The Hidden Cost of a Round Trip Trade: Slippage, Gas, Failed Transactions and Fees

— By Whatsertrade in Tutorials

Many crypto traders calculate profit in a simple way. They look at the buy price, compare it with the sell price, and assume the difference is their gain. If a

Many crypto traders calculate profit in a simple way. They look at the buy price, compare it with the sell price, and assume the difference is their gain. If a token goes up 15 percent, they may believe they made 15 percent. In decentralized exchange trading, the real result is often very different.

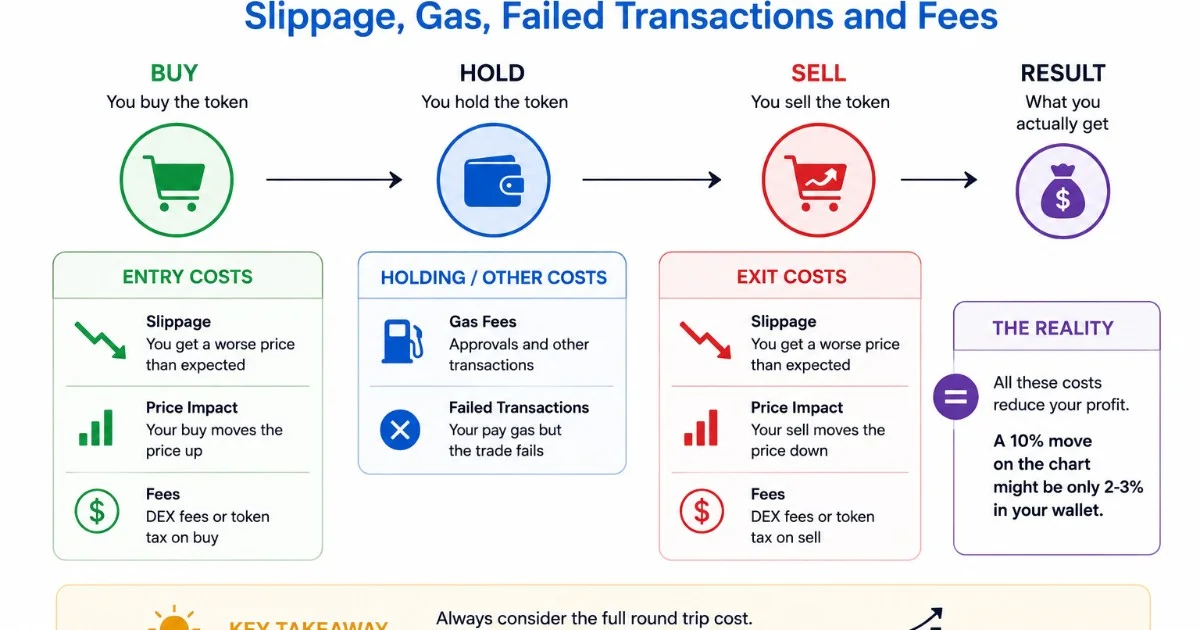

A trade is not just a chart entry and a chart exit. It is a full round trip. You buy a token, hold it, and later sell it back into another asset. During that process, several hidden costs can reduce the final amount you receive. Slippage, gas, DEX fees, failed transactions, price impact, approval costs and weak exit liquidity can all change the outcome.

This is why understanding round trip trade cost is essential for anyone trading on decentralized exchanges. A trade that looks profitable on the chart can become barely profitable, or even negative, once all execution costs are included.

What Is a Round Trip Trade?

A round trip trade is the complete trading cycle from entry to exit. In crypto, this usually means swapping from one asset into a token and later swapping back out. For example, a trader may buy a new token with ETH, BNB, SOL, USDC or another asset. Later, the trader sells that token back into the original asset or into a stablecoin.

The important point is that both sides of the trade matter. The buy has costs, and the sell has costs. If a trader only calculates the price difference between entry and exit, they are ignoring the real cost of execution.

In centralized markets, traders often think in terms of commissions and spread. In decentralized markets, the cost structure can be more complex because execution depends on liquidity pools, network conditions, slippage settings, gas prices, router paths and market volatility.

