Qu'est-ce que Spark Protocol: guide lending Sky DAI (2026)

— By Whatsertrade in Tutorials

Spark est le protocole de lending de l'ecosysteme Sky (ex MakerDAO). Guide 2026 sur Spark Lend, sDAI, USDS et DSR.

Spark Protocol is the lending engine that powers the Sky ecosystem, the rebranded successor to MakerDAO and the home of USDS (formerly DAI). It pipes the DAI Savings Rate directly into a forked Aave V3 market, routes billions of stablecoin liquidity across DeFi through its Spark Liquidity Layer, and as of 2025 has its own governance token, SPK. If you supply USDS or sUSDS, borrow ETH, or just want to understand where Sky's treasury yield ends up, Spark is the protocol you need to know.

What started as a single-chain lending market in 2023 has become a multi-chain credit infrastructure stretched across Ethereum, Base, Optimism, Arbitrum, and Gnosis Chain. Spark routes capital between Aave, Morpho, tokenized treasuries, and curve pools, acting less like a typical lending app and more like a balance-sheet operator for the Sky stablecoin float. That hybrid role is what makes it different from any other money market.

This guide walks through every moving part. You will learn how Spark Lend works under the hood, why sDAI and sUSDS sit at the center of its risk model, how the Spark Liquidity Layer allocates Sky funds across DeFi, what the SPK token does, and how to actually supply collateral, borrow, and manage health factor without getting liquidated. By the end you should be able to use Spark with confidence and understand the risks that come with it.

What Is Spark Protocol?

Spark Protocol is a decentralized lending platform built on a fork of Aave V3, designed to channel the DAI Savings Rate (now Sky Savings Rate) into on-chain credit markets. Users supply assets like USDS, sUSDS, ETH, wstETH, cbBTC, and USDe as collateral, then borrow against them. Behind the scenes, Spark also operates the Spark Liquidity Layer, which routes Sky stablecoin reserves into yield strategies across DeFi.

Spark was incubated by Phoenix Labs and approved by MakerDAO governance in early 2023 as part of the Endgame plan. After MakerDAO rebranded to Sky in 2024 and DAI was upgraded to USDS, Spark became the primary credit venue for USDS lending and the operational arm distributing Sky's stablecoin treasury into other protocols. The SPK governance token launched in 2025, giving Spark its own incentive layer.

From MakerDAO to Sky: The Endgame Context

You cannot understand Spark without understanding the Maker to Sky transition. MakerDAO launched in 2017 as the original DeFi protocol, minting DAI against collateral like ETH and WBTC. By 2022 it had ballooned into a multi-billion-dollar credit business, but founder Rune Christensen argued the protocol had grown too complex and too dependent on centralized real-world-asset (RWA) collateral. His response was the Endgame plan, a multi-year restructuring that would eventually split Maker into smaller specialized units called SubDAOs.

Spark was the first major SubDAO product. Approved by MakerDAO governance in February 2023, Spark Lend launched on Ethereum mainnet in May 2023 with a fork of Aave V3 code (Aave received a small percentage of Spark revenue as part of the licensing deal). The pitch was simple: route the DAI Savings Rate (DSR) directly into a money market, so depositors could earn the DSR plus borrowing fees, while borrowers got DAI at the most efficient rate on the market.

In August 2024, MakerDAO rebranded to Sky. DAI did not disappear, but a new stablecoin called USDS was introduced as a one-to-one upgrade path. MKR was upgraded to SKY at a 1:24,000 ratio. The DSR was rebranded as the Sky Savings Rate (SSR). All of this directly affected Spark, which had to support both DAI and USDS, both sDAI and sUSDS, and adjust its risk parameters to align with Sky governance instead of Maker governance.

For a deeper view of the broader sector Spark sits in, read our complete guide to DeFi before diving deeper.

How Spark Lend Works

Spark Lend is fundamentally an Aave V3 fork, so the mechanics will feel familiar if you have used Aave before. Liquidity providers deposit assets into smart contract pools and receive interest-bearing receipt tokens, called spTokens. Borrowers post collateral, take out loans against it, and pay variable interest. The protocol tracks health factor in real time and liquidates positions that fall below the required collateralization ratio.

