Cash vs In-Kind: Crypto ETF Foundations

Understanding how funds are built is vital for institutional investors. We dissect the mechanical differences between Cash and In-Kind creation pathways in modern digital asset ETFs.

Cash vs In-Kind Creation Models: The Structural Foundations of Crypto ETFs

- The rapid expansion of the digital asset industry has brought ETF Creation Models to the forefront of institutional strategy. While the average investor focuses on the daily performance of an ETF share, the underlying mechanics of how these funds are built determine their tax efficiency, operational friction, and regulatory compliance.

- The fundamental distinction between "Cash Creation" and "In-Kind Creation" is not merely an administrative detail; it is the cornerstone upon which the entire U.S. regulated crypto-investment framework currently rests.

Understanding the Creation/Redemption Loop

- To understand the difference between ETF Creation Models, one must first understand the role of the Authorized Participant (AP). In a traditional ETF, an AP delivers assets to the fund in exchange for shares.

- The decision of whether that delivery is made in cash or in the actual underlying asset (the "In-Kind" model) changes the entire financial profile of the product.

Let's learn about Cash vs In-Kind models.

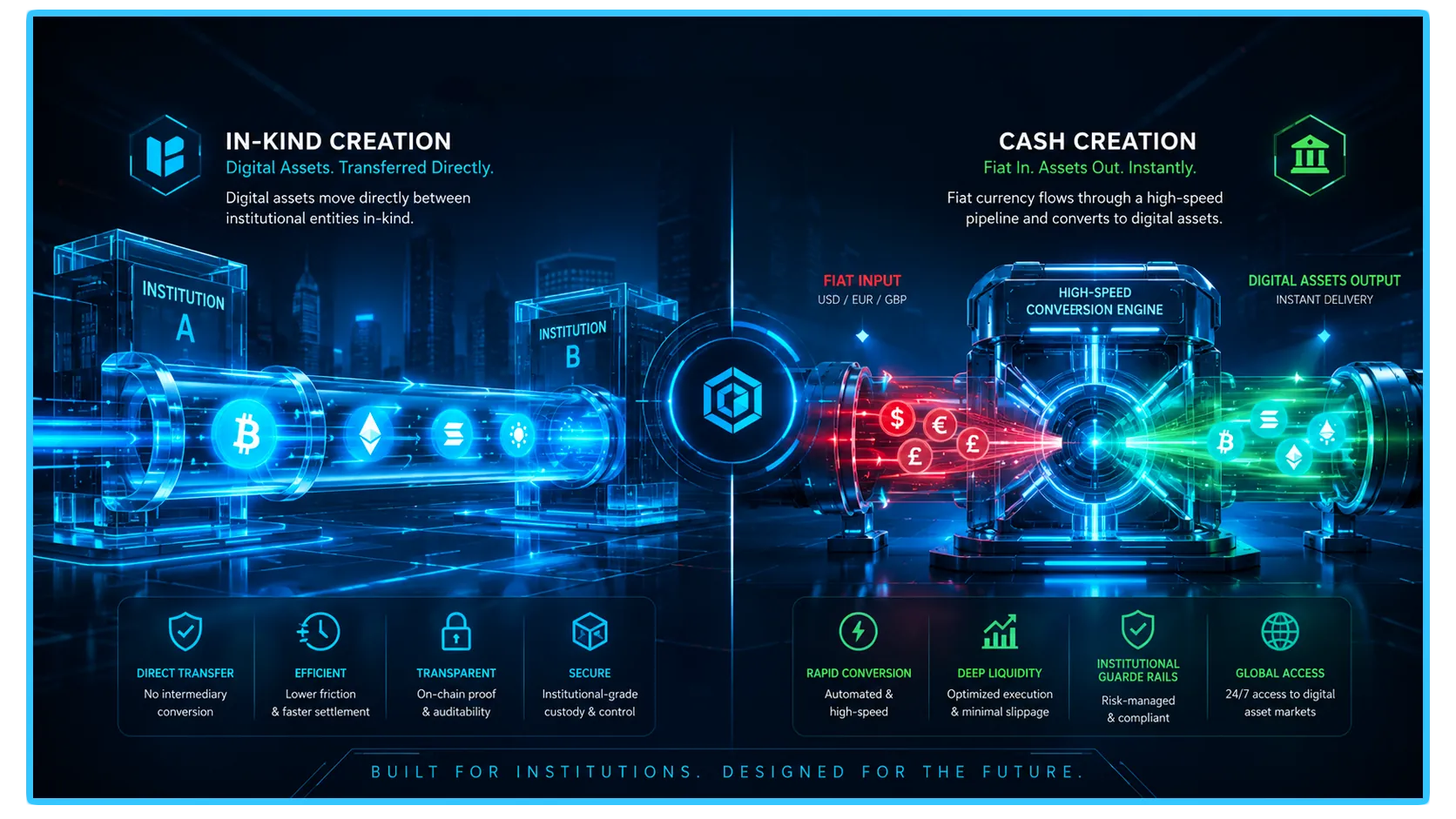

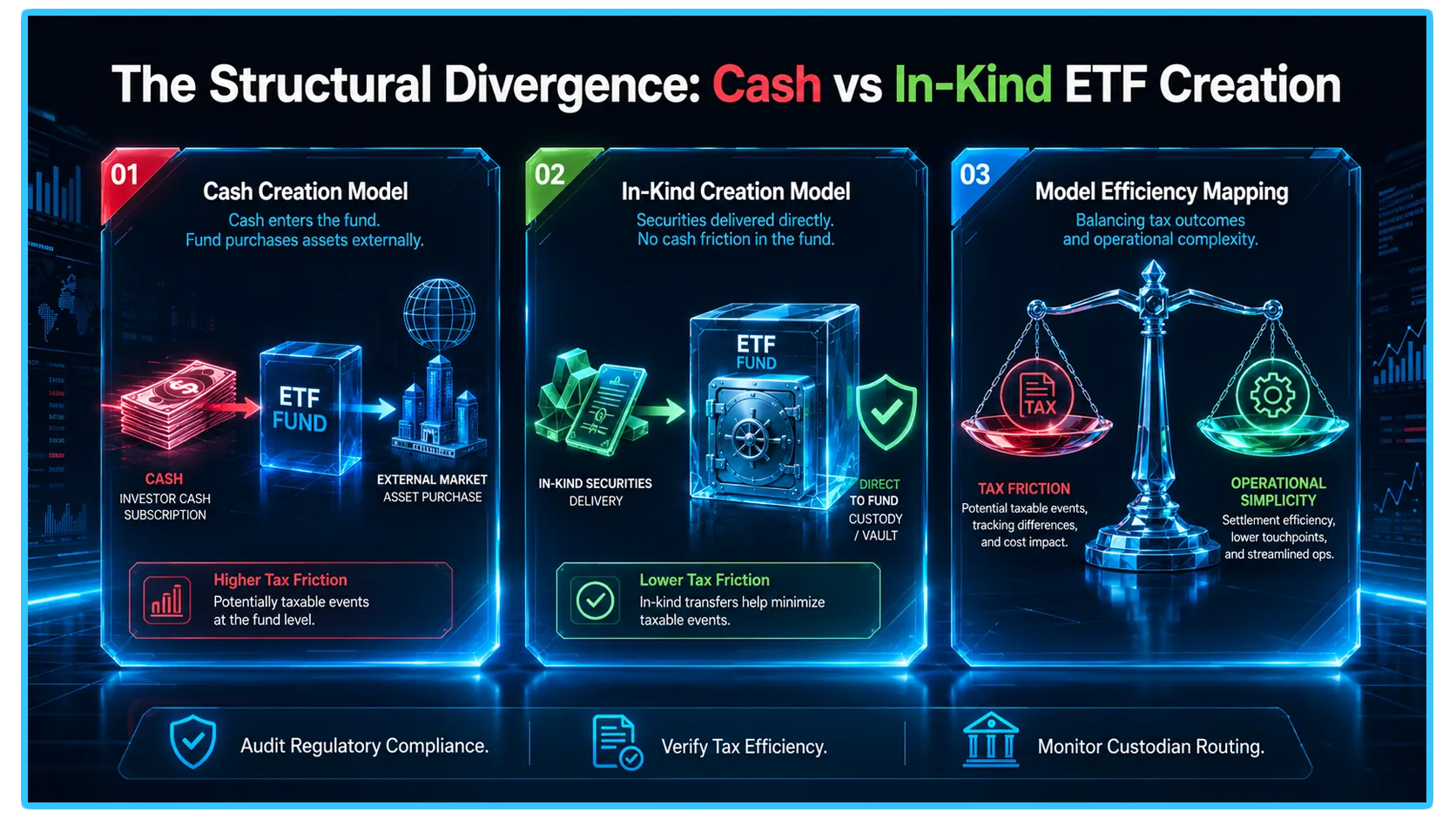

The Cash Creation Model

- Under the cash-only model, when institutional demand surges, the AP provides cash to the ETF manager. The manager then takes that capital to the open market, utilizes institutional-grade OTC desks, and purchases the underlying Bitcoin or Ethereum.

- This model is currently the standard for U.S.-based spot crypto ETFs. It is favored by regulators because it keeps the "dirty work" of asset procurement strictly within the realm of regulated, bank-intermediated trading venues. The fund manager does not need to handle complex, decentralized asset transfers from the AP; they simply receive fiat, buy the asset, and vault it with a regulated custodian.