Why the Chart Does Not Show Your Real Profit

A token chart shows market movement, but it does not show your exact trade result. The displayed price may not be the price you receive when swapping. In thin pools, your own trade can move the price. In volatile markets, the price can change before your transaction confirms. In congested networks, gas fees can make small trades inefficient.

This difference between chart performance and real execution is one of the most common mistakes in DEX trading. A trader may see the token rise 10 percent, but after slippage, gas, fees and sell impact, the actual gain may be much smaller.

The more illiquid and volatile the token is, the larger this gap can become.

Cost 1: Slippage on Entry

Slippage is the difference between the expected price of a trade and the final executed price. When you buy a token, slippage can cause you to receive fewer tokens than expected. This means your real entry price is worse than the chart price you saw before confirming the transaction.

Slippage increases when liquidity is low, trade size is large, price is moving quickly or many traders are trying to buy at the same time. It is especially common during new launches, trending memecoins, low cap tokens and highly volatile market events.

Some traders increase slippage tolerance to force a transaction through. This can help the trade execute, but it also allows the final price to move further against them. A high slippage setting may turn a good looking entry into a poor one.

The first hidden cost of a round trip trade often appears before the trader even owns the token.

Cost 2: Price Impact From Your Own Trade

Price impact is the effect your trade has on the pool price. If your buy order is large compared with the available liquidity, your trade pushes the price upward while it executes. As a result, you pay more for later portions of the same order.

Price impact is not exactly the same as slippage, but the two are connected. Slippage describes the difference between expected and executed price. Price impact describes how much your own order moves the market.

This matters because a trader who creates a large price impact begins the trade at a disadvantage. If buying moves the token up several percent, the token must continue rising just for the trader to break even after other costs.

A position size that works in a deep pool may be too large for a smaller pool. Before entering, traders should ask whether the market can absorb their order without creating a bad entry.

Cost 3: DEX and Pool Fees

Most decentralized exchange pools charge a fee on each swap. This fee may look small, but it applies every time you trade. A round trip trade usually includes at least two swaps: one buy and one sell.

If the pool charges a trading fee on entry and another on exit, that cost must be included in the break even calculation. If the trader routes through multiple pools, the cost can increase. If the token has a transfer tax, buy tax, sell tax or another token level fee, the effective cost can become much higher.

This is why a small price move is not always enough. A token may rise a few percent, but if fees and execution costs consume that move, the trade may not produce a meaningful gain.

Cost 4: Gas Fees

Gas fees are paid to execute transactions on a blockchain. The size of the gas fee depends on the network, congestion, transaction complexity and sometimes urgency. On some chains, gas may be small. On others, or during busy periods, gas can become significant.

Gas affects the full trading cycle. You may pay gas to approve a token. You pay gas to buy. You pay gas to sell. If a transaction fails, you may still lose gas. If you attempt several trades during volatility, gas costs can accumulate quickly.

For smaller accounts, gas can be a major percentage of the total trade. A trader using a small position size may need a much larger price move just to overcome gas costs. This is especially important when trading on networks where gas can spike during heavy market activity.

Cost 5: Token Approvals

Many DEX trades require token approval before selling or interacting with a smart contract. An approval allows the contract to spend a certain token amount from your wallet. This approval transaction can require gas.

Traders often forget approvals when calculating round trip cost. The approval may be small in some cases, but it still matters, especially for smaller trades or expensive networks.

Approval management also has a security dimension. Traders should understand what they are approving and avoid giving unnecessary permissions to unknown contracts. While approval cost is financial, approval risk can become much larger if permissions are mismanaged.

Cost 6: Failed Transactions

Failed transactions are one of the most frustrating hidden costs in decentralized exchange trading. A transaction can fail because the price moved beyond the slippage tolerance, gas was too low, the route changed, liquidity was insufficient, the token had restrictions or the network was congested.

In many cases, the trader still pays gas for the failed attempt. During volatile launches, a trader may experience multiple failed transactions before entering or exiting. Each failure increases the real cost of the trade.

Failed transactions also create emotional pressure. After repeated failures, a trader may raise slippage too high, overpay for gas or make a rushed decision. This can lead to poor execution and increased risk.

A failed transaction is not only a technical inconvenience. It can directly affect profitability.