Where Spark diverges from a vanilla Aave fork is in three places: the direct integration with the DSR, the isolated market architecture for newer assets, and the way Sky treasury liquidity is plumbed into the protocol via a feature called the Direct Deposit DAI Module (D3M), now expanded as the broader Spark Liquidity Layer.

The interest rate model uses the standard Aave V3 jump rate curve. Each market has an optimal utilization point (typically 80 to 92 percent depending on asset). Below the kink, rates grow slowly. Above the kink, rates spike to push borrowers to repay and incentivize new lenders. That makes the protocol self-balancing, since heavy borrowing demand pushes APR up until equilibrium returns.

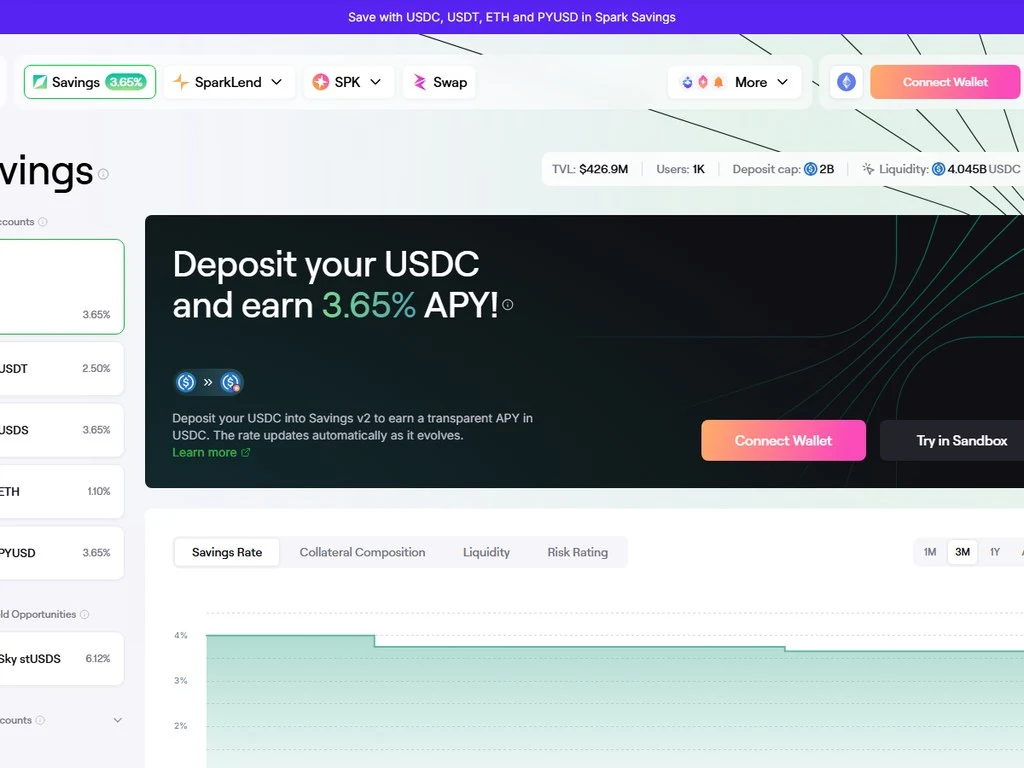

sDAI, sUSDS and the Sky Savings Rate

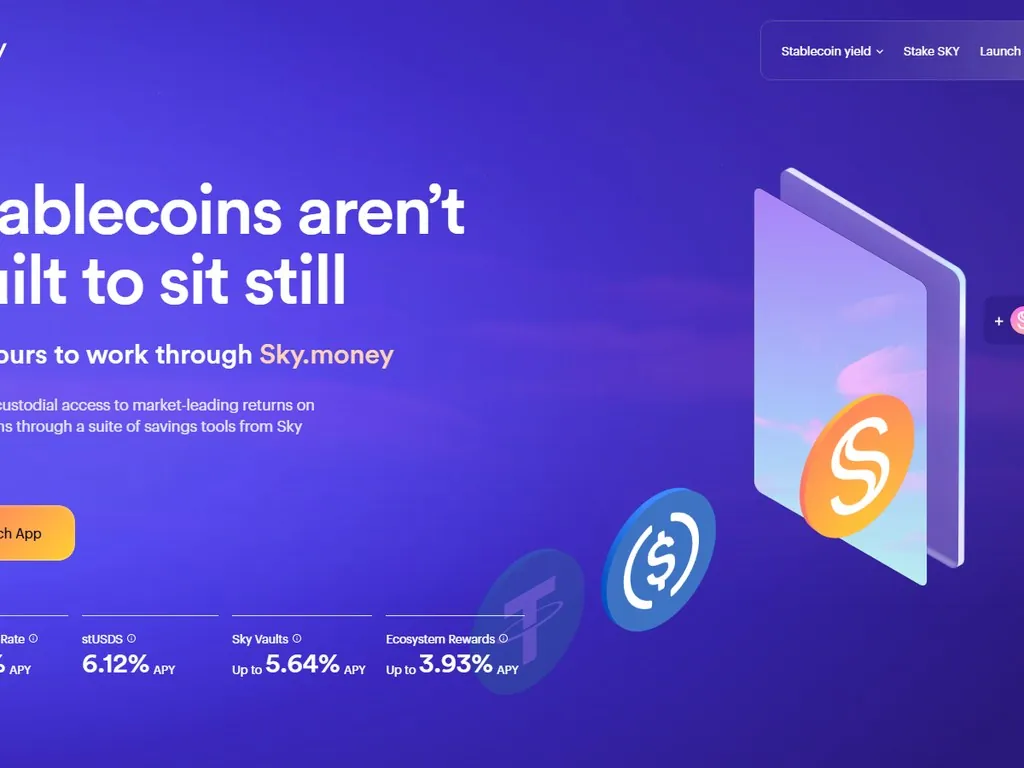

The single most important concept in Spark is the relationship between USDS and its yield-bearing wrapper sUSDS (the modern successor to sDAI). When you deposit USDS into the Sky Savings Module, you receive sUSDS in return. That sUSDS automatically accrues the Sky Savings Rate, currently set by Sky governance and adjusted periodically. The exchange rate between sUSDS and USDS grows over time, so the wrapper effectively becomes more valuable while the underlying balance stays constant.

Spark integrates this in two ways. First, sUSDS and sDAI are both accepted as collateral in Spark Lend, so users can deposit yield-bearing stablecoins and still earn the SSR while using them to borrow other assets. Second, the USDS supply pool on Spark Lend uses the SSR as its floor rate. Even if borrowing demand is zero, USDS depositors earn at least the savings rate, because Spark routes idle liquidity into the Sky Savings Module behind the scenes.