The In-Kind Creation Model

- In the in-kind model, the AP delivers the actual digital assets directly to the fund’s custodian. This is the traditional standard for physical commodity ETFs like Gold. It is highly efficient because it removes the middle step of the manager having to perform market buys.

- However, it requires the fund to have a sophisticated, regulatory-approved pipeline for accepting and verifying direct token transfers from the AP's wallet to the fund's vault.

Taxation, Custody, and Regulatory Friction

The choice of ETF Creation Models has profound implications for the end investor, primarily through the lens of tax friction and custodian integration.

Tax Efficiency and Realization

- One of the primary benefits of the in-kind model in traditional finance is its tax efficiency. When an AP delivers an asset in-kind, it is generally not a taxable realization event. In contrast, if a fund is forced to buy assets using cash, there is a risk of slippage and potentially different tax treatment for the APs involved.

- For the U.S. market, regulators have been hesitant to approve in-kind crypto ETFs due to concerns about the identity of the entities delivering the assets. They want to ensure that no illicit or unverified capital is entering the regulated fund structure through the backdoor of an in-kind transfer.

Custody and Operational Complexity

- Cash creation is, from a compliance standpoint, much simpler to manage. The custodian only needs to interface with a limited number of vetted, institutional trading desks. In an in-kind model, the custodian would need to be able to ingest digital assets from potentially any AP who meets the fund’s requirements.

- This creates a more complex "Know Your Customer" (KYC) and Anti-Money Laundering (AML) hurdle for the fund issuer, as they must ensure every asset deposited into the vault is legally "clean."

The Current Regulatory Landscape in the U.S.