Cost 7: Exit Slippage

Many traders think carefully about entry slippage but forget about exit slippage. This is a serious mistake. Selling can be more difficult than buying, especially in low liquidity markets or during sharp price declines.

When a trader sells, the pool must absorb the order. If liquidity is thin or other holders are selling at the same time, the final received amount may be much lower than expected. A token can show unrealized profit on the chart, but the trader may not be able to capture that profit at the displayed price.

Exit slippage often becomes worse when confidence weakens. During hype, buyers may absorb sells. During panic, buyers disappear and every sell creates stronger price impact.

A realistic trade plan should estimate the cost of getting out before getting in.

Cost 8: Weak Liquidity at the Exit

Liquidity can change after you buy. A pool that looked tradable at entry may become weaker by the time you want to sell. Liquidity can be removed, volume can fade, buyers can leave or attention can rotate to another token.

This creates a major problem for round trip trading. Your entry conditions and exit conditions may not be the same. A trader may buy during high attention and sell during low attention. If liquidity and volume decline, the exit becomes more expensive.

This is especially common in short lived token trends. A token may be easy to buy during the hype phase, but difficult to sell after attention decays.

Cost 9: MEV and Unfavorable Execution

In some blockchain environments, traders may also face MEV related execution problems. Bots can monitor pending transactions and attempt to profit from them. This may lead to worse execution in certain conditions, especially when slippage tolerance is high or liquidity is thin.

The impact depends on the chain, router, transaction settings and market environment. Traders do not need to understand every technical detail to recognize the practical risk: public pending transactions can sometimes be exploited, and poor execution settings can make the problem worse.

Using reasonable slippage, avoiding oversized trades and understanding pool depth can help reduce exposure to unfavorable execution.