This is a structural advantage that no other lending protocol can match. On Aave, an idle USDC supply earns nothing if no one is borrowing. On Spark, an idle USDS supply earns the SSR. That floor rate alone is enough to make Spark the dominant venue for stablecoin yield on Ethereum.

USDS vs DAI: The Migration Nuances

The DAI to USDS migration is voluntary but heavily incentivized. The two tokens are interchangeable one-to-one through the official Sky Upgrade Hub, with no fees and no slippage. Users who upgrade DAI to USDS get access to the Sky Token Rewards program, which historically distributed SKY and other ecosystem tokens to USDS holders. Many Spark users keep DAI for compatibility reasons (some integrations still reference DAI by address) but use USDS when they want yield exposure.

New Sky-native stablecoin. Compatible with Sky Rewards. Backed by the same collateral and CDPs as DAI. Default mint asset of Sky ecosystem in 2026.

Legacy Maker stablecoin. Still fully supported. 1:1 redeemable to USDS. Used by older integrations and contracts that hardcoded the DAI address.

Yield-bearing wrapper of USDS. Accrues Sky Savings Rate. ERC-4626 standard, so it composes cleanly with the rest of DeFi.

Older yield-bearing DAI wrapper. Still active. Accrues DSR (now linked to SSR). Maintained for backward compatibility.

One subtle nuance: USDS supply on Spark exceeds DAI supply by a wide margin in 2026, because newer users default to USDS. But many institutional integrations still hold sDAI rather than sUSDS, since sDAI was the first widely-used yield-bearing stablecoin and ended up in dozens of vault strategies. Spark treats them as equivalent for collateral purposes, but liquidity is deeper on the USDS side. If you want to learn more about how stablecoins fit into the broader landscape, our USDT stablecoin guide is a useful comparison point.

