What Is Futures Trading in Crypto? Guide 2026

— By Tony Rabbit in Tutorials

What is futures trading in crypto? Learn how leverage, margin, funding, and liquidation work, why traders use perps, and the risk workflow for beginners.

Crypto futures look exciting because the interface is simple. You choose long or short, pick a size, and watch profit and loss move faster than it would on spot. What makes the product powerful is also what makes it dangerous: you are usually trading a contract, not the coin itself, and that contract comes with leverage, margin rules, funding payments, and liquidation risk.

Intent check: This guide focuses on leverage, margin, funding, and liquidation. If you are deciding between cash trading and derivatives, read Spot vs Futures in Crypto. If you specifically want the no-expiry version of futures, read What Are Perpetual Futures in Crypto?

Quick answer: futures trading in crypto means trading a derivative contract that tracks a coin's price instead of owning the coin directly. Most retail crypto futures are perpetual futures, which let traders use leverage, short the market, hedge spot holdings, and stay in a position without expiry, but they also introduce funding costs, stricter risk management, and the possibility of forced liquidation.

- You are trading exposure, not ownership. In most futures markets you cannot withdraw the underlying token because the position is a contract tied to price.

- Leverage changes the speed of profit and loss. Small market moves affect the full notional position, not only the collateral you posted.

- Liquidation is the defining futures risk. A trade can be structurally right and still fail if the position is too large for normal volatility.

- Funding and open interest matter. They help explain when a perpetual market is becoming crowded, expensive, or fragile.

- Beginners usually need a risk workflow before they need more leverage. Futures reward preparation far more than excitement.

What futures trading means in crypto

Crypto futures are contracts whose value follows an underlying asset such as BTC, ETH, SOL, or another token. You are taking a position on price direction and price change, not taking delivery of the asset itself. If Bitcoin rises and you are long, the contract gains value. If Bitcoin falls and you are short, the contract gains value. Either way, the trade is about synthetic exposure.

That synthetic layer is why futures feel more flexible than spot. They let traders go short without selling owned coins, hedge existing holdings, and size positions with less upfront capital. The trade-off is that futures have more moving parts, and every moving part can become a source of error if you do not understand it.

Exposure instead of ownership

When you buy spot ETH, you own ETH. You can withdraw it, hold it, bridge it, or stake it if the venue and asset support that use case. In futures, you usually cannot do any of those things because you are not holding the asset itself. You are holding a contract whose value references the asset price.

That distinction shapes everything else. Spot traders think in terms of ownership, custody, and whether the asset is worth holding. Futures traders think in terms of collateral, notional size, liquidation distance, carry cost, and whether the trade can survive normal market noise.

Perpetual futures vs dated futures

Traditional futures have an expiry date. A trader may buy a quarterly contract, hold it through the quarter, and then let it settle or roll into the next contract. In crypto, most retail traders use perpetual futures, often called perps, which do not expire. The position stays open until you close it, reduce it, or get liquidated.

Because perpetuals have no expiry, they use funding payments to keep the contract reasonably close to the spot market. That is why many traders use the words futures and perps almost interchangeably in crypto. In practice, if a venue advertises crypto futures for retail users, the product is often a perpetual contract.

The four moving parts inside a futures position

A futures position looks simple on screen, but it is built from a few separate parts: collateral, notional size, direction, and the venue's risk engine. If you understand those parts, most of the confusing jargon becomes manageable.

Collateral, notional size, and leverage

Suppose you post $1,000 in collateral and open a 5x long. You do not have $1,000 of exposure anymore. You control about $5,000 of notional exposure. If the market rises 4%, the position gains about $200 before fees and funding. If the market falls 4%, the position loses about $200. The underlying asset moved 4%, but your collateral felt a 20% swing because the position was larger than the cash you posted.

This is the essential truth about leverage. It does not improve the market idea. It changes the sensitivity of the trade. Higher leverage can make a modest move matter more, but it also pushes the liquidation threshold closer to your entry. The more leverage you use, the less ordinary market volatility you can survive.

Long and short exposure

A long futures position benefits when price rises. A short futures position benefits when price falls. This is one of the main reasons traders use futures instead of spot. They can express a bearish view directly, and they can hedge an existing portfolio without selling long-term holdings.