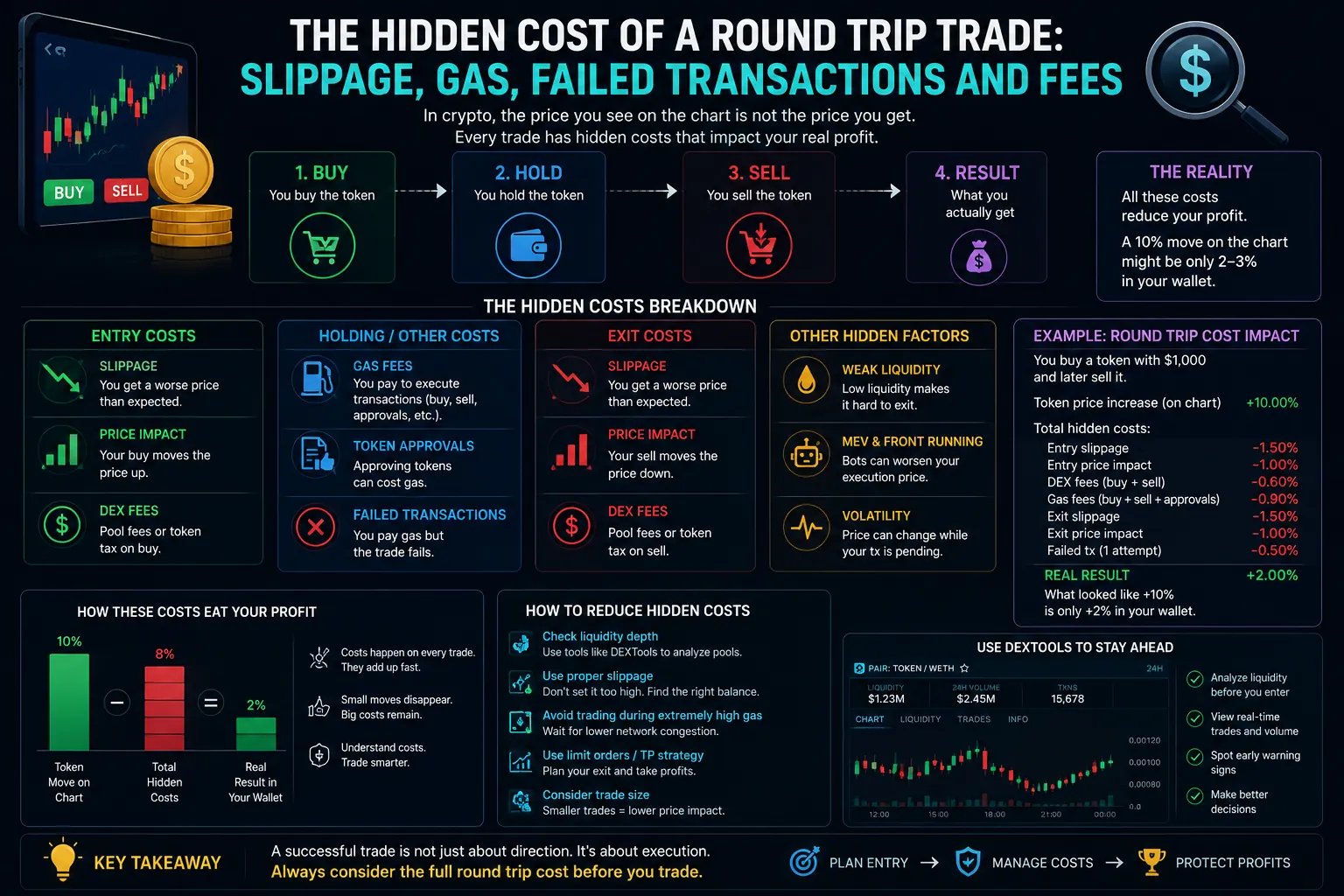

How to Calculate a More Realistic Break Even Point

A realistic break even point includes all costs from entry to exit. Traders should consider entry slippage, entry price impact, DEX fees, gas, approval costs, possible failed transaction costs, exit slippage, exit price impact and any token level taxes or fees.

For example, a token that appears to need only a 5 percent move to produce profit may actually need a much larger move after execution costs. If entry slippage is 2 percent, exit slippage is 2 percent, pool fees apply twice, gas is expensive and there is price impact, the real break even point may be far above the original entry.

The exact number changes by token and network, but the principle is simple. The trade must move enough to pay for the full round trip, not just the chart difference.

Why Microcap Tokens Need a Bigger Profit Buffer

Microcap tokens often require a larger profit buffer because they tend to have lower liquidity, higher volatility, wider execution gaps and more fragile demand. A trader may enter a microcap expecting a quick move, but the hidden costs can be much larger than expected.

In smaller pools, even moderate trades can create price impact. If the trader later sells into weaker demand, the exit can be worse than the entry. This means microcap trades often need more upside potential to justify the risk.

A small target may not be enough. If a trader is aiming for a 5 percent gain in a pool where round trip costs can approach or exceed that amount, the trade may be poorly structured from the beginning.

How DEXTools Can Help Traders Evaluate Round Trip Cost

DEXTools can help traders study the market conditions that influence round trip cost. Before entering a token, traders can review liquidity, volume, recent transactions, price action, pair age and trading activity.

Liquidity helps estimate whether the pool can support the trade size. Volume shows whether the market is active enough to provide entry and exit opportunities. Recent transactions reveal how price reacts to buys and sells. Pair age can help traders understand whether the market is new, established or fading. Price behavior can show whether the token moves smoothly or jumps violently on small trades.

DEXTools does not remove trading costs, but it helps traders understand the environment before they commit capital.

Practical Questions to Ask Before Entering a Trade

Before buying, traders should ask whether the pool has enough liquidity for their position size. They should check whether recent trades caused large price movement. They should estimate how much slippage may occur on entry and exit. They should consider whether gas costs are reasonable relative to the trade size. They should check whether the token has taxes, restrictions or unusual trading behavior.

They should also ask what happens if they need to exit quickly. Can the pool absorb the sell? Is volume strong enough? Are buyers still active? Is liquidity stable, or has it been declining?

The best time to think about exit cost is before the entry is made.

Common Mistakes Traders Make

One common mistake is using the chart percentage as the expected profit. Another is trading position sizes that are too large for the pool. Some traders ignore gas because it feels small compared with the position, but repeated transactions can add up. Others set slippage too high during hype and accept a much worse entry than planned.

Another major mistake is assuming that selling will be as easy as buying. In fast moving markets, the exit can be much harder. Liquidity may fade, buyers may disappear and sellers may compete for the same limited demand.

A trader who ignores round trip cost is not measuring the real trade.