The Spark Liquidity Layer Explained

This is what truly differentiates Spark from Aave or Morpho. The Spark Liquidity Layer (SLL) is a programmatic system that allocates Sky treasury stablecoins across multiple DeFi protocols to maximize yield. It is governed by Sky and operated by Spark, and as of 2026 it deploys multiple billions of dollars worth of USDS, sUSDS, and DAI into venues like Aave V3, Morpho, Pendle, and various Curve pools.

The SLL evolved out of the original Direct Deposit DAI Module (D3M), which let MakerDAO mint DAI directly into another protocol's lending pool. Spark inherited and expanded this design. Today the SLL holds positions across Ethereum mainnet, Base, Optimism, Arbitrum, and Gnosis Chain, automatically rebalancing based on yield opportunities, risk parameters voted by Sky governance, and total caps for each venue.

The SLL has practical effects you can see on chain. When Aave V3 USDS borrowing demand spikes and APR jumps, the SLL deposits more USDS into Aave to capture the higher rate, while Spark Lend's own market sees lower utilization (and lower borrower rates) as a result. When Morpho launches a new isolated market with attractive risk parameters, the SLL can seed it with millions of USDS to bootstrap liquidity.

From a Sky perspective this is a treasury management tool. Sky earns a yield spread between the stablecoins it mints (interest collected from borrowers and external venues) and the SSR it pays to USDS holders. That spread accrues to the Sky surplus buffer and is eventually distributed via Sky governance, including funding the Spark SubDAO. From a Spark token holder perspective this is a value-accrual engine, since SPK governance can influence how SLL fees are distributed.

Top Markets on Spark in 2026

Spark Lend supports a curated set of assets, all approved by Spark governance and Sky risk reviewers. Compared to Aave, Spark runs a tighter list of markets, focused on blue-chip collateral and on Sky's strategic assets. Here are the most important markets you will encounter in 2026.

USDS is the flagship market. Hundreds of millions to several billion in supply, depending on the cycle. Variable supply APR generally trades a few basis points above the SSR. Borrow APR follows the jump rate curve. This is the deepest stablecoin venue in the Sky ecosystem.

DAI remains a major market for legacy reasons. Supply is smaller than USDS but still significant. Risk parameters are essentially identical, since DAI and USDS share the same backing.

sUSDS and sDAI are accepted as collateral, allowing users to borrow against yield-bearing stablecoins without giving up their SSR yield. The loan-to-value (LTV) parameters are slightly higher than for raw stablecoin assets because the yield wrapper grows in value over time.

ETH and WETH markets are the primary venue for borrowing the native token. Many leverage strategies use ETH as the borrowed asset against stablecoin collateral, or vice versa.

wstETH is the most popular leveraged-staking market on Spark. Users supply wstETH (or its equivalent rETH from Rocket Pool), borrow ETH, swap into more wstETH, and loop the position to amplify staking yield.

cbBTC represents Coinbase Wrapped Bitcoin. Adopted in 2024, it gave Spark its first significant BTC-denominated collateral, useful for borrowers who want stablecoin liquidity against BTC without selling.

USDe, Ethena's synthetic dollar, is supported as an isolated market with conservative caps. It enables interesting trades like supplying USDe and borrowing USDS to capture spread between Ethena's funding yield and the SSR.

The SPK Token: Tokenomics and Utility

Spark launched its native governance token, SPK, in 2025 as part of the Sky Endgame's SubDAO rollout. Before that, all Spark governance decisions were made through Sky governance via the broader MKR-to-SKY voting structure. SPK gives Spark its own dedicated governance layer, with token holders voting on parameter changes, risk additions, SLL allocations, and the distribution of protocol revenue.

SPK has a total supply of 10 billion tokens. The distribution is structured to align long-term users with the protocol. Sky Farming accounts for the largest share, distributed to USDS depositors and sUSDS holders over multiple years. Ecosystem incentives, including liquidity mining and grants, are the second-largest bucket. The Spark team, advisors, investors, and the Sky DAO treasury also receive allocations with multi-year vesting schedules.

| Sky Farming (USDS holders) | 65 percent |

| Ecosystem incentives | 12 percent |

| Spark team and contributors | 12 percent |

| Investors and advisors | 6 percent |

| Sky DAO treasury | 5 percent |

SPK utility falls into three categories. First, governance: SPK holders vote on Spark proposals, risk parameters, SLL allocations, and treasury decisions. Second, fee sharing: a portion of Spark protocol fees can be directed back to SPK stakers if governance decides. Third, incentives: SPK is used to bootstrap new markets, reward users on cross-chain deployments, and seed liquidity in partner protocols. SPK does not currently mint stablecoins or directly secure collateral, which keeps its risk profile cleaner than MKR (or SKY) in that respect.

