DeFi Taxation: Lending, LPs, and Wrapped Tokens Explained

Tax authorities increasingly categorize decentralized protocol interactions as taxable realizations. We break down the structural classification of LP entries, token wrapping, and reward accruals to ensure your ledger remains compliant.

DeFi Taxation: Mapping Taxable Events in Decentralized Networks

- In the emerging landscape of decentralized finance (DeFi), the illusion of anonymity often masks the reality of transactional tax liability. When you interact with a smart contract, you are not merely engaging in a digital protocol; you are frequently executing a legal exchange of property. Tax authorities globally are increasingly classifying these on-chain interactions as taxable realization events. Because DeFi is inherently cross-chain and algorithmic, many retail participants fail to account for the specific moments when a "taxable gain" is triggered, leading to severe compliance friction when it comes time to reconcile their annual performance.

- To master your tax hygiene, you must transition from treating your wallet as a simple storage vessel to viewing it as a sophisticated tax-reporting engine. Every interaction (whether providing liquidity, wrapping a standard token, or harvesting yields) carries a specific tax classification. The core challenge is that many DeFi primitives trigger taxable events that are invisible to standard centralized exchange reporting tools. By mastering DeFi tax event tracking, you can ensure your cost basis is correctly calculated and your capital gains/losses are accurately realized throughout your fiscal cycle.

This guide dissects the taxable architecture of the three most common DeFi interactions: liquidity provision, token wrapping, and yield-bearing lending, providing the structural framework you need to stay compliant in a decentralized environment.

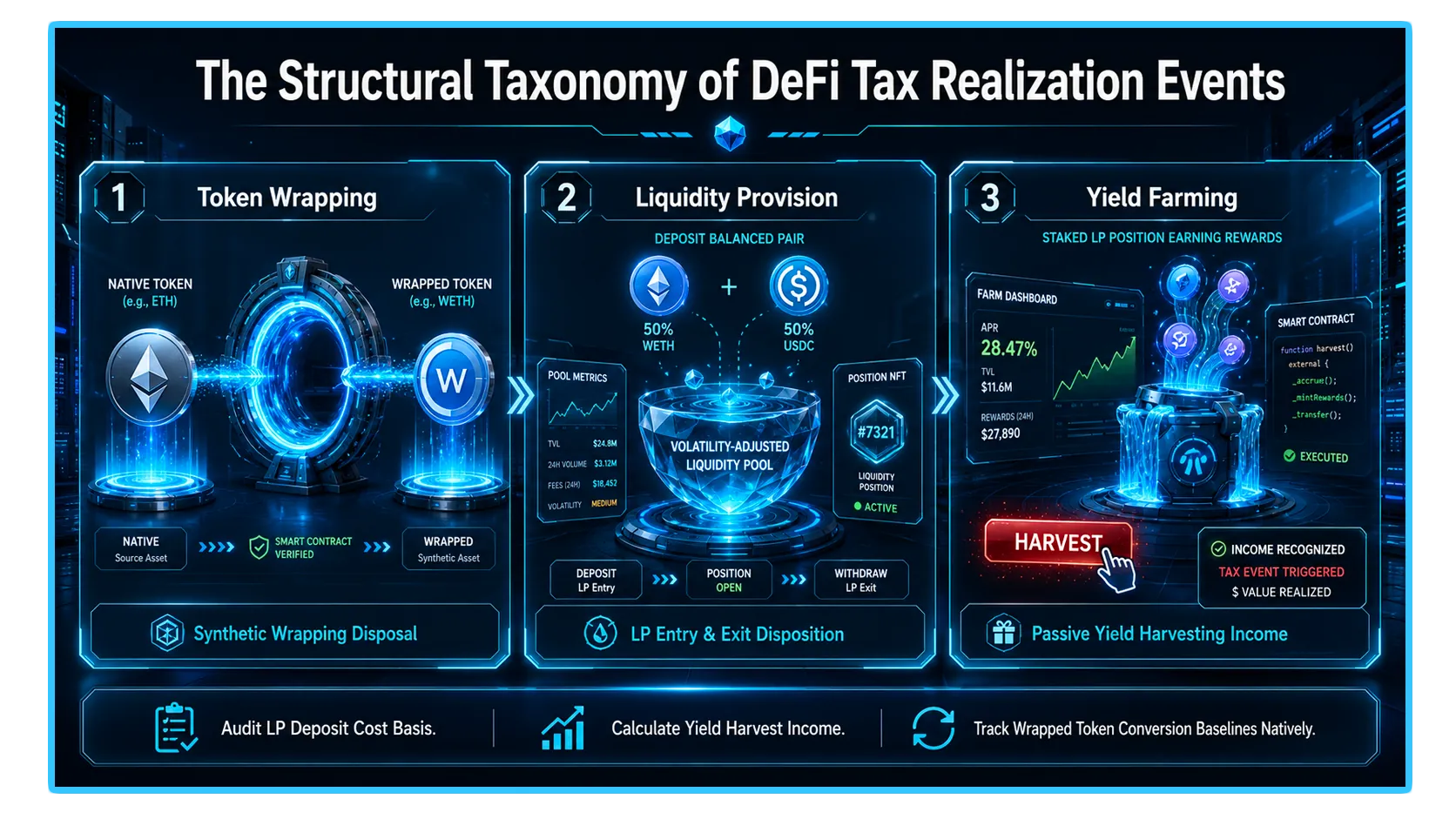

1. The Mechanics of Token Wrapping: Taxable or Nontaxable?

A "wrapped" token (such as WETH or WBTC) is a digital asset that has been locked in a bridge smart contract, with a synthetic equivalent issued on a different blockchain ledger. In the eyes of most tax authorities, the classification of a "wrapping event" is a critical distinction that dictates your reporting obligation.

