats cryptocurrencies under alternative tax rails, traders can legally sell an underperforming token asset to realize a paper loss and repurchase it shortly after. This guide breaks down the underlying statutory exemptions, step-by-step execution workflows, and vital compliance boundaries defining tax-loss optimization frameworks.

1. The Underlying Machinery: How Capital Losses Rebalance Your Ledger

Before executing a harvest, you must understand the financial accounting mechanics that dictate how a realized loss impacts your broader tax liability. A loss only carries structural utility if it is cleanly executed to offset alternative taxable income blocks.

The IRS segments capital events into short-term (assets held for 12 months or less) and long-term (assets held for more than one year) categories. When you harvest a loss, the tracking occurs across a strict sequence:

Unlimited Capital Gains Offset: Realized capital losses can be used to offset an unlimited amount of capital gains within the same tax year. Crucially, crypto losses are fully fungible across asset classes: meaning a loss generated from trading Solana or Ethereum can be used to completely wipe out taxable gains accrued from selling traditional stocks, real estate, or private business equity.

Ordinary Income Deduction: If your total harvested losses exceed your total capital gains for the calendar year, you can deploy the remaining net loss to reduce up to $3,000 of ordinary income (such as your standard W-2 salary or self-employment revenue).

Indefinite Carryforwards: Any remaining net capital losses left over after neutralizing gains and applying the $3,000 ordinary income cap do not vanish. They are programmatically rolled over into future tax years as a "carryforward loss," remaining on your ledger indefinitely until they are fully absorbed by future market expansions.

2. The Legal Loophole: Why the Wash Sale Rule Doesn't Cover Spot Crypto

The primary question raised by traditional wealth managers is how a trader can legally buy back an asset immediately after selling it for a tax write-off. The answer lies within the strict statutory definitions of Internal Revenue Code (IRC) Section 1091.

Section 1091 dictates that if an investor sells a "stock or security" at a loss and acquires a "substantially identical" stock or security within a 30-day window before or after that sale, the loss is disallowed and pushed into the cost basis of the new position.

The Property Exemption: The IRS explicitly classifies virtual currency as property, not as stock or securities (per IRS Notice 2014-21). Because the literal text of Section 1091 is confined exclusively to stocks and securities, general property asset classes fall entirely outside its jurisdiction.

Consequently, there is no mandatory 30-day waiting period enforced on spot digital assets. You can legally dispose of an underwater cryptocurrency position to convert a paper loss into a realized, tax-deductible event, and immediately re-enter the position to preserve your long-term market exposure.

3. The Step-by-Step Blueprint for Compliant Harvesting

Executing a tax-loss harvest requires methodical accounting sub-treatment to ensure that your cost basis reporting stands up to federal automated auditing algorithms.