Spark Across Chains

Spark originally launched on Ethereum mainnet, but as of 2026 it operates on multiple networks. Gnosis Chain was the first non-Ethereum deployment, launched in early 2024, and is still where Spark's xDAI-paired markets live. Base became the second major deployment when Coinbase's L2 grew rapidly in 2024 and 2025. Optimism and Arbitrum followed, primarily as venues for SLL allocations rather than full Spark Lend markets.

The cross-chain architecture uses a hub-and-spoke model. Ethereum mainnet remains the canonical home of Sky governance and the SLL controllers. Each L2 or sidechain deployment receives liquidity from the SLL through canonical bridges and authorized routers. Users on Base or Optimism interact with Spark exactly as they would on Ethereum, but with lower gas costs. The trade-off is that some advanced features (like complex looping strategies) may have lower liquidity on L2s.

If you care about gas costs and want to understand how transaction fees vary by chain, our Gwei and gas guide explains the underlying mechanics.

Step-by-Step: Supply USDS and Borrow ETH

Here is how to actually use Spark to supply USDS as collateral and borrow ETH. The exact UI may evolve, but the underlying mechanics will not.

Step 1: Connect a wallet. Go to the official Spark app at spark.fi. Connect MetaMask, Rabby, WalletConnect, or another EVM wallet. Make sure you are on the Ethereum network (or your preferred Spark-supported chain). Always double-check you are on the genuine spark.fi domain, since phishing copies are common.

Step 2: Acquire USDS. You can buy USDS on a DEX or upgrade DAI to USDS one-to-one on the Sky app. If you are coming from another stablecoin like USDC, swap via a router like 1inch. Our 1inch aggregator guide walks through that process.

Step 3: Supply USDS to Spark. Click the USDS market in the Spark dashboard and press Supply. Approve the token (this is a one-time approval per asset, costing a small amount of gas). Then sign the supply transaction. Your wallet will receive an equivalent amount of spUSDS, the interest-bearing receipt token.

Step 4: Enable USDS as collateral. By default, supplying USDS makes it available as collateral. You can confirm this by checking the toggle in your dashboard. If it is off, switch it on. Now your USDS counts toward your borrow power.

Step 5: Check your borrow limit and health factor. The dashboard will show your maximum borrow capacity in USD terms. The exact LTV depends on the collateral asset. For USDS as collateral, LTV is typically very high (around 87 to 90 percent) because the collateral is itself the same stablecoin being borrowed in some cases. For ETH borrowing, LTV is lower because ETH is volatile.

Step 6: Borrow ETH. Click the ETH market and press Borrow. Enter the amount, review the borrow APR and projected health factor, and sign. The ETH appears in your wallet within seconds. You can now use it for trading, staking, or whatever your strategy requires.

Step 7: Monitor health factor. Set up alerts (Etherscan, DeBank, or DeFi Saver work well). If ETH price rises significantly, the dollar value of your debt grows, and your health factor falls. If it approaches 1.0, you must either deposit more collateral, repay part of the debt, or close the position. Aim to keep health factor at 1.5 or higher to leave room for volatility.

Step 8: Repay or unwind. When you want to close the position, repay the ETH debt (you can do this in any sequence: repay all, repay part, or use a flash loan to unwind a leveraged position in one transaction). Once debt is repaid, you can withdraw your USDS collateral plus accrued supply yield.

Health Factor and Liquidation Mechanics

Health factor is the single most important number to track when borrowing on Spark. It is calculated as the sum of (collateral value times liquidation threshold) divided by total borrowed value. When it falls below 1.0, your position is liquidatable. Liquidators repay part of your debt and receive your collateral plus a bonus, which typically ranges from 5 to 10 percent depending on the asset.

To avoid liquidation, follow three rules. First, never borrow at the maximum LTV. Leave a safety buffer. A health factor of 1.5 is a common target for active managers, while 2.0 or higher is appropriate for passive positions. Second, monitor positions actively, especially during periods of high volatility. ETH dropping 10 percent in an hour is not unusual, and your health factor will drop with it. Third, have a deleveraging plan. Know in advance how you will repay or top up collateral if your position deteriorates. For more on liquidation risk in general, our liquidation zones guide is essential reading.

