Stop Loss vs. Trailing Stop: When to Use Each

Digital asset networks run 24/7 on high-leverage microstructures that trigger violent flash liquidations. We break down the automated order book mechanics needed to protect your capital.

The Risk Imperative: Moving from Emotional Survival to Programmatic Boundaries

- In globalized, permissionless digital asset networks, capital preservation is the absolute variable separating generational wealth compounding from total systemic ruin. Because blockchain-based liquidity networks run continuously without regional closing bells, overnight trading freezes, or central corporate circuit breakers, price trends are prone to immediate, extreme structural distortions.

- An unexpected multi-million dollar spot market dump, an algorithmic stablecoin unpegging event, or a localized smart contract exploit can trigger cascading liquidations across perpetual swap desks, erasing 30% to 50% of an unhedged token's valuation within a single multi-minute candlestick frame.

- For retail market participants, navigating these high-velocity cycles using manual, ad-hoc execution timing introduces severe psychological bias. Human biology is inherently ill-equipped to handle real-time financial drawdowns; when a position enters a loss state, the cognitive illusion of loss aversion compels the individual to freeze, hold their breath, and irrationally hope for a mean-reversion bounce. This emotional friction turns routine, minor trading errors into terminal, account-destroying liquidations.

- To survive this hostile landscape cleanly, professional asset allocators abandon subjective human decision-making entirely. They treat risk management as a cold, non-negotiable software engineering problem, embedding automated execution scripts directly into their order routing desks.