For example, a trader who owns spot ETH for a long-term thesis may still short ETH perps for a few days if macro conditions look weak and they do not want to sell the underlying asset. That flexibility is useful, but it is not free. A badly timed short can get squeezed just as violently as an overleveraged long can get liquidated.

Isolated margin vs cross margin

With isolated margin, you assign a defined amount of collateral to one position. If the trade fails, the loss is limited to that isolated margin. With cross margin, the platform can use a wider pool of account equity to keep the position alive. Cross margin gives a position more breathing room, but it also means one bad trade can threaten more of your account.

For most beginners, isolated margin is easier to reason about because the risk boundary is clearer. Cross margin has real uses, especially for hedging or portfolio-level management, but it requires more discipline because the account is sharing risk across positions.

Mark price, maintenance margin, and liquidation

Many beginners assume liquidation happens only when the last traded price touches a scary number. In reality, most venues use a mark price, which is meant to be a fairer reference price than one noisy print. They also require a minimum level of account equity called maintenance margin. When the remaining buffer falls too low, the venue reduces or closes the position.

This is why a good market idea can still fail in futures. Your chart thesis might say the trade only becomes invalid if BTC loses a major daily level, but your liquidation level might sit much closer because the position is oversized. The platform does not care that you planned to be right later.

How profit, loss, and funding actually work

Futures profit and loss is not only about whether price went up or down. The platform is also tracking unrealized PnL, mark price, funding, and how close the position is to liquidation. Reading all of that together is more useful than staring at the green or red number alone.

Unrealized PnL vs realized PnL

Unrealized PnL is the floating gain or loss on an open position. It changes as price changes. Realized PnL appears only when you fully or partially close. New traders often treat a strong unrealized gain as if it is already secured, then watch it disappear because they never defined an exit plan.

That is why professional-looking futures trading often seems boring. The trader already knows where they will reduce size, where they will cut the trade, and how much they are willing to let a winner retrace before they act.

Funding rates and the cost of holding a perp

Because perpetual futures do not expire, traders may periodically pay or receive funding while the position stays open. If funding is strongly positive, longs usually pay shorts. If funding is strongly negative, shorts usually pay longs. Normal funding is just part of the product. Extreme funding often tells you that one side of the market is getting crowded.

Funding matters in two ways. First, it is a carrying cost if you hold a position for hours or days. Second, it is a sentiment clue. A trader entering a late long into aggressively positive funding is stepping into a different environment than a trader entering a neutral market. If you want the full mechanics, this article should hand off to the dedicated funding-rate guide.

A simple long example with numbers

Imagine SOL is trading at $150. You post $500 in collateral and open a 4x long, so your position controls roughly $2,000 of notional value. Your invalidation level is $144, which is about 4% below entry. If price trades down to that invalidation and you exit there, the loss is about $80 before fees and funding. That is meaningful, but manageable.

Now take the same trade idea and increase leverage to 15x. Your notional exposure becomes about $7,500. The same 4% adverse move now threatens roughly $300 before fees, and the liquidation level sits far closer to entry. The market idea did not change at all. Only the fragility changed. This is why leverage selection is a risk decision, not a confidence statement.

Why liquidation often happens before a trader can be right later

Crypto is full of sharp wicks, stop runs, and emotional bursts. Spot traders can sometimes survive being early if they sized responsibly and still believe the thesis. Futures traders do not always get that luxury. A brief move through the liquidation band ends the position even if price recovers ten minutes later.

That is the futures lesson many traders learn the hard way. The chart does not only need to go where you think. It needs to get there without taking you out first.

Why traders use futures instead of spot

Futures are not better than spot by default. They are useful when the product solves a specific problem.

Shorting the market directly

The clearest advantage is direct short exposure. If a setup looks weak, futures let you express that view without selling owned coins or constructing a more awkward workaround. For active traders, that ability alone makes futures valuable.

Hedging an existing bag

Futures are also useful for hedging. Imagine a trader who holds a long-term BTC position but expects short-term macro volatility around a major rate decision. Instead of selling the whole bag and potentially losing the core position, they may open a smaller BTC perp short to offset part of the downside. The hedge is not meant to be a lifestyle. It is a temporary risk-management tool.

