NFT Taxation: Royalties, Sales, and Mints Explained

Digital collectible markets have evolved into complex financial ecosystems. We break down the taxable lifecycle of NFT mints, creator royalty accruals, and secondary market dispositions to ensure your crypto ledger remains compliant.

The Digital Ledger: Navigating NFT Tax Event Tracking

- In the rapid evolution of digital assets, Non-Fungible Tokens (NFTs) have transitioned from simple collectibles into complex financial vehicles that command significant valuation. As these assets are bought, sold, and traded across global decentralized marketplaces, tax authorities are sharpening their focus on the revenue flows generated by these digital collectibles. For the average participant, the intersection of blockchain-based ownership and jurisdictional tax law is often filled with ambiguity. Without a structured approach to NFT tax event tracking, many participants inadvertently expose themselves to significant compliance risks by failing to properly classify the different types of economic events occurring within their wallets.

- Unlike fungible tokens that trade against standardized pools, NFTs are unique property rights. This uniqueness dictates that each interaction (whether it is the initial "minting" of an asset, the collection of creator royalties, or a secondary market disposal) triggers a specific tax classification. To build a resilient financial strategy, you must view every smart contract interaction through the lens of a "taxable realization event." By establishing a robust cost basis for every digital asset and distinguishing between ordinary income (like royalties) and capital gains (from sales), you can maintain institutional-grade tax hygiene.

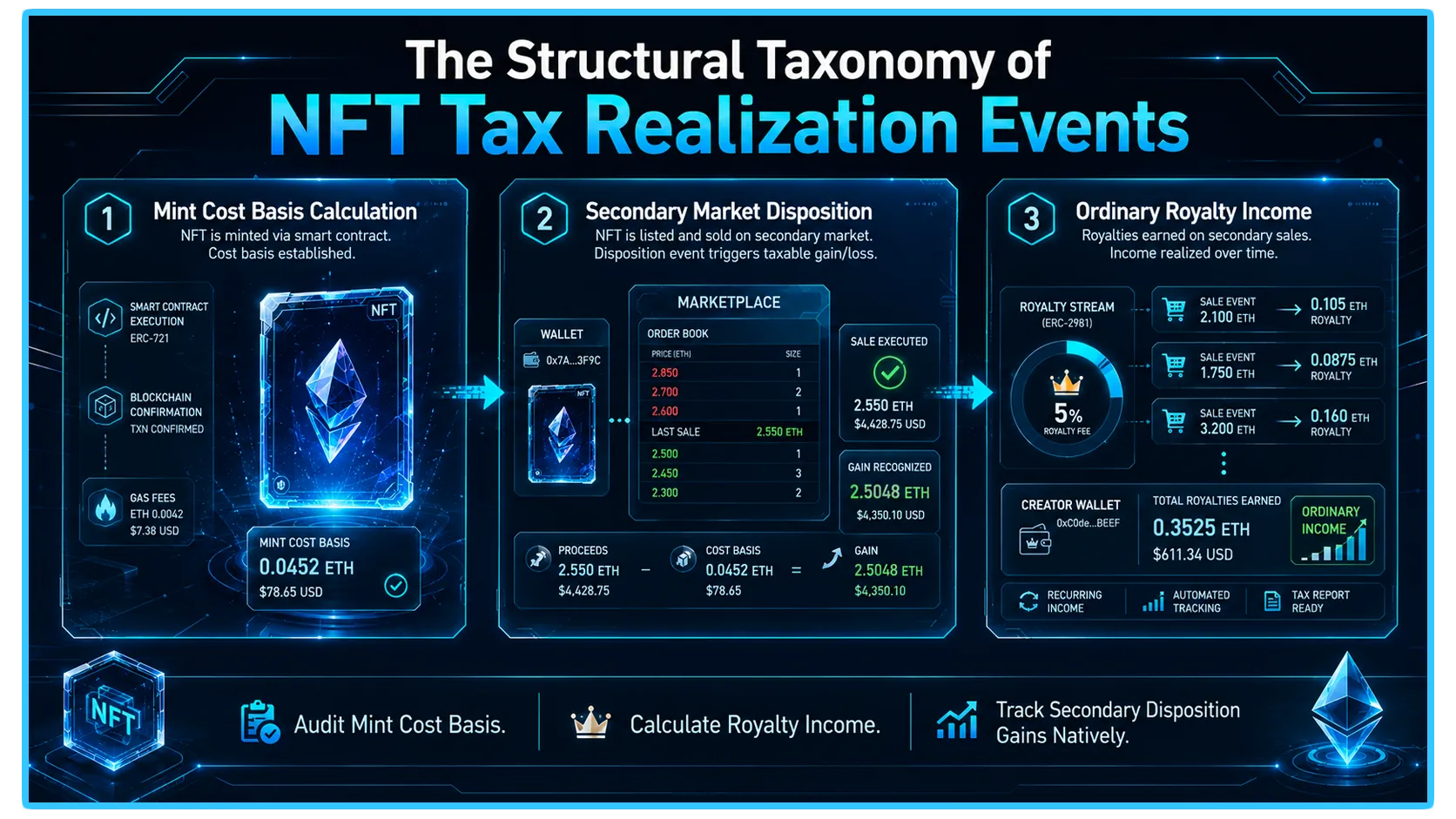

This guide provides the structural taxonomy needed to classify your NFT activities, ensuring you can identify which events trigger immediate tax liability and which act as cost-basis adjustments in your overall portfolio.