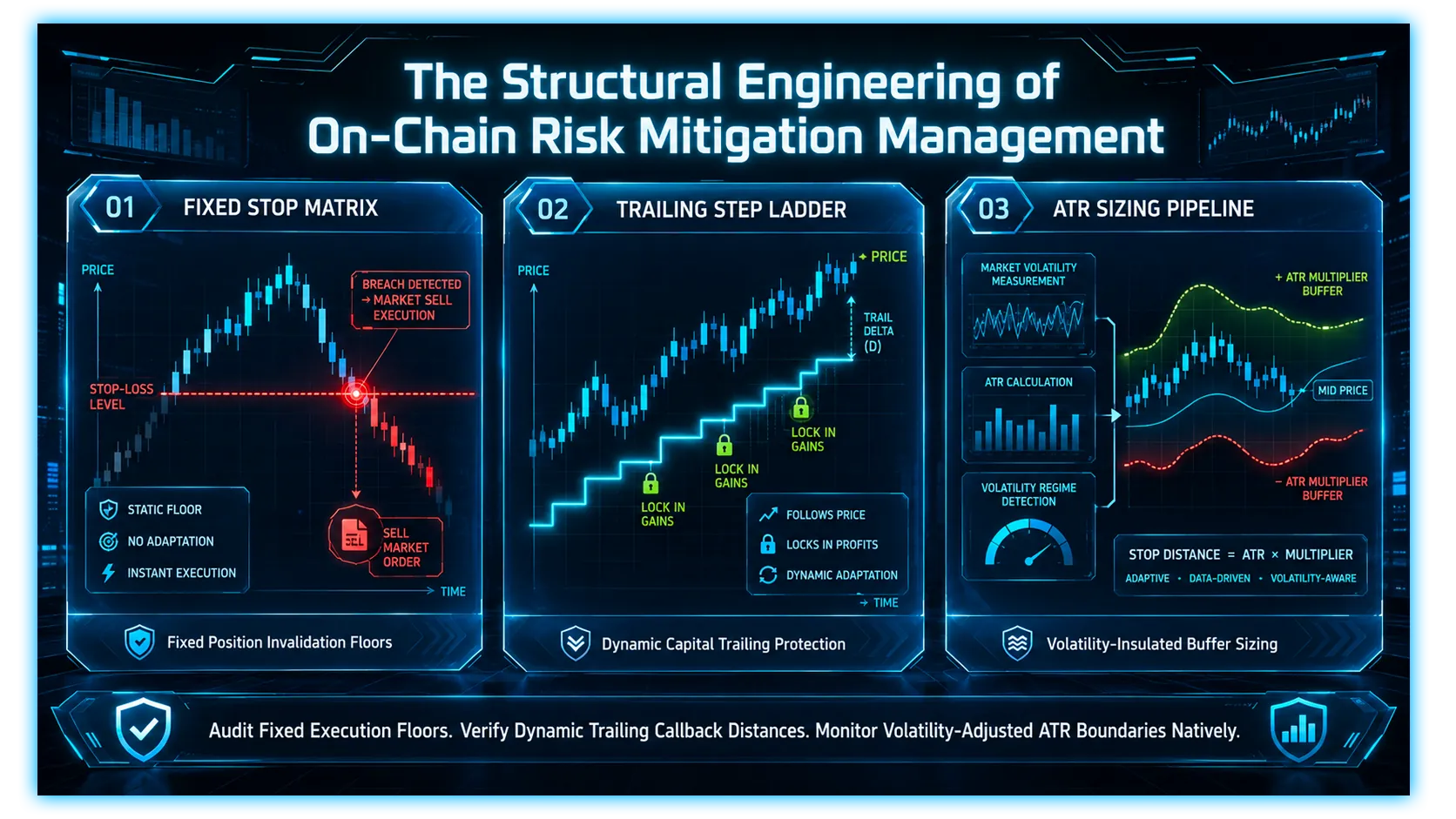

- The two primary architectural pillars used to automate this structural capital protection are the Fixed Stop Loss and the Trailing Stop. Yet, choosing which tool to deploy across a specific market regime is not a matter of casual preference; it demands a deep structural understanding of limit order book mechanics, order routing latency, volatility-adjusted buffer sizing, and market maker liquidity hunt scripts. This extensive technical guide untangles the mechanical engineering of both order types, isolates their unique vulnerabilities under stress, profiles advanced Average True Range configurations, and establishes a definitive tactical selection matrix.

1. Fixed Stop Loss: The Unyielding Line of Position Invalidation

- The Fixed Stop Loss represents the absolute, stationary boundary floor of your position's invalidation thesis. It answers a simple, cold structural question: At what precise price point does the market prove my underlying directional hypothesis is mathematically dead?

- To execute a fixed stop loss with institutional efficiency, you must look past the superficial button on your user interface and understand how your exchange’s internal matching engine processes the order packet. A fixed stop loss is composed of two independent functional layers: the Trigger Price and the Execution Payload.

The Trigger Price

The Trigger Price acts as an internal algorithmic alarm clock. It sits silently inside the exchange's matching engine cache, completely hidden from the public resting limit order book. Because it is dormant, a resting stop loss injects zero visible passive liquidity into the depth chart.

The Execution Payload: Stop-Market vs. Stop-Limit

The exact millisecond the active spot price touches your trigger coordinate, your stop order wakes up and instantly converts into a live, aggressive order packet broadcast straight to the active matching matrix. You must pre-configure how this payload behaves:

The Stop-Market Order (The Survival Standard): When triggered, your order transforms into an aggressive market taker order. It demands immediate execution at any price, chewing through whatever buy bids are resting at the top of the order book. This configuration guarantees your position is fully closed out, acting as an essential emergency escape hatch during catastrophic structural breakdowns.

The Stop-Limit Order (The Slippage Trap): When triggered, your order transforms into a standard passive limit order resting at a pre-set price line. While this prevents you from selling at an unfavorable discount, it introduces extreme execution risks inside high-velocity crypto markets. If the asset enters a vertical flash-liquidation drop, the spot price can gap clean over your limit price before the matching engine can fill your size, leaving you holding a completely unhedged, collapsing bag with zero downside protection.

2. Trailing Stop Loss: The Adaptive Capital Staircase

While a fixed stop loss acts as an unmoving protective shield, a Trailing Stop functions as a dynamic, one-way adaptive escalator. It is explicitly engineered to capture extended upside price discovery runs across high-momentum expansion trends while programmatically locking in accrued paper profits and capping maximum drawdown risk.

The Callback Mechanics and the Step Ladder

The core operational logic of a trailing stop is defined by asymmetric, directional movement tracking. You initialize the order by configuring a specific tracking parameter, structured either as a fixed nominal dollar distance (e.g., $5.00) or a precise Callback Percentage (e.g., 5%).

The behavioral feedback loop of a trailing stop follows a strict mathematical staircase protocol:

The Upward Ascent: As long as the asset's spot price continues to scale higher, print new local highs, and climb up-curve, the trailing stop baseline shifts upward in perfect lockstep, automatically maintaining your defined 5% callback gap underneath the absolute peak of the trend.