Capital efficiency for active traders

Because futures require less upfront cash than buying the full spot position, they can be more capital-efficient for traders who actively manage risk and opportunity across several markets. That said, capital efficiency is only useful when the trader is also efficient at controlling losses. Without that second skill, leverage becomes borrowed fragility.

Keeping cash simple while expressing a view

Stablecoin-margined perps let traders stay in a cash-like collateral base while still taking directional exposure. That can be operationally convenient, especially for short-term traders. It does not remove counterparty, execution, or liquidation risk. It simply changes how the exposure is packaged.

A beginner-safe risk workflow before every futures trade

Futures feel chaotic when every decision happens inside the trading panel. They become much clearer when you follow the same sequence every time.

- Start with the chart, not the leverage selector. Mark trend, support, resistance, and the exact level that would invalidate the idea.

- Define maximum cash loss first. Decide what dollar amount or account percentage you are willing to lose, then size the position from that limit. The correct notional size should come from stop distance, not from whatever leverage the venue allows.

- Check derivatives context. Review open interest, funding, and whether the market already looks crowded. A good setup in an overheated derivatives environment may deserve smaller size or no trade at all.

- Choose isolated margin and realistic leverage. Most beginners survive longer when the risk is ring-fenced and the liquidation level is comfortably outside ordinary noise.

- Plan exits before entry. Write down where you will stop out, where you may take partial profit, and how you will manage the trade if it starts working. Reduce-only orders are helpful when the venue supports them.

- Check the instrument itself. Some alt perps have wider spreads, thinner books, and rougher mark-price behavior than the major pairs. A decent idea can become a poor trade on a bad contract.

The workflow sounds slow. That is exactly why it helps. Futures punish improvisation.

Common beginner mistakes that turn a good idea into a bad trade

- Using leverage as an emotion amplifier: size should respond to risk, not to how strongly you feel about the setup.

- Ignoring liquidation distance: if normal intraday volatility can liquidate you, the position is too fragile.

- Averaging down because the liquidation level feels close: adding to a losing perp without a fresh thesis often compounds the problem instead of fixing it.

- Holding through expensive funding or thin-liquidity hours without a plan: the environment can worsen even when price barely moves.

- Trading small alt contracts like they are BTC: weaker liquidity and faster squeezes make mistakes more expensive.

A simple self-check helps: if you cannot explain your trade size, invalidation, liquidation distance, and exit plan in one calm sentence each, the trade probably is not ready.

Practical DEXTools workflow before placing a futures trade

DEXTools is useful before the actual perp order because it helps answer a question many traders skip: does the underlying token deserve leveraged attention at all?

- Validate the asset first. Check liquidity, pair quality, recent volume, and whether the spot market looks orderly enough to respect technical levels.

- Review wallet and trade behavior. One-wallet spikes, suspicious activity, or obviously noisy pair behavior should reduce confidence, especially on smaller names.

- Map the important spot levels. Futures traders still get liquidated around spot-driven support and resistance, so the underlying chart comes first.

- Only then open the perp venue. Compare funding, spread, and crowding conditions to see whether the derivatives side is calm, neutral, or overheated.

- Use platform tutorials only after the market thesis exists. Readers who need venue mechanics can continue to how to use Hyperliquid for perpetual trading.

That order matters because it keeps the trading interface from becoming the idea. The thesis should exist before leverage is added.

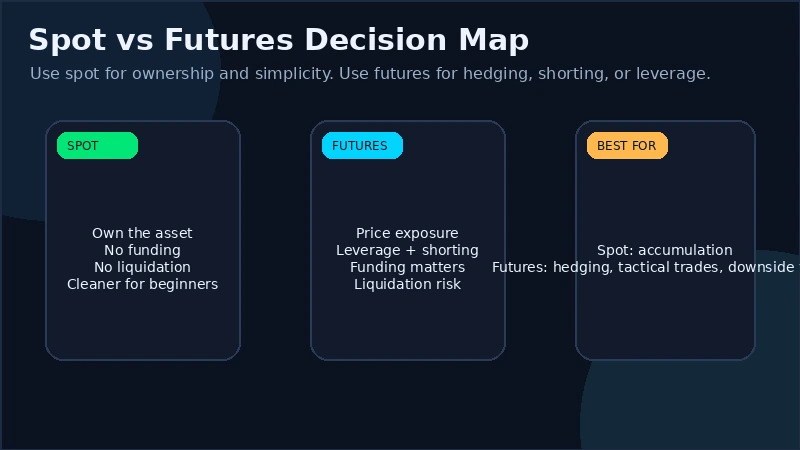

Spot vs futures in one quick decision block

This page should stay focused on futures, so keep the comparison compact. Readers who want the full side-by-side breakdown should move to our dedicated spot vs futures guide.