- As of mid-2026, the U.S. Securities and Exchange Commission (SEC) has maintained a clear preference for cash-based ETF Creation Models. This stance is driven by a desire for total transparency and institutional control. By forcing the cash-through-brokerage pathway, the regulator ensures that every dollar of institutional capital is documented from the moment it leaves the investor's bank account to the moment it is converted into a digital asset stored in a regulated vault.

- While there have been persistent requests from large issuers to move toward an in-kind model (arguing it would improve market efficiency and tighten tracking error) the regulatory environment remains cautious. The current consensus is that the cash model provides the safest bridge for institutional adoption, even if it introduces slightly more operational friction and potential for temporary price decoupling during periods of extreme market volatility.

Telemetry and Verification

- Whether a fund utilizes cash or in-kind methods, the end goal remains price parity between the ETF share and the underlying asset. Market participants must monitor the liquidity and arbitrage efficiency of these products. DEXTools provides the critical data infrastructure to verify that the price discovery happening within the ETF sphere is echoed in the underlying decentralized market.

- By monitoring pair activity, liquidity concentration, and order book pressure on decentralized exchanges, you can audit the efficiency of these funds in real-time. DEXTools allows you to verify if the "cash creation" inflows are translating into active on-chain demand, ensuring your investment strategy is based on actual market movement rather than just administrative noise.

- You can access DEXTools here and start trading today!

Disclaimer: This article is for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other kind of advice. DEXTools does not recommend buying, selling, or holding any cryptocurrency or token. Users should conduct their own research and consult with a qualified financial advisor before making any investment decisions. Cryptocurrency investments are volatile and high-risk. DEXTools is not responsible for any losses incurred.