The Optimization Workflow Sequence

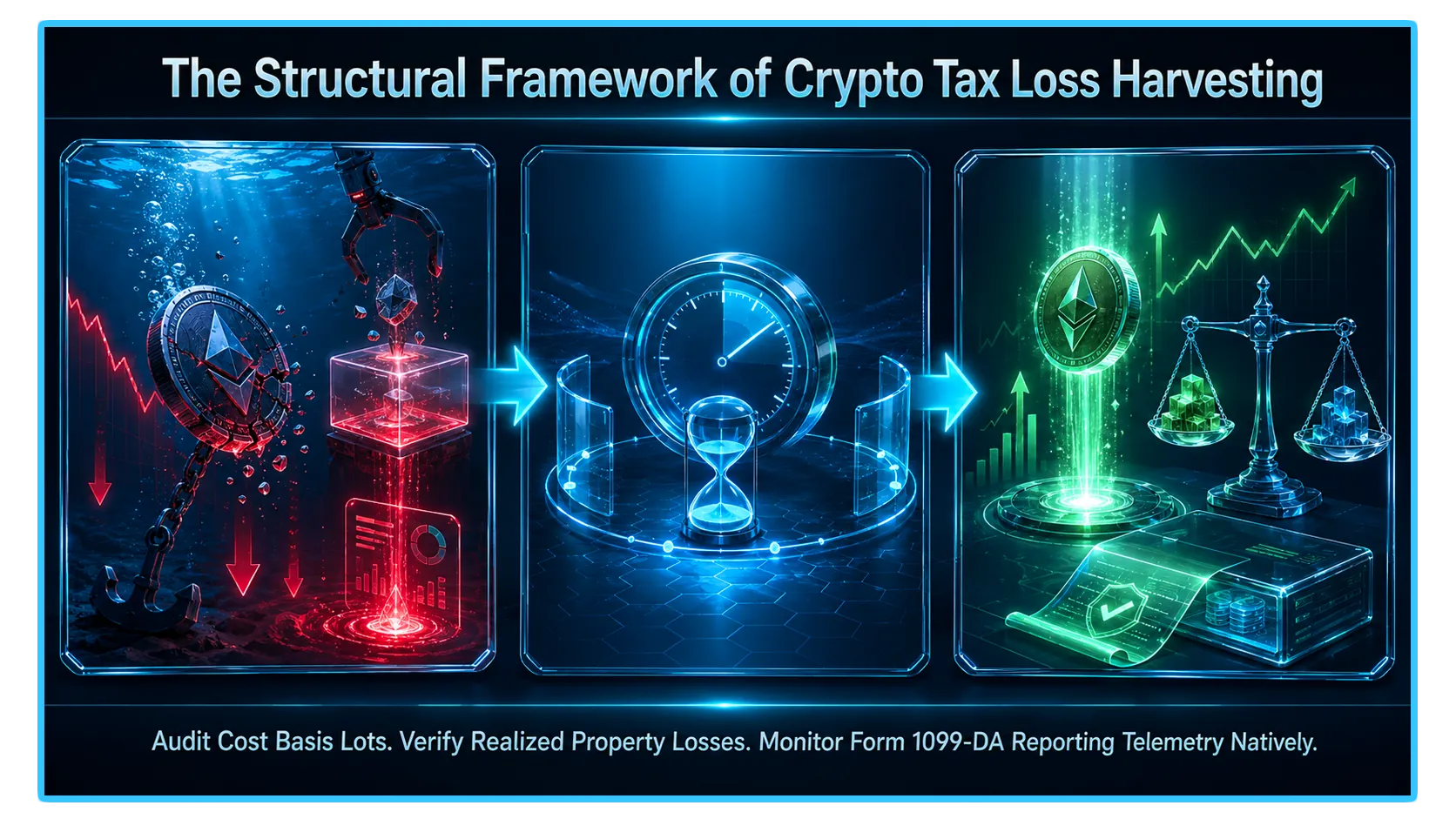

Step 1: Perform an Inventory Audit and Lot Analysis

A loss does not exist for the tax authorities when your chart turns red; it is only established upon execution of a taxable disposal. Review your multi-wallet and exchange infrastructure using specialized crypto tax software (such as CoinLedger or TokenTax) to isolate positions currently trading below your original acquisition cost basis.

Step 2: Utilize Highest-In, First-Out (HIFO) Matching

If you have accumulated an asset like Bitcoin across multiple price tiers over several years, you must designate your accounting lot selection framework. To maximize the size of your harvest, select Highest-In, First-Out (HIFO) or Specific Identification. This matching criteria ensures that when you execute a partial sale, the engine programmatically disposes of the specific units you purchased at the absolute peak of the market, maximizing the resulting capital loss deduction.

Step 3: Complete the Disposal

Execute a clean market or limit order to sell the underperforming token into a fiat stablecoin (like USDT or USDC) or a core pairing asset. This transaction locks in the realized capital loss. Save the digital receipt, fee metrics, and exact blockchain transaction hash.

Step 4: Re-Enter the Position with Strategic Friction

Once the sale finalizes and the loss is crystallized on the ledger, you can deploy your capital to repurchase the token. However, while an immediate same-second rebuy is technically allowed under Section 1091, navigating contemporary audit profiles requires the implementation of strategic friction (detailed below).

4. Modern Compliance Boundaries: Form 1099-DA & The Economic Substance Doctrine

The absolute property exemption under Section 1091 does not mean crypto trading operates inside a lawless vacuum. The regulatory framework features highly advanced tracking systems designed to penalize aggressive or manipulative tax avoidance strategies.

The Form 1099-DA Transparency Layer

- Centralized exchanges and hosted digital asset brokers report transaction data directly to the IRS using Form 1099-DA.

- Form 1099-DA delivers absolute transparency to federal audit networks, logging the precise timestamps, cost bases, and gross proceeds of your asset disposals. This structural data matching means that attempting to forge trade records or hide multi-wallet arbitrage flows will instantly flag an account for manual tax review.