Spark vs Aave vs Morpho

Spark, Aave, and Morpho are the three dominant lending protocols on Ethereum in 2026, and they have different strengths. Choosing between them depends on what you want to borrow and what you want to earn.

The summary: Spark wins for USDS and DAI lending, especially passive supply, because of the SSR floor. Aave wins for breadth of assets and chains, and remains the most widely integrated venue. Morpho wins for sophisticated users building custom markets and for those seeking the highest yields with explicit risk acceptance. Many serious DeFi users hold positions in all three depending on the strategy.

Risks and What Can Go Wrong

Spark looks safe on the surface, but several risk categories deserve scrutiny before committing significant capital.

Smart contract risk. Spark is built on Aave V3 code, which has been audited extensively, but the Spark fork introduces additional contracts for the SLL, the savings module, and Sky-specific modules. Each of those is an attack surface. Spark engages multiple audit firms and runs a bug bounty, but no protocol is bulletproof. Make sure you understand Permit2 token permission risks before signing arbitrary approvals.

Sky governance risk. Spark is tightly coupled to Sky governance. If SKY holders pass a controversial parameter change, increase risky RWA exposure, or modify the SSR sharply, all Spark users feel the impact. Sky governance has historically been responsive but has also approved aggressive RWA allocations that critics view as risky.

RWA collateral exposure. A meaningful percentage of Sky's stablecoin backing is collateralized by real-world assets, including tokenized US Treasuries, real-estate-backed loans, and traditional fixed-income vehicles. If any of those RWA exposures default or face redemption gates, USDS itself could be impaired. The protocol holds significant surplus to absorb minor losses, but a major RWA shortfall would be a serious event. Our RWA tokenization guide explains this landscape in depth.

Liquidation risk. Borrowers face liquidation if collateral falls or debt grows faster than expected. This is amplified in leveraged staking strategies where wstETH is supplied and ETH is borrowed. If wstETH depegs from ETH (it has happened briefly during past stress events), the borrower can be liquidated even though both assets remain backed.

Oracle risk. Spark relies on Chainlink price feeds and supplementary oracles for some assets. A bad price update, an oracle delay, or a manipulated feed could trigger erroneous liquidations or allow undercollateralized borrowing. Spark has multiple safeguards, but oracle risk is structural to all lending protocols.

Bridge and cross-chain risk. SLL allocations to L2s and sidechains depend on canonical bridges. A bridge exploit could trap or steal allocated funds. Spark uses only the most reputable bridges and tends to be conservative with cross-chain exposure, but the risk is not zero.

De-pegging risk. USDS, like DAI before it, depends on a complex collateral mix to maintain its peg. The peg has held remarkably well for years, but stress events (a sudden RWA loss, a black swan in crypto markets, a regulatory shock) could pressure the peg. Spark users denominated in USDS bear this risk directly.

Advanced Strategies on Spark

Once you understand the basics, Spark opens up to a series of more sophisticated plays. Most active DeFi users in 2026 layer at least one of these on top of simple supply or borrow positions.

Loop wstETH against ETH. Supply wstETH, borrow ETH, swap back to wstETH, supply again. Repeat to build leveraged staking exposure. Net yield is approximately staking APR times leverage minus borrowing APR times leverage minus one, plus any incentives. Done conservatively (2x to 3x), this is a popular yield strategy. Done aggressively (5x or more) it becomes dangerous during volatility.

USDe-USDS spread trade. Supply USDe (or sUSDe) as collateral. Borrow USDS. Earn the difference between Ethena's funding yield (which can spike to 15 to 30 percent during bullish periods) and the USDS borrow rate. The risk is USDe depegging or Ethena's funding rate flipping negative, which would invert the trade.

cbBTC borrowing for stablecoin liquidity. Hold cbBTC long-term but need stablecoin liquidity without selling. Supply cbBTC, borrow USDS, deploy elsewhere or use it for spending. As long as BTC does not crash and your health factor stays safe, you keep your BTC exposure plus get liquidity.