| Question | Spot is usually better if... | Futures is usually better if... |

|---|---|---|

| Do you want to own the asset? | Yes, you want direct ownership or withdrawal. | No, you mainly want price exposure. |

| Do you need leverage or short exposure? | No, simple buying and selling is enough. | Yes, you need leverage, hedging, or direct downside trades. |

| Can the position survive being early? | Usually yes, if the size is sensible and the thesis still holds. | Only if leverage is conservative and liquidation sits well outside normal noise. |

| Will carrying costs matter? | There is no perpetual funding cost by default. | Funding and liquidation mechanics are part of the trade. |

Who futures are actually for

Futures are usually best for traders who already know why they need them: active short-term traders, hedgers, and experienced spot participants who understand sizing and volatility. They are usually a poor first product for someone still learning basic market structure, order execution, or emotional control.

If you are new, spot is not the boring version of trading. It is often the clearer classroom. Futures become useful when you can explain exactly why leverage, short exposure, or hedging adds something specific to your process.

Frequently asked questions

What is the difference between crypto futures and perpetual futures?

Crypto futures is the broader category. Perpetual futures are the non-expiring version most retail traders use, and they stay anchored to spot through funding payments rather than an expiry date.

Do you own the coin when you trade crypto futures?

Usually no. In most cases you are trading a contract linked to the asset price rather than holding the underlying coin itself.

Can you lose more than your collateral in crypto futures?

Platform rules differ, so traders should always check how margin, liquidation, and negative-balance handling work on the venue they use. What never changes is that poor sizing can make the collateral disappear very quickly.

What does funding rate mean in futures trading?

Funding rate is a periodic payment exchanged between longs and shorts in perpetual markets. It helps keep perps closer to spot and also tells traders when one side of the market is becoming crowded.

Is futures trading better than spot trading for beginners?

Usually no. Spot is simpler and more forgiving because it does not include liquidation mechanics or leverage management by default. Most beginners should understand spot first and approach futures later with a defined risk process.

Final takeaway: futures trading in crypto is powerful because it gives traders flexible exposure, not because it makes the market easier. If you understand leverage, margin, funding, crowding, and liquidation, futures can become a useful tool. If you skip those mechanics, the product usually supplies the lesson for you.

Disclaimer: This draft is for educational purposes only and does not constitute investment, financial, legal, or trading advice. Futures and perpetual products are high-risk instruments.

Related Guides

- Kraken Pro Tutorial: Spot, Margin and Futures Explained

- Margin Trading in Crypto: Beginner Guide (2026)

- What Is Leverage Trading in Crypto: Complete Guide for Beginners (2026)

- Top 5 Perpetual DEXs in 2026: Best Platforms for On-Chain Leverage Trading

- Crypto Futures Explained: Perps, Quarterly and Inverse Contracts (2026)

Frequently Asked Questions

What is futures trading in crypto?

Crypto futures are contracts to buy or sell an asset at an agreed price, letting traders speculate on price direction without holding the underlying coin. They often use leverage, which amplifies both gains and losses.

How does leverage work in crypto futures?

Leverage lets you control a larger position with a smaller amount of margin, multiplying potential profit and loss. Higher leverage increases the risk of liquidation if the market moves against your position.

What is liquidation in futures trading?

Liquidation happens when your losses reduce your margin below the required level, and the position is automatically closed. It is a key risk of leveraged trading and can wipe out the margin you committed.

What is the funding rate in perpetual futures?

Perpetual futures use a funding rate, a periodic payment between long and short traders, to keep the contract price near the spot price. Depending on market conditions, you may pay or receive funding while holding a position.