1. The Minting Phase: Establishing Your Cost Basis

The "minting" event is the birth of an NFT on the blockchain and serves as the foundational moment for your tax reporting. At this stage, you are effectively "purchasing" a unique digital asset from the protocol.

Calculating the Initial Cost Basis

To accurately report your future capital gains, you must correctly identify your total "acquisition cost" at the moment of minting. This is not merely the floor price or the minting fee set by the project; it is the total economic expenditure required to secure the asset.

The Minting Price: The primary fee paid to the project treasury.

Gas Expenditures: The transaction fees paid to the network (e.g., Ethereum) to execute the smart contract call. Under most jurisdictional frameworks, these gas fees are considered part of the "cost of acquisition" and should be added to the total cost basis of your NFT.

By documenting the total value (Mint Price + Gas Fees) in your fiat currency at the exact timestamp of the mint, you create the "anchor" for your NFT cost basis. If you fail to account for gas fees, you artificially lower your basis, resulting in an inflated capital gain when you eventually dispose of the asset.

2. Secondary Market Sales: Realizing Gains and Losses

Once an NFT is minted or purchased, it enters the secondary market. The sale of an NFT is the most straightforward taxable event, categorized as a disposition of property.

Classification of Dispositions

When you sell an NFT for a fungible token (like ETH or USDC), you are triggering a taxable realization. The calculation is relatively standard:

Capital Gain/Loss: (Total Proceeds - Total Acquisition Cost Basis) = Taxable Gain or Loss.

A critical complexity arises if you participate in "cross-asset" trades. If you trade your NFT for another NFT, many tax jurisdictions view this as a taxable event where you must determine the fair market value of both assets at the time of the swap. This "barter-like" transaction requires you to realize a gain or loss on the NFT you are giving up, based on its current market value, even if no fiat currency ever touched your bank account.

3. Royalties: Ordinary Income vs. Capital Gains

For creators and active participants, royalties represent a distinct stream of revenue. In many jurisdictions, the tax classification of royalties differs significantly from the appreciation of the NFT's underlying value.

Royalties as Ordinary Income

If you are an artist or creator receiving secondary market royalties, these payments are typically classified as "ordinary income" rather than "capital gains." Because royalties are viewed as compensation for your intellectual property or services rather than the appreciation of a held asset, they are often subject to different tax rates.

Taxing the Accrual: Similar to yield farming, royalties are usually considered taxable income at the moment they hit your wallet and you gain the ability to exercise control over them.

The Record-Keeping Requirement: Because these are distinct from capital gains, they must be tracked in a separate ledger. Failing to distinguish royalty income from capital gains can lead to significant errors when filing, as these categories may be taxed at vastly different levels depending on your local tax residency.

4. Jurisdictional Nuances and Compliance

Tax law regarding digital collectibles is rapidly evolving, and your residency plays a primary role in how your activities are treated. Some jurisdictions have begun to clarify that NFTs are "collectibles," which may be subject to a higher capital gains tax rate compared to standard financial assets or stocks.

The Role of Documentation

The burden of proof rests entirely on the asset holder. If you cannot provide an audit trail for a specific mint or sale, tax authorities may assume your entire proceeds are taxable gains with a cost basis of zero. Using NFT tax event tracking software is no longer optional for active participants; it is a fundamental requirement. By maintaining a clean log of your transaction hashes, timestamps, and the associated value of native tokens at the time of each event, you build an institutional-grade defense for your tax filings.

5. Operational Verification via DEXTools

- Even for unique digital collectibles, maintaining visibility over the underlying native token's liquidity and market health is essential. DEXTools offers advanced telemetry to monitor the trading volume, floor price trends, and liquidity pool health of the assets you use to fund your NFT activities.

- By utilizing the Pair Explorer and the Big Swap Explorer, you can verify the exact market value of the native tokens you used for minting or received from sales, providing a consistent data source to cross-reference with your tax ledger. Accurate documentation ensures that your unique assets rest safely within your portfolio, shielded from compliance-related volatility.

You can access DEXTools here and start trading today!

What Is Cost Basis in Crypto? Tax Guide What Are Gas Fees? How They Work on Ethereum and L2s Top 5 NFT Marketplaces in 2026: Where to Buy and Sell Digital Assets 7 On-Chain Data Signals That Help Identify High-Growth Crypto AssetsDisclaimer: This article is for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other kind of advice. DEXTools does not recommend buying, selling, or holding any cryptocurrency or token. Users should conduct their own research and consult with a qualified financial advisor before making any investment decisions. Cryptocurrency investments are volatile and high-risk. DEXTools is not responsible for any losses incurred.