SSR farming via sUSDS. Simplest strategy. Hold USDS in the Sky Savings Module, earn the SSR, never borrow. This is what most of the Sky community recommends to newcomers. It is also what the SLL replicates for Sky's own treasury, just at industrial scale.

If you want to test these strategies in simulation before deploying real capital, our backtesting guide walks through the framework.

Spark Pros and Cons

- Sky Savings Rate floor on USDS supply

- Native USDS and DAI lending with deepest liquidity

- Spark Liquidity Layer routes funds to best yields

- Battle-tested Aave V3 codebase

- SPK token rewards for Sky participants

- Multi-chain deployment with consistent UX

- Heavy dependence on Sky governance decisions

- RWA collateral exposure in underlying stablecoins

- Smaller asset list than Aave

- Some markets thinly liquid on L2 deployments

- USDS still less universally accepted than USDC

- Complex Sky / Spark structure for beginners

DSR / SSR Rate History

The DSR (now SSR) has moved through several major phases since Spark launched. Understanding this history helps you calibrate expectations for future yield.

In May 2023, when Spark launched, the DSR was 1 percent. Within months, MakerDAO governance raised it aggressively as US Treasury yields climbed. By August 2023 the Enhanced DSR (EDSR) was as high as 8 percent for the largest depositors, a special promotional rate. By late 2023 it stabilized around 5 percent matching the prevailing US risk-free rate.

Throughout 2024, the rate moved between 6 and 12 percent at various points, depending on market conditions and Maker's surplus. The rebrand to Sky in August 2024 did not change the underlying mechanics, just the name. By 2025 the rate was tracking US Treasury yields more closely as RWA collateral became a larger share of Sky's backing.

In 2026, the SSR fluctuates between roughly 4 and 8 percent depending on Sky's surplus, Treasury rates, and governance preferences. The rate is set by Sky governance through a regulated process. It is not algorithmic, which is both a feature (responsive) and a risk (politically influenced).

Where to Track Spark On-Chain

Several dashboards make it easy to monitor Spark in real time. The official spark.fi app shows your positions, the markets, and the Spark Liquidity Layer status. DefiLlama tracks total TVL, supply, and borrow figures across all chains. Sky's own explorer at sky.money tracks SSR history, USDS supply, and Sky governance proposals. Etherscan and other block explorers let you read raw contract state directly. Our Pyth oracle guide covers how price feeds can be tracked for the assets you supply or borrow.

For tokenized treasury exposure that complements Spark holdings, our Ondo Finance guide covers the largest RWA issuer in the space, whose products often appear in SLL allocations.

Frequently Asked Questions

Is Spark Protocol safe to use?

Spark inherits the security profile of Aave V3, which has been audited extensively and has run for years without major exploits. Spark adds additional contracts for the savings module and liquidity layer, which are also audited and covered by bug bounties. That said, no smart contract is risk-free. The largest risks are not the contracts themselves but Sky governance decisions, RWA collateral exposure in USDS, and liquidation risk for leveraged borrowers. Use Spark with the same caution you would apply to any DeFi lending protocol.

What is the difference between DAI and USDS?

USDS is the rebranded successor to DAI under Sky governance, introduced in August 2024 as part of the Endgame transition. Both stablecoins share the same collateral backing and are redeemable one-to-one with no fees through the official Sky Upgrade Hub. USDS is required to participate in Sky Token Rewards and is the default mint asset in 2026. DAI remains fully functional and is still supported by Spark for backward compatibility.

What is sUSDS?

sUSDS is the yield-bearing wrapper of USDS. When you deposit USDS into the Sky Savings Module, you receive sUSDS, which automatically accrues the Sky Savings Rate. The exchange rate between sUSDS and USDS grows over time. sUSDS is an ERC-4626 token, so it composes cleanly with Aave, Morpho, and other DeFi protocols. On Spark, sUSDS can be used as collateral while still earning the SSR.

What does SPK do?

SPK is the native governance token of Spark Protocol, launched in 2025. SPK holders vote on Spark Lend risk parameters, Spark Liquidity Layer allocations, and treasury decisions. A portion of protocol revenue can be directed to SPK stakers via governance. SPK does not currently mint stablecoins or directly secure collateral, keeping it focused on governance and incentives rather than the collateral-backstop role that MKR or SKY play.

How is the Sky Savings Rate set?