The Impenetrable Ceiling Ratchet: The exact millisecond the asset's price momentum stalls and enters a local correction, the trailing stop line locks completely flat. The underlying code script contains a strict one-way mathematical ratchet function: the stop trigger can only scale upward; it is technically incapable of moving downward. * The Trigger Squeeze: If the market's correction deepens until the price drops exactly 5% from its absolute cycle peak, the spot price collides with the frozen trailing stop baseline, instantly triggering an automated market order payload to seal your accrued gains.

This adaptive architecture completely eliminates the need to manually time local macro market tops, allowing trend-following allocators to remain safely nested inside a powerful bull expansion run until the exact moment the trend structure officially breaks down.

3. Structural Vulnerabilities: Slippage, Liquidity Gaps, and Stop Hunts

Deploying automated stop protocols without analyzing the underlying mechanics of market microstructure can trap your capital flow in devastating execution deficits. Both order types are highly vulnerable to localized matching anomalies.

The Slippage Reality in Flash Liquidity Gaps

- A common point of confusion for retail participants is the belief that if they set an automated stop-market order at exactly $100.00, their capital is guaranteed to exit at precisely $100.00. This is a severe financial misconception.

- During an intense panic event or a multi-million dollar cascading liquidations sweep, market makers and algorithmic liquidity desks instantly pull their resting limit buy orders from the book to insulate themselves from taking on toxic inventory. This defensive action creates an Order Book Vacuum or liquidity gap.

- When your trigger price of $100.00 is ticked, your stop order transforms into a market taker order. However, if the closest resting institutional buy bid on the depth ledger has plummeted down to $92.00, your order will slide straight through the void, filling at $92.00. This execution gap is Slippage: the real-world transactional friction that can drastically expand your computed maximum drawdown parameters during periods of high-amplitude volatility.

The Algorithmic Stop Hunt (Liquidity Raids)

Because major public blockchains process value across open, transparent ledgers, and centralized derivatives exchanges track millions of clustered retail positions, sophisticated high-frequency trading (HFT) desks and institutional whales know exactly where retail stops are stacked. Retail traders are highly predictable; they systematically place their fixed stop-losses slightly beneath obvious psychological integers or clear structural support levels (such as just below a major local swing low).

When a whale or market maker looking to accumulate a massive spot tranche identifies a dense cluster of retail stop-losses sitting just below support, they will execute an intentional Liquidity Raid:

The Intentional Press: The whale aggressively market-sells a block of tokens, driving the spot price down past the visible support line.

The Liquidation Cascade: The moment the price pierces the line, it triggers the massive cluster of hidden retail stop-market orders. This forced automated retail selling floods the limit order book with liquid spot supply within a fraction of a second.

The V-Shaped Reversal: The whale's high-frequency accumulation scripts instantly absorb this forced supply, filling their institutional size at a deep, artificial discount. Once the retail stop supply is fully vacuumed up, the selling pressure collapses to zero, and the price executes an immediate, sharp V-shaped bounce, leaving the retail traders stopped out at the exact absolute bottom of the market correction.

4. Advanced Configuration: Volatility-Adjusted ATR Sizing

- To protect your portfolio from being stopped out prematurely by routine market wiggles and intentional algorithmic liquidity raids, you must move past static, arbitrary percentage-based stop allocations. Setting a fixed 5% stop loss across every asset inside your portfolio is an unscientific operational error; a 5% stop might be perfectly insulated for a highly capitalized macro blue-chip like Bitcoin, yet completely useless for a hyper-volatile, high-beta utility token that undergoes routine 10% daily intraday fluctuations.

- Professional quantitative allocators adjust their stop distances dynamically based on real-time asset velocity using the Average True Range (ATR) metric. Developed by J. Welles Wilder Jr., the ATR calculates the exact geometric volatility profile of an asset over a specified lookback window (typically 14 periods) by measuring the absolute spatial spans between historical candle highs, lows, and closing parameters.

The Multiplier Framework

By tethering your stop-loss distance directly to the ATR, you construct a volatility-insulated buffer zone that expands and contracts in perfect harmony with the asset's active market footprint. The industrial standard configuration utilizes a multiplier factor, mapped against the current ATR value.