The Economic Substance Shield

The greatest legal hazard facing a high-velocity tax harvester is the Economic Substance Doctrine (IRC Section 7701(o)). Under this doctrine, the IRS can unilaterally disallow any tax deduction if the transaction lacks a real, independent economic purpose outside of pure tax minimization.

The Automated Bot Trap: If a trader employs high-frequency automated API scripts to sell and buy back identical crypto positions within the exact same block transaction hundreds of times a day solely to manufacture paper losses, an auditor can argue the trade possessed no real economic risk and invalidate the entire deduction.

To guarantee your harvest remains legally unassailable, embed these protective parameters into your workflow:

Introduce Execution Windows: Do not execute the rebuy within milliseconds. Introduce a meaningful chronological buffer (such as waiting several hours or a full calendar day). This delay exposes your capital to real market volatility and execution risk, satisfying the economic substance requirement.

Deploy Correlated Proxies: Instead of buying back the exact same token signature, consider swapping the depreciated asset for a highly correlated alternative primitive. For instance, you can sell a liquid staking token like stETH at a loss and instantly purchase native ETH. You capture the tax write-off while maintaining virtually identical structural exposure to the underlying ecosystem.

5. The Asset Split: Spot Tokens vs. Crypto Securities

Allocators who manage wealth across both native Web3 interfaces and traditional brokerage accounts must track a strict compliance split. The property exemption exclusively covers spot digital assets. The moment your crypto exposure is wrapped inside a traditional financial security, it is pulled directly into the Section 1091 wash sale dragnet.

The Security vs. Property Tax Grid

| Asset Environment | Underlying Asset Wrapper | IRS Tax Classification | Wash Sale Status (Section 1091) |

| Spot Cryptocurrency | Direct on-chain tokens (BTC, SOL, ETH) | Property | Exempt (Losses allowed immediately) |

| Spot Crypto ETFs | Exchange-Traded Funds (e.g., IBIT, ETHA) | Security | Subject to Rule (Losses disallowed if bought within 61 days) |

| Crypto Equities | Public proxy stocks (e.g., MSTR, COIN, MARA) | Security | Subject to Rule (Losses disallowed if bought within 61 days) |

If you liquidate a Spot Bitcoin ETF or a proxy equity like MicroStrategy at a loss, you must wait a full 30 calendar days before repurchasing any shares of that same security, or the loss deduction will be legally disallowed and deferred.

6. Advanced Market Verification via DEXTools Telemetry

- Executing large-scale tax-loss harvesting maneuvers across highly volatile, decentralized asset classes requires deep, look-through visibility into live market microstructure. While an investor's internal portfolio dashboard tracks historical cost basis lot data, evaluating real-time order book depth, transaction velocity, and automated market maker (AMM) reserves on decentralized venues is the only method to execute major structural asset swaps without suffering destructive execution slippage.

- DEXTools provides the critical analytical data infrastructure needed to monitor these on-chain movements in real-time. By utilizing advanced pair tracking, cross-chain volume visualization, and large-scale whale wallet monitoring, market participants can instantly verify whether the specific liquidity pools they intend to harvest maintain sufficient depth to support immediate, low-slippage re-entries. Monitoring these real-time data metrics ensures your tax-loss maneuvers are executed against authentic economic substance, keeping your capital efficient and insulated from unexpected on-chain pricing anomalies.

You can access DEXTools here and start trading today!

Summary Checklist for Compliant Crypto Tax Loss Harvesting

Audit your portfolio to isolate token positions currently trading below their acquisition cost basis.

Configure your accounting matching settings to Highest-In, First-Out (HIFO) to maximize the loss size.

Complete the asset disposal on an exchange or decentralized application before December 31 to count for the current tax year.

Save the transaction hashes, cost basis logs, and receipts to reconcile against incoming Form 1099-DA broker statements.

Introduce a meaningful time delay or utilize a correlated proxy asset upon re-entry to robustly satisfy the Economic Substance Doctrine.

Disclaimer: This article is for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other kind of advice. DEXTools does not recommend buying, selling, or holding any cryptocurrency or token. Users should conduct their own research and consult with a qualified financial advisor before making any investment decisions. Cryptocurrency investments are volatile and high-risk. DEXTools is not responsible for any losses incurred.