The Sky Savings Rate is determined by Sky governance through a structured process. Risk advisors and economic analysts produce recommendations based on US Treasury yields, Sky's surplus buffer, RWA earnings, and DeFi competitive rates. SKY token holders then vote (or delegate) on proposed rate changes. Adjustments typically happen monthly or in response to market conditions. The rate is not algorithmic, which means it can lag market moves but also can be stabilized politically when needed.

What is the Spark Liquidity Layer?

The Spark Liquidity Layer (SLL) is the system that allocates Sky treasury stablecoins across multiple DeFi protocols to earn yield. It deploys billions of dollars worth of USDS, sUSDS, and DAI into venues like Aave, Morpho, and Curve, rebalancing based on yield opportunities and Sky governance parameters. The SLL evolved from the original Direct Deposit DAI Module and now operates across Ethereum, Base, Optimism, Arbitrum, and Gnosis Chain.

Can I lose money on Spark?

Yes. Suppliers face smart contract risk, RWA collateral risk in the underlying stablecoins, and the possibility of a USDS de-peg event. Borrowers face all of those plus liquidation risk if their collateral falls in value or their debt grows due to rising interest rates. Leveraged strategies amplify both losses and gains. Always understand the position before opening it and never deposit funds you cannot afford to lose.

Is Spark Protocol the same as Aave?

No. Spark is a separate protocol that was built on a fork of Aave V3 code under a licensing agreement that pays Aave a small percentage of Spark revenue. The two protocols have different governance (Spark uses SPK and Sky, Aave uses AAVE), different markets, different risk parameters, and different liquidity. Spark focuses on USDS and DAI as native assets and integrates with Sky in ways Aave cannot. They are competitors, but they also share design lineage.

Which chains does Spark support?

As of 2026, Spark operates on Ethereum mainnet (primary), Gnosis Chain, Base, Optimism, and Arbitrum. Ethereum hosts the governance and core SLL controllers. The L2 deployments offer the same user experience as mainnet with significantly lower gas costs but with more concentrated asset support. Bridging happens through canonical Ethereum-to-L2 bridges and authorized routers managed by Sky governance.

How do I claim SPK rewards?

SPK rewards are distributed through the Sky Token Rewards module. To qualify, you must hold USDS (or sUSDS) and have enrolled in the rewards program, then activate SPK as your chosen reward token. Rewards accrue continuously and can be claimed from the Sky or Spark app at any time. Claim transactions cost gas, so most users claim in batches when rewards reach a meaningful amount. The exact distribution schedule and farming rate is set by Sky governance.

Final Thoughts: Why Spark Matters

Spark is more than a lending protocol. It is the operational hub of the Sky ecosystem, the venue where USDS supply and demand meet, and the routing layer that pushes Sky liquidity into the rest of DeFi. If you participate in stablecoin yield, leveraged staking, or any USDS-denominated strategy in 2026, you will end up touching Spark, directly or indirectly.

For passive savers, the appeal is straightforward. Hold sUSDS, earn the SSR, optionally collect SPK rewards. For active borrowers, the deep USDS liquidity and reliable interest rate model make it one of the most efficient places to source stablecoin debt against ETH, wstETH, or BTC collateral. For sophisticated DeFi users, the SLL creates interesting opportunities to front-run or trade alongside Sky's treasury allocations.

The structural risks are real and worth respecting. RWA exposure in USDS means that Spark depositors are indirectly exposed to traditional credit risk in ways most DeFi protocols are not. Sky governance is more responsive than many DAOs but still concentrates power in a relatively small group of large delegates. The SPK token is young and its long-term value accrual depends on governance decisions that have not all been made yet.

If you are new to lending, start small. Supply some USDS, watch the yield accrue, learn the dashboard. Then try a conservative borrow against ETH or wstETH collateral. Build intuition for how health factor reacts to price moves. Only after that should you consider looped or leveraged strategies. The protocol rewards patient users far more than aggressive ones.

And remember: the Spark and Sky ecosystem will keep evolving. New SubDAOs, new collateral types, new SLL integrations, possibly new chains. Stay close to governance forums and reputable risk analysts. The fundamentals you have learned in this guide will carry over, but the surface area expands every quarter.

Whatever your strategy, you now know enough about Spark Protocol to make informed decisions. Go test it with a small deposit, see the SSR accrue, and build from there.