Conclusion

The hidden cost of a round trip trade can change the entire result of a decentralized exchange position. Slippage, gas, DEX fees, token approvals, failed transactions, price impact, MEV risk and weak exit liquidity all affect the final outcome.

A profitable chart does not always mean a profitable trade. Traders need to think in terms of execution, not just direction. Before entering, they should estimate what it will cost to buy, what it may cost to sell, and how much the token must move to make the trade worthwhile.

DEXTools gives traders important market data to evaluate liquidity, volume, transaction behavior and price structure. By using that data before entering, traders can make better decisions and avoid setups where hidden costs consume the opportunity.

Profit is not what the chart promises. Profit is what remains after the full round trip is complete.

How to Bridge Crypto Between Chains: Complete Cross-Chain Tutorial 2026 How to Use 1inch for Swaps: Classic, Fusion and Limit Orders (2026) OKX Web3 Wallet Tutorial 2026: Multi-Chain Setup GuideBeyond the Spread: Unpacking Impermanent Loss in LP Positions

While a simple round trip trade on a DEX incurs slippage and gas, providing liquidity to a Decentralized Exchange (DEX) introduces a more complex, often overlooked cost: impermanent loss. This isn't a direct fee, but rather a divergence in value compared to simply holding your assets. When you deposit two tokens into a liquidity pool, you're essentially betting that their relative price will remain stable. Any significant price movement, up or down, between the two assets you provided will result in impermanent loss.

The term "impermanent" suggests that this loss is temporary and could theoretically reverse if asset prices return to their original ratios. However, in volatile markets, this reversal is far from guaranteed. Many liquidity providers (LPs) fail to account for this potential erosion of capital when calculating their effective returns from trading fees or farming rewards, leading to a miscalculation of their true profitability.

Mitigating Impermanent Loss

Understanding and strategically approaching impermanent loss is crucial for any LP. It fundamentally changes the risk-reward profile of providing liquidity.

- Favor stablecoin pairs: Pools consisting of two stablecoins (e.g., USDC-USDT) minimize price divergence and thus impermanent loss.

- Choose correlated assets: Pairing assets that tend to move in similar directions (e.g., ETH-WBTC) can reduce the impact of relative price changes.

- Monitor pool volatility: Highly volatile pairs are more susceptible to significant impermanent loss. Regular re-evaluation is key.

- Consider single-sided liquidity or concentrated liquidity pools: Newer DEX models offer options that can reduce or optimize exposure to impermanent loss, though they often come with their own complexities.

- Calculate potential loss: Before providing liquidity, use tools or formulas to estimate potential impermanent loss based on various price scenarios.

Related Guides

- What Are Bridge Fees in Crypto? Cost Breakdown, Quotes and Hidden Charges (2026)

- Gas Subsidies vs Organic Fee Demand: When Free Transactions Hide Weak Adoption

- Post-Trade Review Using DEXTools: How to Learn From Failed Crypto Trades

- Liquidity Pool Economics: Fees, Slippage and Impermanent Loss

- What Is Gas Price (Gwei): Complete Ethereum Fees Guide (2026)

Frequently Asked Questions

What is slippage and how does it affect my crypto trades?

Slippage is the difference between your expected trade price and the actual executed price. It occurs due to market volatility or insufficient liquidity, especially with large orders or illiquid assets. This difference directly reduces your potential profit or increases your loss, acting as a hidden cost.

How do gas fees impact my crypto trading profits?

Gas fees are transaction costs paid to network validators on blockchains like Ethereum. These fees are variable and can be substantial, especially during network congestion. Every on-chain interaction, including buying, selling, or moving crypto, incurs gas fees, eating into your net profit.

What are failed transactions and why do they cost me money?

Failed transactions are attempts to execute a trade or interaction on a blockchain that do not complete successfully. Even when a transaction fails, you still pay the gas fee because the computational resources were consumed. This means you lose money without completing your intended trade.

Beyond slippage, gas, and failed transactions, what other fees should I consider?

You should also account for exchange trading fees, which are typically a percentage of your trade volume. Withdrawal fees for moving assets off an exchange and potential network fees for bridging assets between different blockchains are additional costs. These accumulate and diminish your overall profitability.