The mathematical formula to define your volatility-adjusted stop baseline during an uptrend execution follows a strict structural loop:

High-Volatility Regime Sizing: When the asset enters an intense volatility regime featuring wide trading spans, the ATR value expands. The formula automatically widens your stop-loss distance, preventing your position from being cleaned out by random, non-trend-altering intraday noise wicks.

Low-Volatility Regime Sizing: Conversely, when the token enters a quiet, highly compressed consolidation phase, the ATR contracts. The formula tightens your stop boundary closer to the price action, maximizing your capital efficiency and optimizing your overall risk-to-reward metrics.

Applying this exact ATR logic to your trailing stops creates an advanced execution system known as the Trailing Chandelier Exit. Instead of tracking the price using an arbitrary percentage callback, the trailing staircase advances upward at a precise distance beneath the highest local high of the expansion run, securing an elite balance between capital protection and trend tolerance.

Stop Protection Structural Metrics Matrix

| Order Typology | Mathematical Movement Axis | Primary Operational Hazard | Optimal Market Sandbox |

| Fixed Stop Loss | Completely Static Floor | Vulnerable to predatory stop hunts | Position Invalidation Verification |

| Trailing Stop | Dynamic One-Way Escalator | Premature exit during deep wiggles | Parabolic Trend Maximization |

ATR Volatility Sizing Multipliers

| Multiplier Weight (C) | Buffer Profile Depth | Structural Protection Tier | Intended Asset Horizon |

| 1.5 $\times$ ATR | Tight / Sensitive | Aggressive Capital Protection | High-Frequency Intraday Scalping |

| 2.0 $\times$ ATR | Medium / Balanced | Standard Market Noise Insulation | Core Altcoin Swing Trading |

| 3.0 $\times$ ATR | Wide / Institutional | Maximum Liquidity Raid Defense | Long-Term Macro Trend Following |

5. Tactical Blueprint: When to Deploy Each Architecture

Mastering defensive execution requires matching the appropriate order architecture to the active macroeconomic structural regime of the asset.

When to Deploy a Fixed Stop Loss

High-Leverage Support Break Trading: When you enter a position based on a strict breakout thesis above a long-term horizontal resistance ceiling or structural chart pattern. Your stop must sit immovably beneath the breakout floor; if the price slips back inside the pattern, your thesis is completely dead, and you must exit immediately.

Illiquid Asset Environments: Inside thin order books, trailing stops are highly dangerous because a single random whale wick can easily drop the asset 10% before bouncing back, triggering a premature trailing exit. A fixed stop loss placed deep beneath an institutional High Volume Node peak protects you from minor intraday distortions.

When to Deploy a Trailing Stop

Parabolic Price Discovery Runs: When an asset successfully breaks past its all-time high and enters open price discovery mode. Because there are no historical overhead resistance lines or past volume profiles available to guide your take-profit orders, deploying a trailing stop ensures you ride the vertical mania wave up until the exact microsecond the macro trend peaks and flips downward.

Defensive Profit Scaling on Core Swings: When an altcoin swing position achieves an initial profit milestone, initialize a trailing stop to replace your fixed stop floor. This tactical migration automatically converts a speculative trade into a risk-free position, guaranteeing that no matter how erratically the market behaves down-curve, you exit the setup with realized profit locked in.

6. Integrating Telemetry Auditing via DEXTools

- As you secure your seed phrase storage and hardware wallet setup, maintaining visibility over decentralized markets remains essential. DEXTools provides advanced analytics to monitor live token behavior, liquidity pools, contract data, and market activity across public blockchain networks.

- With tools like Pair Explorer, Live New Pairs, Trade Story, Top Traders, and Big Swap Explorer, traders can audit volume trends, track whale movements, review liquidity depth, and check contract safety before interacting on-chain. This helps ensure secured wallets engage only with verified and liquid market venues while private keys remain safely protected offline.

You can access DEXTools here and start trading today!

Disclaimer: This article is for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other kind of advice. DEXTools does not recommend buying, selling, or holding any cryptocurrency or token. Users should conduct their own research and consult with a qualified financial advisor before making any investment decisions. Cryptocurrency investments are volatile and high-risk. DEXTools is not responsible for any losses incurred.