The "Like-Kind" vs. "Conversion" Debate

For most jurisdictions, the primary question is whether wrapping your token is considered a "disposition" of property.

The Conservative View: Many tax accountants argue that swapping your native token (ETH) for a wrapped version (WETH) is a taxable disposal. You are technically selling one asset class to purchase another. Under this framework, you must realize a capital gain or loss based on the price difference between your original acquisition cost and the value at the time of wrapping.

The Operational View: Conversely, many argue that wrapping is a "like-kind" exchange or a non-disposition event because the economic utility and value of the wrapped asset are pegged precisely 1:1 to the native token.

Best Practice: Always treat the wrap and the unwrap as potential taxable events on DeFi taxation if your local jurisdiction is aggressive regarding asset conversions. Log the timestamp, the price of the native token at the time of wrapping, and the transaction hash.

2. Liquidity Provision (LP): Entry, Exit, and Impermanent Loss

Providing liquidity to decentralized automated market makers (AMMs) is perhaps the most complex area for tax reporting. You are essentially acting as a market maker, depositing assets into a pool to facilitate trading for others.

The LP Entry (The Deposit)

When you deposit a pair of tokens into a liquidity pool (e.g., ETH/USDC), you are essentially swapping your individual tokens for LP tokens. Many jurisdictions view this as a taxable event: you are disposing of two independent assets to acquire a new, singular asset (the LP token). You must record the fair market value of the assets at the time of deposit to establish your new cost basis.

The LP Exit (The Withdrawal)

When you withdraw your liquidity, the pool returns a different ratio of tokens based on the trading activity that occurred while you were a provider. This withdrawal is almost universally considered a taxable disposition.

The Taxable Gain: If you deposited 1 ETH and 2,000 USDC, and you withdraw 0.8 ETH and 2,500 USDC, you have technically "sold" a portion of your ETH and "purchased" more USDC. This exchange triggers capital gains on the ETH that was sold.

Accounting for Impermanent Loss: Impermanent loss is an economic reality, but tax authorities may not allow you to deduct it as a separate expense. Instead, it is factored into your final capital gain/loss calculation upon withdrawal.

3. Yield Farming and Lending: Accrual vs. Realization

Lending and yield farming introduce the complexity of "passive income" versus "capital appreciation." In most jurisdictions, rewards earned from lending protocols are classified as ordinary income, not capital gains.

Taxing the Accrual

The Income Trigger: The moment you "claim" or "harvest" your yield farming rewards, the fair market value of those tokens at that exact second is considered your taxable income.

The Cost Basis: Once those rewards are in your wallet, that "income value" becomes your new cost basis. If you later sell those rewards at a higher price, you then owe capital gains tax on the difference between your cost basis (the price at the time of harvest) and your eventual selling price.

Lending Platforms

Lending your assets out to a protocol (like Aave or Compound) generally is not a taxable event. You are merely moving your assets into a smart contract while retaining ownership. However, if the protocol issues you a "receipt token" (like aTokens or cTokens) that accrues value, you must check whether your jurisdiction views the increase in your receipt token's exchange rate as taxable interest income.

4. Strategic Ledger Hygiene and DEXTools Integration

- To survive an audit in the DeFi space, your documentation must be as immutable as the smart contracts you interact with. Many participants rely on DEXTools to verify their historical transaction prices and pool performance metrics. By leveraging DEXTools' Pair Explorer and Top Traders dashboard, you can audit the exact price of your LP entries and exits, ensuring your reported cost basis matches the actual on-chain liquidity data.

- Maintaining a consistent, granular spreadsheet of every "Wrap," "LP Deposit," and "Harvest" event is the only way to effectively manage your tax liability and avoid the pitfalls of retroactive reporting. While DEXTools provides the real-time pair telemetry, you must bridge that data with a dedicated DeFi tax accounting tool to automate the complex cost-basis math.

You can access DEXTools here and start trading today!

Impermanent Loss in DeFi Liquidity Pools What Is Yield Farming: Complete DeFi Earning Guide What Is Cost Basis in Crypto? Tax Guide What Are Liquidity Pools in DeFi? ExplainedDisclaimer: This article is for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other kind of advice. DEXTools does not recommend buying, selling, or holding any cryptocurrency or token. Users should conduct their own research and consult with a qualified financial advisor before making any investment decisions. Cryptocurrency investments are volatile and high-risk. DEXTools is not responsible for any losses incurred.